California Annual Policy Review: Keep Your Home Insurance Up to Date

Your home insurance policy isn’t a set-it-and-forget-it document. California’s housing market, wildfire risks, and your personal circumstances shift constantly, which means your coverage should too.

A California annual policy review catches gaps before they become expensive problems. At Cappuccino Insurance Agency, we’ve seen homeowners discover they’re underinsured only after a claim-and by then it’s too late.

Why Your Coverage Needs to Change

California homeowners often assume their insurance policy remains adequate year after year, but this assumption costs thousands in uncompensated losses. Your home’s value doesn’t stay frozen in time, and neither do the risks surrounding it. Housing prices across California have climbed significantly, with median home values in many regions increasing 5–8% annually over the past five years. If your dwelling coverage limit was set three years ago, it likely falls short of what you’d actually need to rebuild today. Replacement costs for construction materials have surged due to supply chain pressures and labor shortages, meaning the square-foot rebuilding cost in your area may be substantially higher than when you last reviewed your policy.

Home Improvements Create Immediate Coverage Problems

Renovations, additions, and upgrades demand immediate notification to your insurer. A new roof, remodeled kitchen, added deck, or finished garage increases your home’s replacement cost, but your policy limit won’t automatically adjust. Many homeowners discover this gap only after a loss, when the insurance company denies claims for improvements that weren’t listed on the policy. You must report any significant work to your insurer so your dwelling limit reflects the current, post-improvement value. This isn’t optional paperwork-it’s the difference between full recovery and out-of-pocket repair costs that could reach tens of thousands of dollars.

