Landlord Property Insurance Requirements: Meeting California Standards

California landlord property insurance requirements aren’t optional-they’re the foundation of protecting your investment and staying compliant with state law. Whether you own a single-family rental or a multi-unit complex, understanding what coverage you actually need makes the difference between adequate protection and costly gaps.

At Cappuccino Insurance Agency, we help landlords navigate these requirements without overpaying. This guide breaks down the specific standards California demands and shows you how to meet them efficiently.

What Coverage Limits Do California Landlords Actually Need

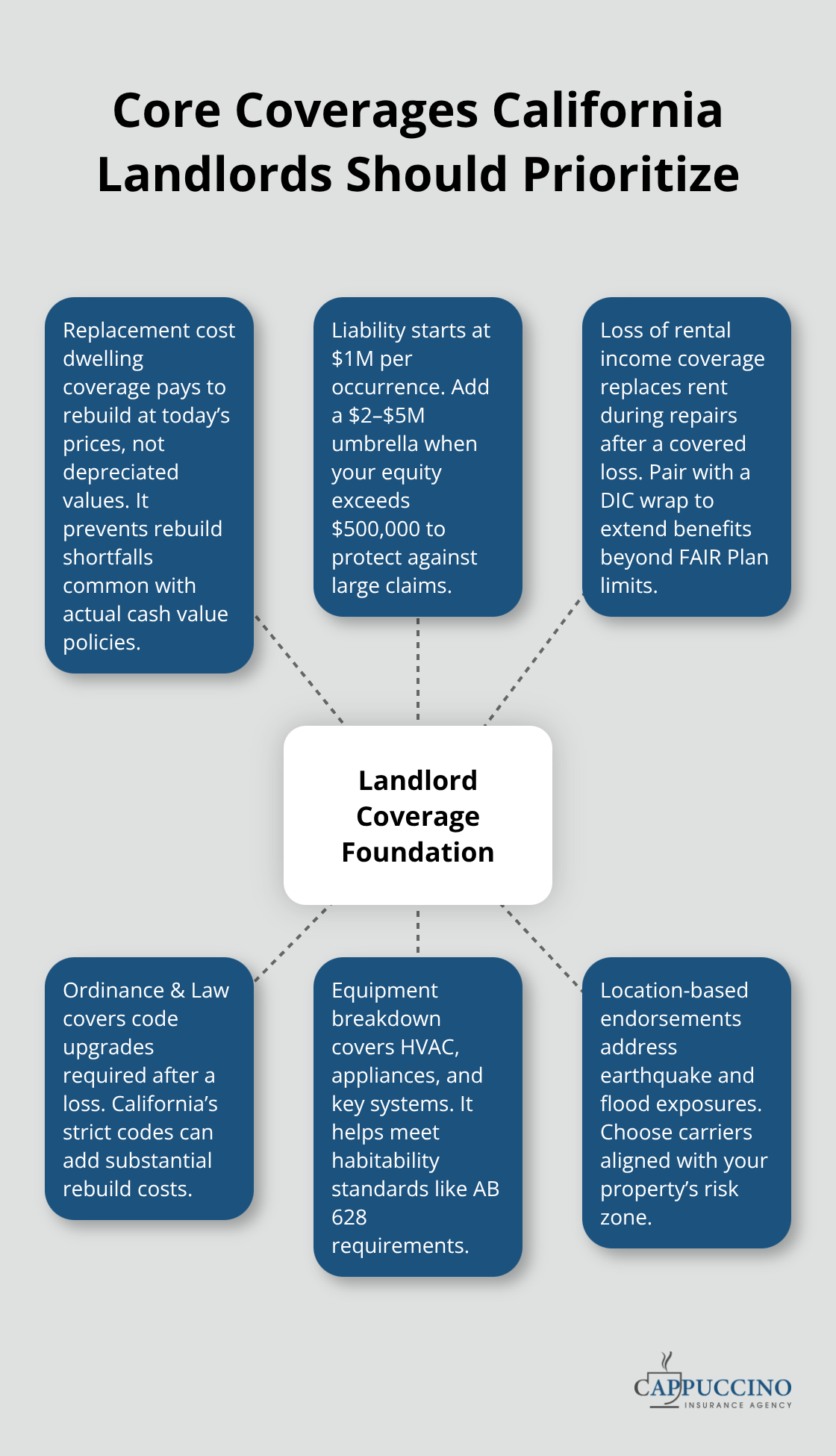

Landlord insurance in California costs about $1,700 per year in 2026, though wildfire-exposed properties jump to $2,000–$3,500 or higher depending on their specific fire hazard zone. The real issue isn’t just picking a number-it’s matching your coverage to replacement cost, not market value. A house worth $800,000 on the market might cost $1.2 million to rebuild after a total loss due to current labor and material prices in California. Standard policies default to actual cash value, which pays depreciated amounts and leaves you short when rebuilding.

