Auto Insurance Pricing Options: How to Compare Quotes

Auto insurance pricing options vary wildly from one company to the next, and most drivers have no idea why. The difference between a cheap quote and an expensive one often comes down to factors you can control.

We at Cappuccino Insurance Agency help drivers cut through the confusion and find coverage that actually fits their budget. This guide walks you through comparing quotes side by side, spotting the discounts you qualify for, and making smart adjustments that lower your costs.

What Makes Your Insurance Quote Different From Everyone Else’s

How Insurers Build Your Premium

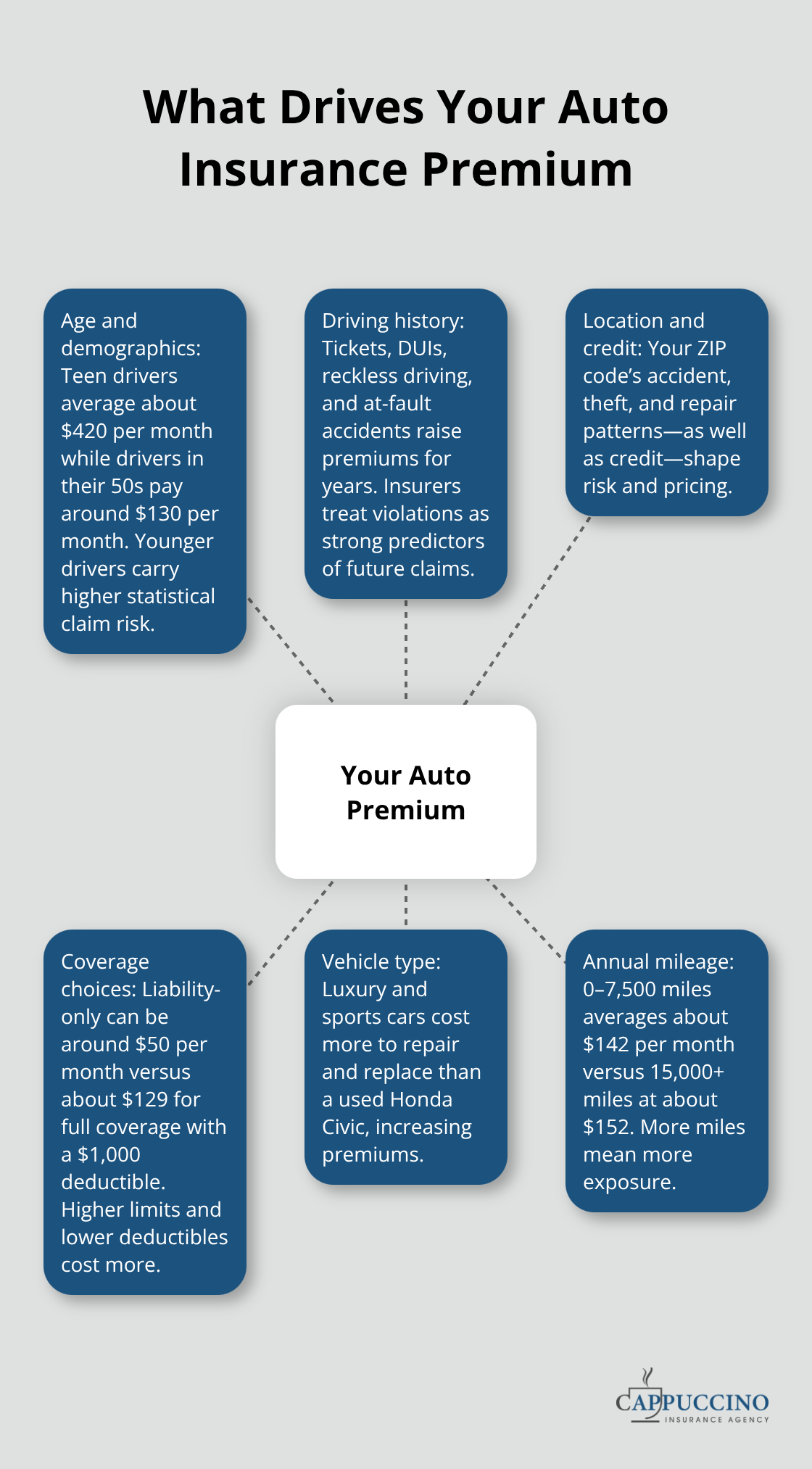

Your premium starts with a broad calculation that insurers narrow down to your specific situation. Insurers estimate the cost of future claims across groups of similar drivers, then adjust that baseline rate for factors unique to you. A 25-year-old driver in Los Angeles pays a fundamentally different amount than a 55-year-old in a rural area, even with identical coverage levels, because the data shows they face different accident and claim risks. Age alone creates massive variation: teen drivers average about $420 per month while drivers in their 50s pay around $130 per month, according to Insurify data. This isn’t arbitrary-it reflects actual claims history and statistical risk.

Driving History and Violations

Your driving history acts as the biggest lever on your premium. A single speeding ticket can push your six-month cost up by roughly $1,378, a DUI by about $2,133, and reckless driving by approximately $2,006. An at-fault accident adds around $434 to your six-month premium compared to a clean record. These increases persist because insurers view violations and accidents as strong predictors of future claims. One poor decision on the road can affect your rates for years.