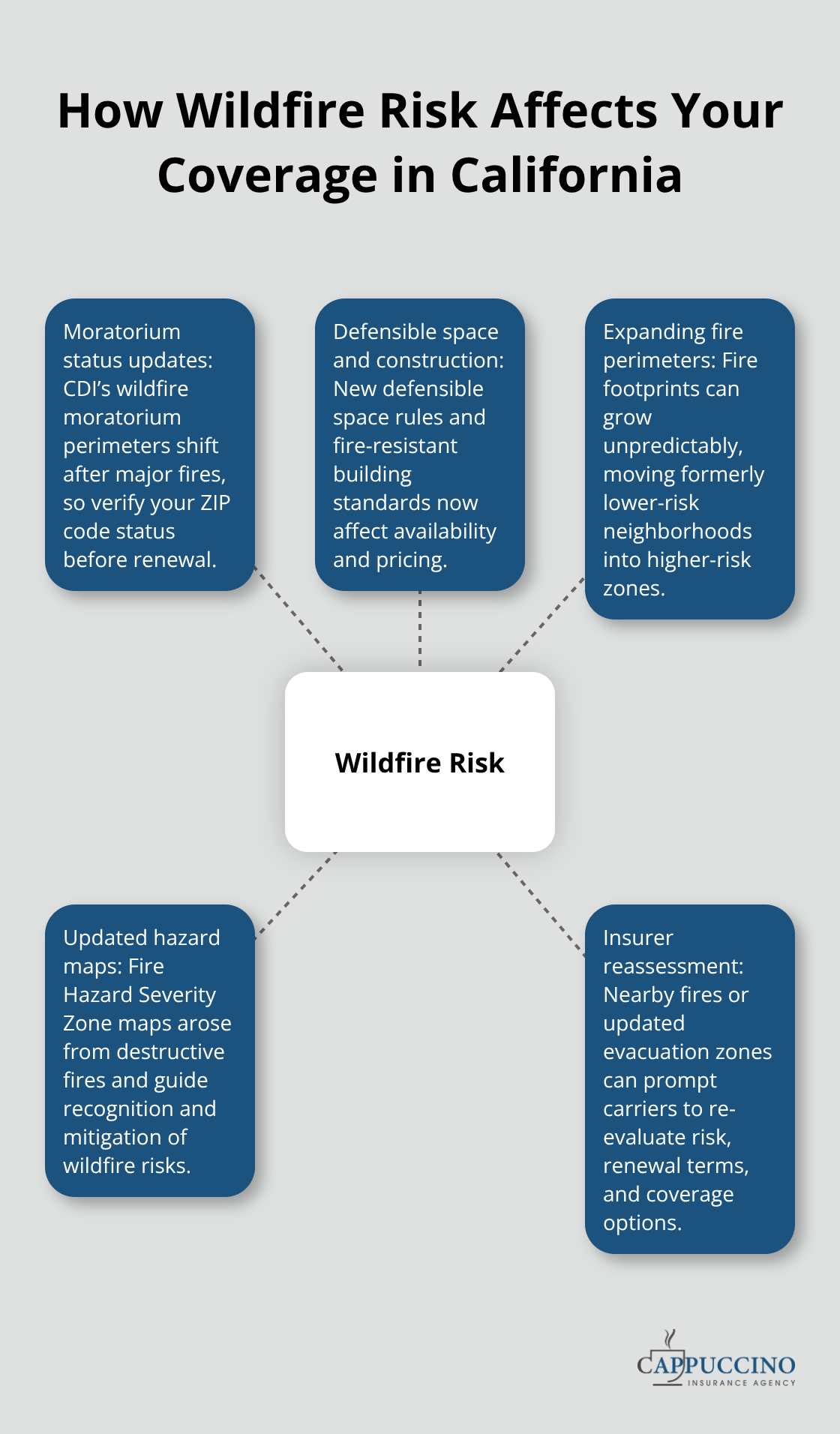

Wildfire Risk Shifts Faster Than You Think

California’s wildfire patterns have intensified dramatically, and your property’s exposure may have changed even if you haven’t moved. Fire perimeters expand unpredictably, and areas considered lower-risk five years ago may now fall within high-risk zones. The California Department of Insurance provides an online tool to check whether your ZIP code falls within a wildfire moratorium perimeter, and this status shifts with each major fire event.

Additionally, new defensible space requirements and fire-resistant construction standards now influence insurance availability and pricing in ways they didn’t previously. Fire Hazard Severity Zone maps arose from major destructive fires, prompting the recognition of these areas and strategies to reduce wildfire risks. If your neighborhood has experienced a nearby fire or if CAL FIRE has updated evacuation zones, your insurer may reassess your risk profile, potentially affecting your renewal terms or available coverage options.

These shifts in home value, property improvements, and wildfire exposure form the foundation of why annual reviews matter-but knowing what to look for during that review separates homeowners who stay protected from those who face costly surprises.