You need replacement cost coverage instead, and many landlords still miss this distinction.

Liability and Income Protection Form Your Safety Net

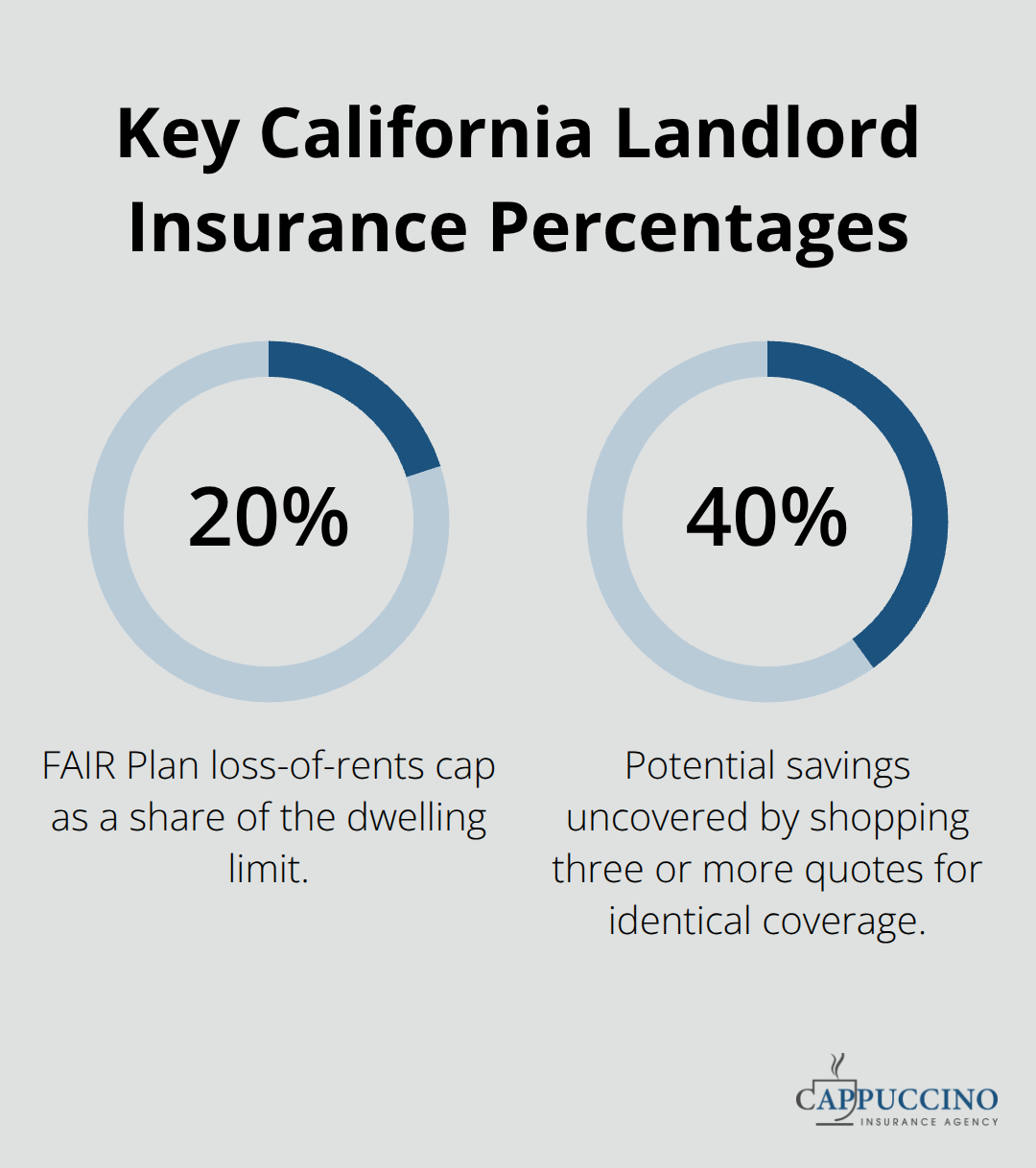

For liability, start with a minimum of $1 million in coverage per occurrence; if your property equity exceeds $500,000, add an umbrella policy of $2–$5 million to cover tenant injuries or lawsuits that exceed your base limit. Loss of rental income coverage matters more than most landlords realize-it reimburses you when a covered loss makes the property temporarily uninhabitable. The California FAIR Plan caps this at 20% of your dwelling limit, which often falls short for properties with high monthly rents. Pair FAIR Plan coverage with a Difference in Conditions (DIC) wrap to fill gaps and protect your income during repairs.

Single-Family Properties Require Strategic Endorsements

Beyond the base policy, add equipment breakdown coverage for HVAC systems and appliances since California’s new AB 628 requirement starting 2026 mandates working stoves and refrigerators as habitability standards. Ordinance and Law endorsements cover the cost of upgrading to current building codes after a loss-California’s code requirements are strict and often exceed the original construction cost. If your property sits in a high fire hazard zone, document any wildfire mitigation steps like defensible space maintenance or roof upgrades, as these earn credits from insurers that can reduce premiums by 10–15%.

Larger Properties and High-Value Homes Demand Specialized Coverage

For multi-unit properties or those worth over $1 million, carriers like Chubb and PURE offer higher limits and specialized wildfire defense consultations that justify the premium difference. Shopping three or more quotes reveals pricing gaps up to 40% for identical coverage, so never accept the first quote. Condo rentals operate differently-if you own a condo, your HOA master policy may reduce your individual landlord insurance costs, but verify what gaps remain uncovered before assuming you’re protected. Multi-family properties with five or more units cost 0.4–0.8% of replacement value annually and require additional liability layers for larger portfolios.

Location-Based Risk Shapes Your Coverage Strategy