Location, Credit, and Coverage Choices

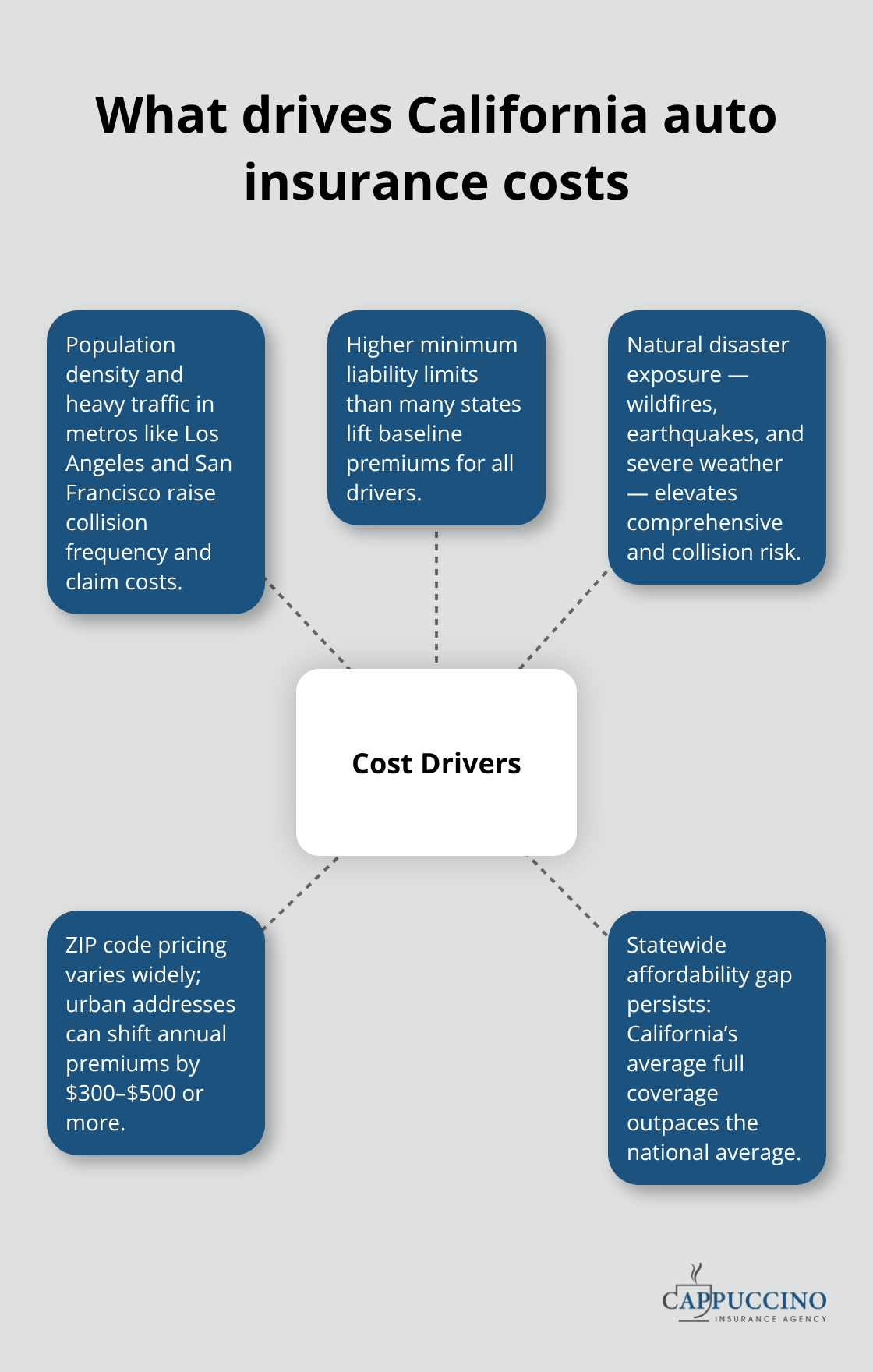

Location matters intensely because your ZIP code captures local accident rates, theft statistics, and repair costs. Michigan drivers pay well above the national average due to no-fault insurance laws with unlimited personal injury protection, while rural areas typically cost less than dense urban neighborhoods. Your credit score influences the final number as well. Coverage choices amplify these differences significantly: switching from liability-only at around $50 per month to full coverage with a $1,000 deductible jumps the cost to approximately $129 per month.

Vehicle Type and Mileage

Vehicle type creates another layer of variation because repair and replacement costs differ wildly-a used Honda Civic costs far less to insure than a luxury sedan or sports car. Annual mileage shifts the calculation too: drivers covering 0–7,500 miles yearly average about $142 per month, while those driving 15,000+ miles annually average about $152 per month. Each factor compounds the others, and the insurer’s algorithm weights them based on their predictive power for claims. Two quotes from the same company for seemingly similar situations can differ by hundreds of dollars because these variables interact in complex ways.

Understanding why your quote looks different from your neighbor’s quote prepares you to spot opportunities for savings. The next section shows you how to gather multiple quotes and compare them fairly so you can identify which insurer offers the best value for your specific risk profile.

How to Compare Quotes Without Wasting Your Time

Gather Quotes From Multiple Carriers