What to Review in Your Policy This Year

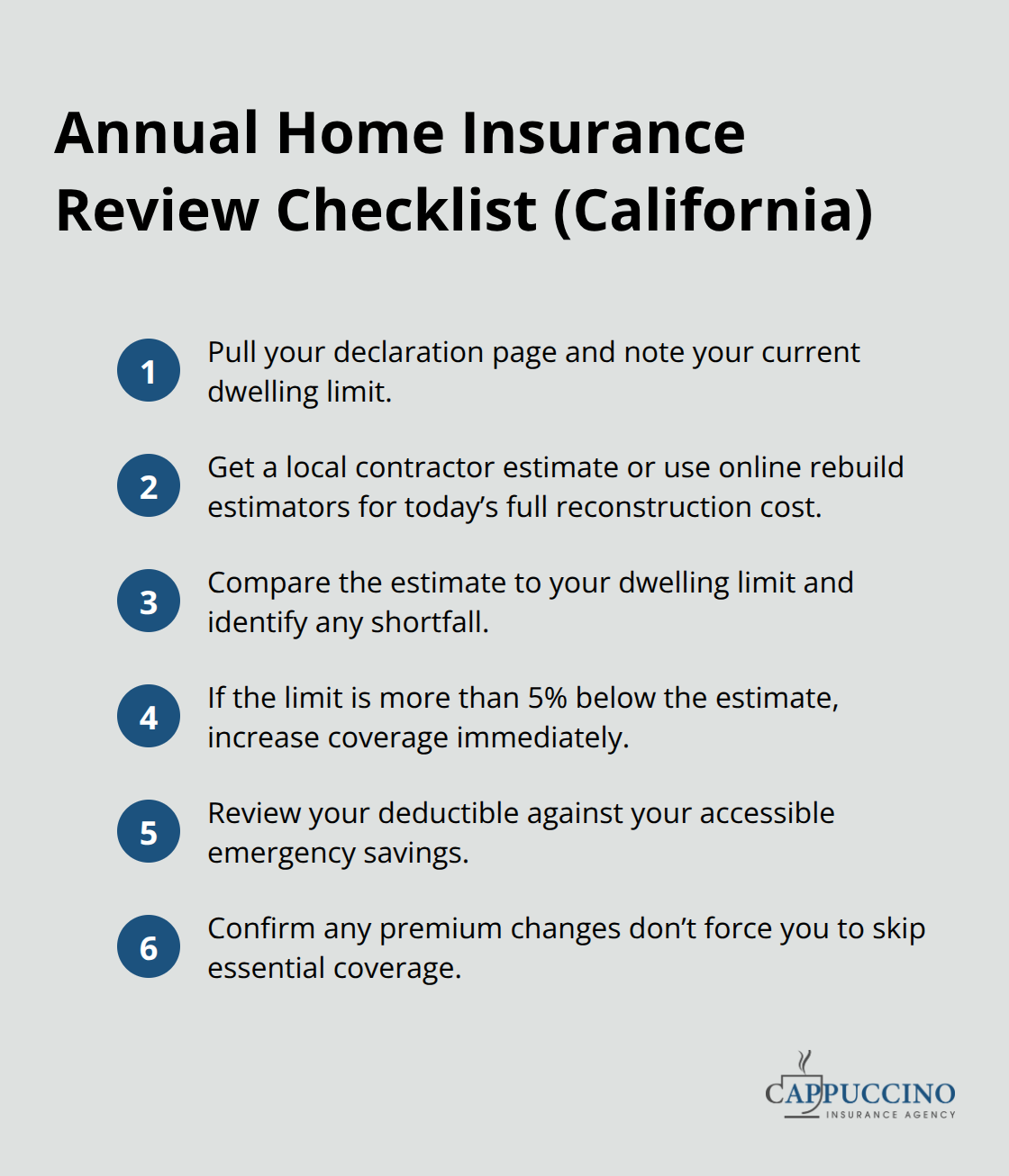

Verify Your Dwelling Coverage Against Current Rebuild Costs

Your dwelling coverage limit is the single most important number in your entire policy, yet most California homeowners haven’t verified it matches current rebuilding costs in years. Pull your declaration page and write down your dwelling limit. Next, contact a local contractor or use online rebuild estimators to determine what it would actually cost to reconstruct your home from the ground up in today’s market. Construction costs in California have risen sharply due to labor availability and material expenses, with some regions seeing rebuilding costs increase 10–15% annually. If your dwelling limit falls more than 5% below the estimated rebuild cost, you face significant underinsurance. The deductible matters equally-a $2,500 deductible sounds reasonable until you face an $8,000 roof claim and realize you pay the first $2,500 yourself. Evaluate whether your deductible aligns with your emergency savings.

If you have $15,000 in accessible savings, a $2,500 deductible is manageable. If you have $3,000 in savings, that same deductible creates financial stress after a claim.

Higher deductibles lower your premium, but only if the savings don’t force you to skip coverage you actually need. The math matters: a $500 annual premium reduction sounds attractive until a water damage claim forces you to choose between your deductible and your rent payment.

Report Home Improvements Immediately

Home improvements create coverage gaps faster than almost any other factor. Any renovation, addition, or structural upgrade requires immediate notification to your insurer-don’t wait for renewal. A finished basement, new deck, roof replacement, or kitchen remodel increases your home’s value but doesn’t automatically increase your policy limit. Your insurer won’t know about these changes unless you tell them, and that silence can invalidate claims for the improved areas. Contact your agent within 30 days of completing major work so your dwelling limit reflects the current, post-improvement value. This step prevents the painful discovery after a loss that your insurance company denies claims for improvements that weren’t listed on the policy.

Assess Wildfire Risk Changes in Your Area

Wildfire risk factors shift dramatically across California, making this review critical for anyone in or near high-risk zones. Check the California Department of Insurance’s online tool to confirm whether your ZIP code currently falls within a wildfire moratorium perimeter. These perimeters change with each major fire event, and your property’s risk classification may have shifted since your last review. If your area experienced a nearby fire within the past three years or if CAL FIRE updated evacuation zones for your neighborhood, inform your insurer immediately. Insurance carriers actively reassess risk exposure in these areas, and failing to disclose changes can jeopardize your coverage when you need it most.