High-risk properties in coastal areas or burn-scar zones face surcharges and carrier restrictions, making it essential to disclose location details accurately to avoid claim denial later. These location factors also determine which carriers will even quote your property and what additional protections you’ll need to fill coverage gaps.

What Coverage Gaps Cost California Landlords

Loss of Rental Income Falls Short Without Supplemental Protection

Most California landlords discover their coverage gaps only after a loss occurs, and by then it’s far too late. The standard landlord policy covers the structure and your liability, but it leaves critical income and natural disaster exposures unprotected. Loss of rental income coverage ranks as the most misunderstood protection available, yet it separates landlords who weather a six-month repair period from those facing financial collapse. When fire or major wind damages your property, tenants vacate and rent stops flowing immediately. Your mortgage, property taxes, and maintenance costs continue regardless of repairs. Standard landlord policies limit loss of rents to 20% of your dwelling coverage through the California FAIR Plan, which translates to roughly $4,000–$8,000 annually for most single-family rentals.

That cap barely covers two months of lost rent on a $2,000-per-month property. Pairing FAIR Plan coverage with a Difference in Conditions (DIC) wrap fills the income gap and extends your benefit period up to 12 months. Without this supplemental protection, you’re betting your cash reserves against a covered loss.

Liability Exposure Escalates With Tenant Occupancy

Liability exposure rises sharply with tenant occupancy and visitor activity. California’s tenant protection laws create a complex legal environment where you face heightened exposure to injury claims, discrimination disputes, and habitability violations under AB 1482. A single lawsuit from a tenant or guest injured on your property can exceed your base $1 million liability limit within weeks of discovery. Coastal properties and those in high-density neighborhoods face even greater exposure due to increased foot traffic and premises liability risk. Umbrella policies starting at $2–$5 million become essential once your property equity exceeds $500,000, yet most landlords skip this layer and expose themselves unnecessarily to catastrophic claims.