Gathering quotes from multiple carriers is non-negotiable if you want to find genuine savings. Most drivers stop after one or two quotes and assume they’ve done their homework, but that approach leaves money on the table. Insurify’s research shows you can save up to $1,100 annually just by shopping around, and that figure only works if you compare real options. Request quotes from at least 3–5 different insurers to capture meaningful price variation. Rates differ substantially between carriers even for identical drivers and vehicles. A 30-year-old woman with good credit might pay $128 per month for full coverage at State Farm but $298 per month at Liberty Mutual, according to Florida pricing data. That $170 monthly gap translates to over $2,000 per year in unnecessary expense if you pick the wrong company. Request quotes online or contact carriers directly, and don’t settle for estimates based on incomplete information.

Request Identical Coverage Across All Quotes

The second mistake drivers make is comparing apples to oranges. One quote might include $250,000 liability limits while another shows $100,000, making the price comparison meaningless. You must request identical coverage limits and deductibles across every single quote so you’re actually measuring which insurer prices your specific risk lowest. If you’re unsure what coverage levels make sense for your situation, local independent agents can help you determine the right protection before you start comparing. Once quotes arrive, organize them in a spreadsheet or document that shows the insurer name, monthly premium, coverage limits, deductible amounts, and any available discounts you qualify for.