Protect High-Value Items With Scheduled Coverage

Standard homeowners policies cap specialty items like fine art, jewelry, antiques, or high-value electronics at $2,500 to $5,000 total-far below replacement value for most collections. Scheduled personal property endorsements cost $50–$150 annually but protect items worth thousands. If you own valuable possessions (inherited jewelry, collectibles, or expensive electronics), verify that your policy includes adequate coverage. Without scheduled endorsements, you face significant out-of-pocket losses after a claim. These gaps in specialty coverage represent some of the most common and costly oversights we see among California homeowners, and addressing them now prevents financial devastation later.

The next step involves understanding which coverage gaps appear most frequently across California properties and how to identify whether your specific situation includes these blind spots.

Common Coverage Gaps California Homeowners Miss

Dwelling coverage falls short of actual rebuild costs

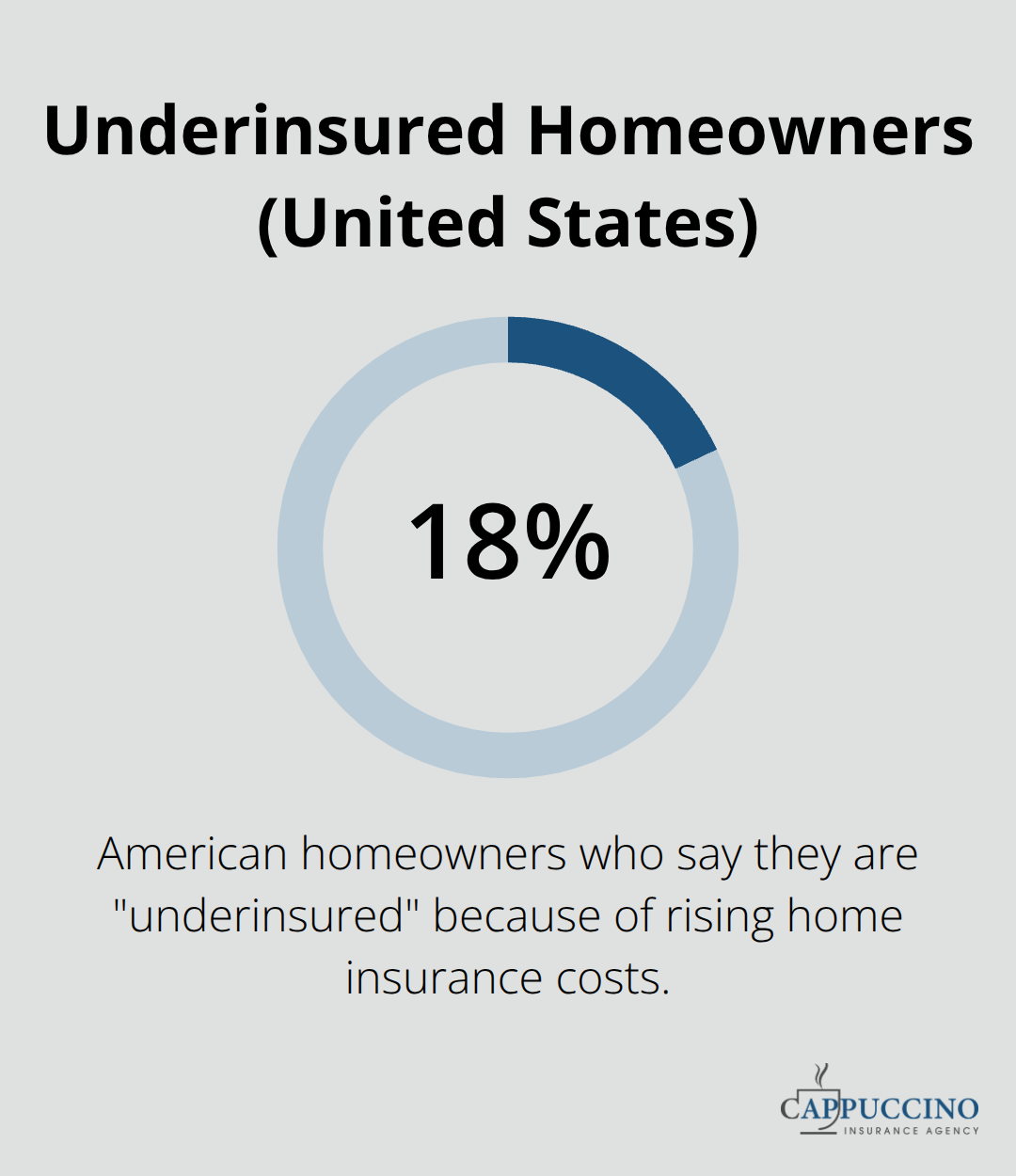

Most California homeowners discover their coverage shortfalls only after a loss occurs, and by then the financial damage is irreversible. Dwelling coverage underinsurance represents the most widespread problem we encounter. According to a recent survey, 18% of American homeowners say they’re “underinsured” because of the rising cost of home insurance, and California homeowners face this risk acutely because reconstruction costs have accelerated dramatically.

A dwelling limit set five years ago may cover only 70–80% of actual rebuild costs today, leaving homeowners responsible for significant uninsured losses.

The problem intensifies because many policies use replacement cost value rather than actual cash value, yet the limit itself hasn’t been updated to reflect current market conditions. You need to verify your dwelling limit against actual rebuilding costs in your specific area, not against what your policy cost when you purchased it. Contact a local contractor, request a detailed rebuild estimate, and compare that number directly to your declaration page. If the gap exceeds 5%, you’re significantly underinsured, and closing that gap should be your immediate priority.

Wildfire Risk Requires Specialized Coverage

Wildfire risk creates a second critical gap that shifts faster than most homeowners realize. Properties in or near high-risk zones require specialized coverage that standard homeowners policies either exclude or severely limit. California’s Sustainable Insurance Strategy now allows catastrophe models to assess wildfire risk more accurately than the 30-year-old methods previously used, which means insurers actively reprice properties based on updated fire exposure data. If your home falls within a Fire Hazard Severity Zone or if nearby fires have expanded evacuation perimeters into your area within the past three years, your standard policy may not provide adequate wildfire-related coverage.