Water Damage and Earthquake Coverage Require Separate Endorsements

Water damage and natural disaster coverage demands equal attention because standard policies exclude flood and earthquake entirely. Wildfire mudslides in burn-scar zones differ from traditional flood coverage, meaning a hillside property damaged by post-fire debris flow may not trigger your flood policy. Earthquake coverage must be added separately through the California Earthquake Authority at typical deductibles of 5–25% of your dwelling limit, costing roughly $35–$100 annually depending on your coverage level. Properties within Very-High Fire Hazard Severity Zones should document wildfire mitigation investments like roof upgrades, defensible space maintenance, and ember-resistant vents (these improvements earn carrier discounts of 10–15% that offset the cost of supplemental earthquake and flood endorsements). Understanding these gaps positions you to address them before a loss exposes your financial vulnerability.

Cutting Your Landlord Insurance Costs Without Sacrificing Protection

Compare Multiple Carriers to Reveal Hidden Savings

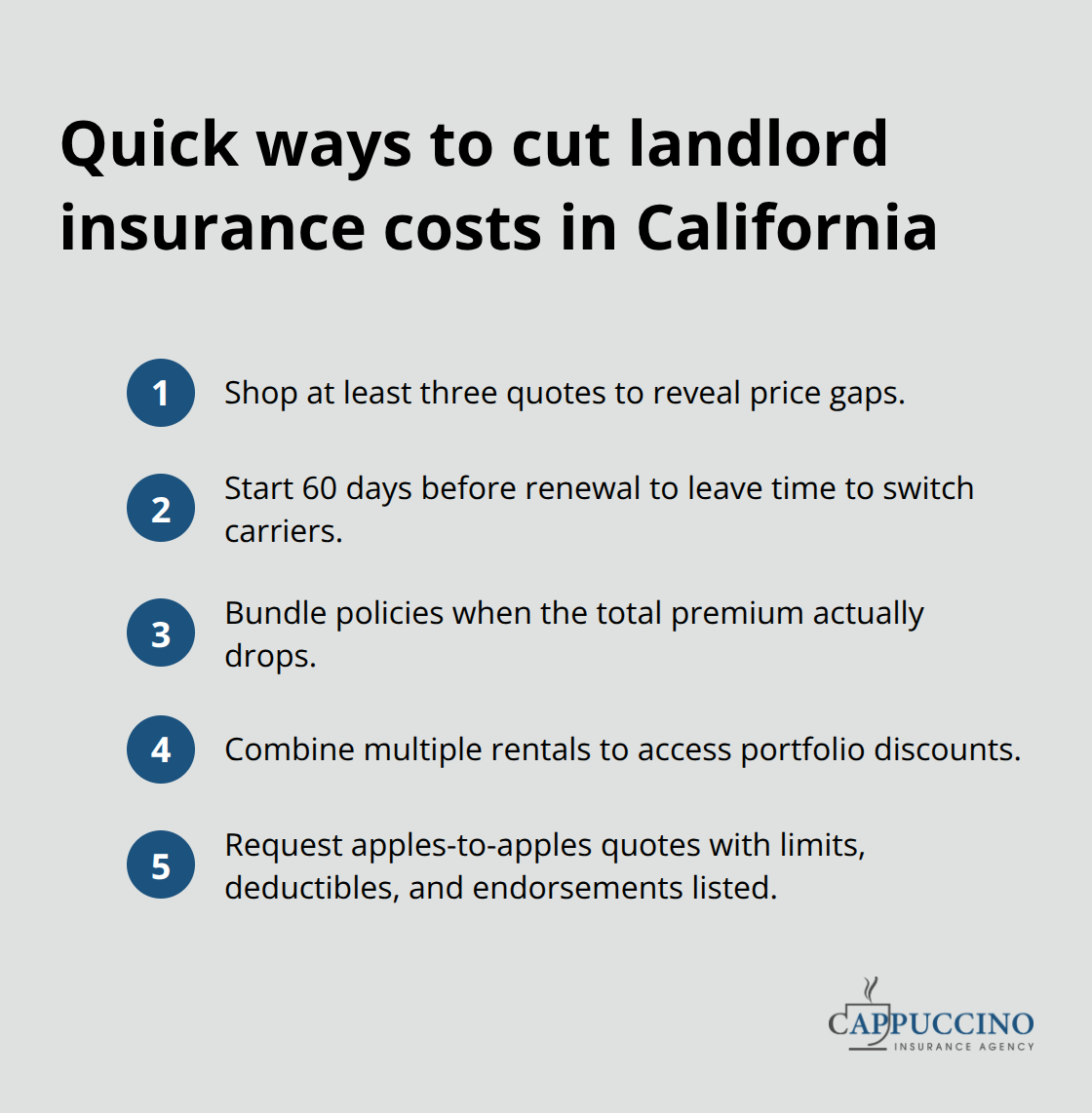

Bundling your landlord policy with auto, home, or other coverage through a single carrier can provide savings, though the savings vary by insurer and your specific risk profile. The mistake most landlords make is accepting the first bundled quote without shopping alternatives-a property owner paying $2,200 annually through one carrier’s bundle might pay $1,680 through a competitor offering the same coverage limits and deductibles. Shopping three or more quotes takes roughly two hours and reveals pricing gaps up to 40% for identical protection. Start 60 days before your renewal date so you have time to evaluate options and switch carriers if the savings justify the administrative effort. Multi-property portfolios gain even larger discounts when you combine multiple rentals together, sometimes reaching 15–30% savings depending on the carrier’s appetite for larger accounts.

Request quotes that specify your dwelling limit, liability coverage, loss of rental income cap, and any endorsements like Ordinance and Law or equipment breakdown so you compare apples to apples across carriers. Document your current coverage details before you shop-most agents can retrieve this from your renewal notice, but having it ready accelerates the quoting process.

Work With Local Agents to Address Coverage Gaps

A local independent agent reviews your policy for occupancy classification accuracy, wildfire-zone coverage challenges, and supplemental protections like Difference in Conditions wraps that fill California FAIR Plan gaps. At Cappuccino Insurance Agency, we partner with 20+ carriers across California, which means we compare bundled rates from multiple providers rather than locking you into one carrier’s discount structure. This approach reveals savings opportunities that single-carrier agents cannot access. An agent familiar with your local market understands which carriers actively write in your fire hazard zone and which ones restrict new business, saving you time on quotes from carriers that won’t cover your property anyway.

Schedule Annual Reviews Before Renewal Deadlines