Track Discounts and Price Changes

Track which discounts each carrier offers because discounts vary widely and can shift the final price dramatically. Some insurers heavily reward bundling auto with home or renters insurance, while others emphasize safe driver discounts or telematics programs that monitor your driving habits. Your spreadsheet becomes the decision tool that prevents you from overlooking a cheaper option buried in the fine print. Set up price-drop alerts through platforms that monitor rate changes, because your quote today might not hold at renewal, and carriers occasionally lower rates for existing customers. Check your organized quotes monthly during the renewal window to catch any unexpected increases before your policy renews.

The data you’ve collected now positions you to identify which carriers offer genuine value for your profile. The next step involves spotting the discounts you actually qualify for and making strategic adjustments that lower your costs without sacrificing protection.

How to Cut Your Premium Without Sacrificing Coverage

Stack Discounts Through Policy Bundling

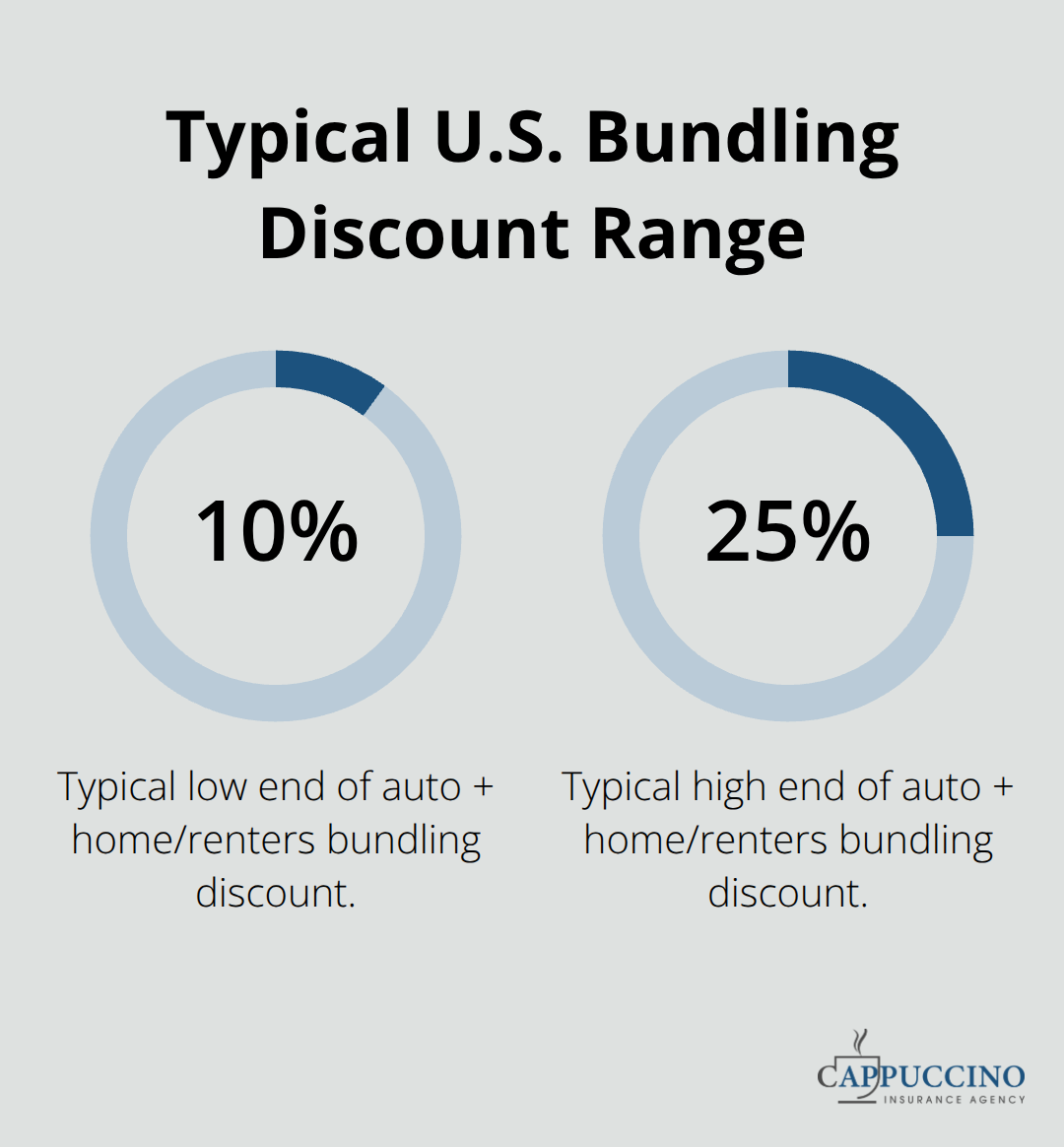

Bundling auto with home or renters insurance remains the single most effective way to lower your costs, and the savings are substantial. State Farm, Allstate, and Nationwide lead the market in bundling discounts, though virtually every major carrier offers them. The discount typically ranges from 10–25% depending on the insurer and your specific policies, which means a driver paying $150 monthly for auto alone could drop that to $120–135 after adding a renters or homeowners policy. Insurers view multi-policy customers as lower risk and more loyal, so they reward consolidation with real money. Before you assume you need to consolidate everything with one company, request bundled quotes and compare them against standalone auto quotes from competitors.

Sometimes a cheaper standalone auto policy from one carrier plus a renters policy elsewhere beats a bundled offer from another, so the spreadsheet you built in the previous section becomes essential here. Don’t let bundling convenience override actual savings.

Claim Low-Mileage and Safety-Feature Discounts

Low-mileage and safety-feature discounts offer real money but require you to actively claim them. Drivers covering 0–7,500 miles annually qualify for low-mileage discounts at most carriers, yet many never mention their actual driving patterns during the quote process. If you work from home, use public transit, or are retired, your mileage is almost certainly lower than the default assumption, which means you’re overpaying. Safety features like airbags, anti-lock brakes, daytime running lights, and anti-theft devices reduce your premium by lowering the insurer’s repair and theft risk. Telematics programs that monitor your actual driving behavior can yield savings if you’re a safe driver, though results vary by program and insurer. Progressive Snapshot and State Farm Drive Safe & Save are the most established options available.