The solution involves two components: first, verify your current risk classification through CAL FIRE’s online mapping tools and confirm whether your property qualifies for standard market coverage or whether you need supplemental wildfire protection. Second, if your property requires specialty wildfire coverage, explore options including the California FAIR Plan for basic protection and difference-in-conditions wraps that fill gaps between standard policies and catastrophe coverage.

High-Value Items Need Scheduled Personal Property Coverage

High-value items like fine art, jewelry, collectibles, and expensive electronics represent a third massive gap. Standard homeowners policies cap personal property coverage at $2,500 to $5,000 total for all specialty items combined, yet a single inherited necklace or art collection often exceeds this limit substantially. Scheduled personal property endorsements cost remarkably little (typically $50 to $150 annually per item) but provide full replacement coverage without depreciation. If you own valuables worth more than $5,000, you’re almost certainly missing critical coverage unless you’ve specifically added scheduled endorsements to your policy.

Final Thoughts

Skipping your annual policy review costs far more than the hour it takes to complete one. Homeowners who neglect this step face underinsurance gaps that result in tens of thousands of dollars in uncompensated losses after a claim. A single major loss without adequate coverage wipes out years of premium payments and leaves you responsible for reconstruction costs that exceed your policy limits.

We at Cappuccino Insurance Agency partner with you to identify coverage gaps before they become financial disasters. Our team works with multiple carriers across California, which means we find solutions for properties that standard insurers reject, including hard-to-place wildfire-risk homes through the California FAIR Plan and difference-in-conditions wraps. Your free coverage assessment removes the guesswork from protection by reviewing your dwelling limits against current rebuild costs, verifying your wildfire risk classification, and identifying specialty coverage gaps.

Contact Cappuccino Insurance Agency today to start your California annual policy review. One conversation now prevents costly surprises later, and many clients discover they can lower premiums while increasing coverage at the same time.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.