Annual policy assessments should happen 90 days before renewal, not at renewal itself, so you have time to address underinsurance before your policy lapses. Request a detailed coverage review that compares your current dwelling limit against current replacement costs in your area-California construction costs have risen 12–18% annually in recent years, meaning a limit that was adequate two years ago may now cover only 70–80% of actual rebuilding expenses. If your property has appreciated significantly or you’ve made major improvements like a roof replacement or foundation upgrade, notify your agent immediately so these investments are reflected in your coverage limit and earn any available mitigation discounts. The California Department of Insurance recommends updating replacement cost estimates annually through a qualified contractor estimate rather than relying on inflation adjustments alone, especially in high-cost coastal or urban markets where labor rates spike unpredictably.

Document Wildfire Mitigation Work to Earn Premium Credits

Properties in Very-High Fire Hazard Severity Zones should document wildfire mitigation work with photos and contractor invoices because carriers offer 10–15% premium reductions for defensible space maintenance, roof upgrades to Class A materials, and ember-resistant vents. These credits often offset the cost of adding earthquake or flood endorsements, making your total protection more affordable than it appears at first glance. Schedule your annual review for late August or early September so any coverage changes take effect well before the October fire season when carriers tighten underwriting standards and some restrict new business in high-risk zones.

Final Thoughts

California landlord property insurance requirements protect both your investment and your tenants, yet most landlords treat coverage as a checkbox rather than a strategic asset. Replacement cost dwelling coverage matching actual rebuild expenses, liability protection starting at $1 million per occurrence, loss of rental income coverage paired with a Difference in Conditions wrap, and location-specific endorsements for earthquake or flood exposure form the foundation of financial security when a covered loss strikes. Annual policy reviews 90 days before renewal catch underinsurance before it becomes a problem, while shopping multiple carriers reveals savings up to 40% for identical coverage.

Proactive coverage planning separates landlords who recover quickly from those facing months of financial strain. Documenting wildfire mitigation work earns premium credits that offset the cost of supplemental protections, making comprehensive coverage more affordable than it appears. Bundling multiple properties or pairing your landlord policy with auto and home coverage through a single carrier generates additional discounts that compound over time.

The next step involves scheduling a coverage assessment with an agent who understands California’s unique risks and carrier landscape. We at Cappuccino Insurance Agency partner with 20+ carriers across California, which means we compare rates from multiple providers rather than locking you into one carrier’s pricing structure. Contact us today to request your assessment and secure the protection your rental property actually needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.