Review Your Policy Annually and Adjust Coverage

Annual policy reviews matter because your situation changes and so do insurance rates. A promotion you qualified for last year might have expired, or your vehicle safety features might unlock a new discount after a recent model update. Review your policy every 12 months and request updated quotes from at least two competitors to confirm you’re still getting competitive pricing. Rates shift constantly, and carriers occasionally lower prices for existing customers without notifying them, so active comparison prevents you from drifting into an overpriced policy year after year. Check your organized quotes monthly during the renewal window to catch any unexpected increases before your policy renews.

Final Thoughts

Finding the right auto insurance pricing options requires discipline and comparison, but the effort pays off immediately. You now understand why quotes differ between carriers, how to gather apples-to-apples comparisons, and where to find discounts that actually reduce your costs. The spreadsheet approach works because it forces you to track real numbers instead of relying on memory or gut feeling.

Your next move is straightforward: gather quotes from at least three to five carriers using identical coverage limits, organize them in a document, and identify which insurer offers the best combination of price and service for your specific situation. Rates shift constantly, and carriers occasionally lower prices without telling you, which means your renewal notice might hide a better deal if you shop around. Set a calendar reminder for your renewal date and request updated quotes from at least two competitors every 12 months to prevent rate creep.

We at Cappuccino Insurance Agency understand that comparing quotes feels overwhelming, which is why we offer free coverage assessments to help you navigate your options. As an independent agency partnering with multiple carriers across California, we can show you several quotes side by side and identify bundling opportunities you might miss on your own. Contact us today for a free assessment and discover how much you could save by comparing your auto insurance pricing options properly.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.