Westlake Village Insurance Agency: Your Local Independent Agent Advantage

Westlake Village residents face unique insurance challenges, from wildfire exposure to specific local driving conditions. Finding the right coverage at the right price requires more than a generic online quote.

At Cappuccino Insurance Agency, we work with 20+ carriers to build protection that actually fits your life. An independent Westlake Village insurance agency gives you access to options and expertise that big national companies simply can’t match.

Why Independent Agents Deliver Real Value in Westlake Village

Local Knowledge Protects You from Coverage Gaps

Westlake Village sits in one of California’s highest-risk zones for wildfire, earthquake, and flood exposure. The Insurance Information Institute reports that homeowners insurance costs in California have risen significantly due to higher rebuilding costs and labor expenses. When you call a national insurer’s 1-800 number, a representative reads from a script without ever seeing your neighborhood, knowing that your street floods during heavy rain, or explaining why your premium jumped 30% year-over-year. An independent agent in Westlake Village knows your community because they live here.

They understand which carriers actively write in our area, which ones have pulled back due to wildfire exposure, and which ones offer specialized endorsements for earthquake and water backup that standard policies exclude. This matters because local knowledge protects you from coverage gaps in Westlake Village, where insurance gaps expose homeowners to significant risk.

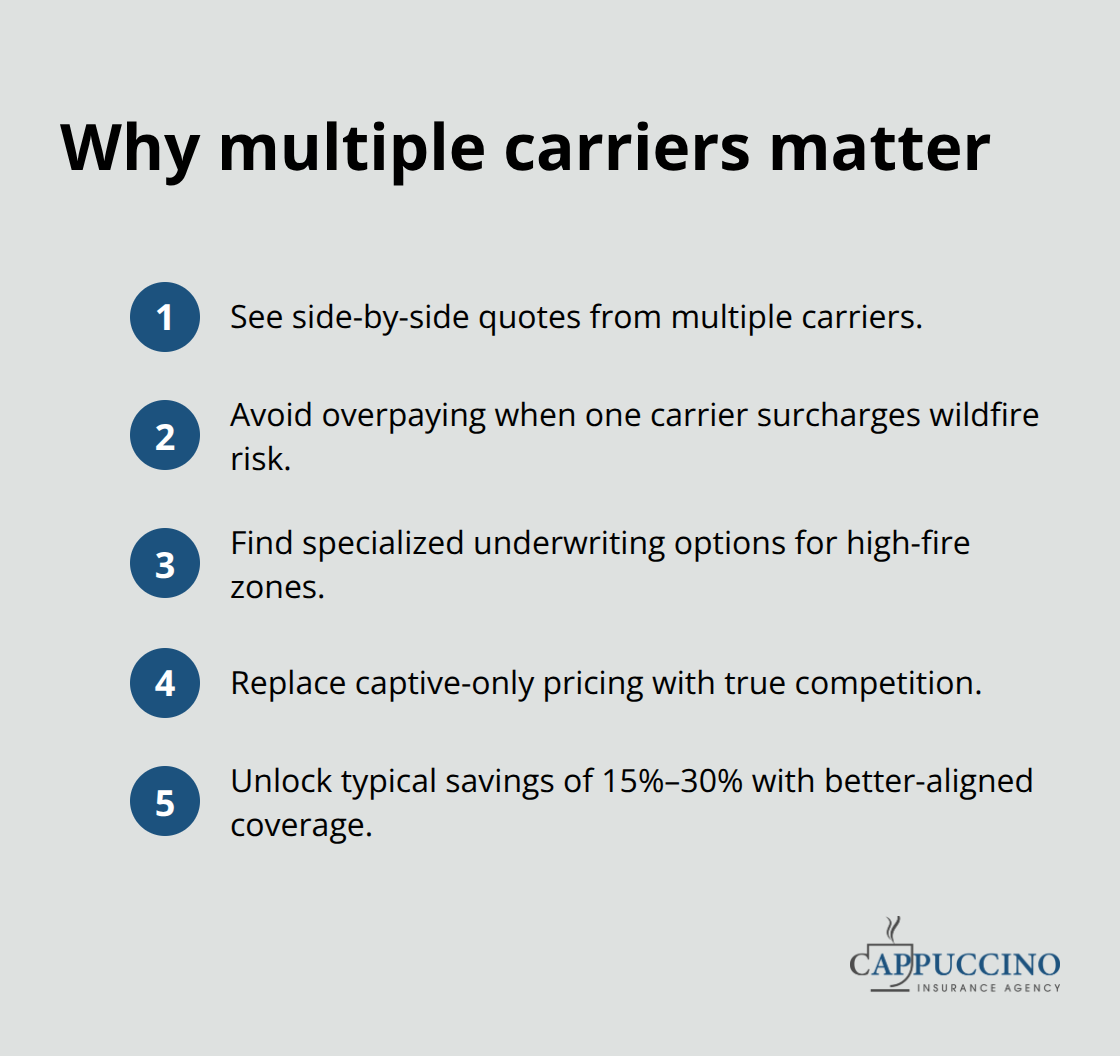

Multiple Carriers Create Real Competition for Your Business

When you work with a captive agent representing a single insurance company, that agent has one solution to offer you-their company’s policy at their company’s rates. An independent agent represents multiple carriers, which means genuine competition works in your favor. A homeowner in Westlake Village shopping for auto insurance might find quotes ranging from $1,200 to $2,100 annually for identical coverage across different carriers-a difference of $900 per year. Without an independent agent comparing those quotes side by side, most people never see the full range of options available to them. The Independent Insurance Agents & Brokers of America notes that independent agents help clients identify the best-value options through multiple quotes, something you cannot get from a direct-to-consumer website or a captive agent. Independent agents represent multiple carriers, which translates to real choices on price, coverage limits, and endorsement options that fit your budget and risk tolerance.

Local Agents Advocate for You During Claims

When a claim happens-a roof damaged by wind, a car totaled in an accident, a business interruption from a fire-you need someone advocating for you, not against you. A local independent agent coordinates with the carrier on your behalf, explains the circumstances, pushes for fair settlement, and keeps you informed throughout the process. National claims departments process thousands of claims monthly and operate on standard timelines. A local agent knows the adjusters in your area, understands how quickly claims typically move, and flags delays before they become problems. They also know which carriers have strong reputations for claims handling in Westlake Village and which ones have a history of disputes. When you bundle auto, home, and possibly umbrella coverage through one independent agent, claims coordination becomes simpler-one person manages your relationship with the carrier instead of you juggling multiple departments.

Specialty Coverage for Hard-to-Place Properties

Some Westlake Village properties face challenges that standard policies won’t cover. High-value homes, properties in elevated wildfire zones, or homes with unique features (pools, solar panels, luxury vehicles) require specialized solutions. An independent agent accesses carriers that specialize in these hard-to-place risks and knows which endorsements address specific California exposures. This expertise prevents you from buying inadequate coverage or overpaying for unnecessary add-ons. The right agent matches your property’s actual risk profile to the right carrier and policy structure, saving you money while closing protection gaps that could cost thousands after a loss.

How We Give You More Carrier Options and Better Coverage Fits

We at Cappuccino Insurance Agency work with over 20 insurance carriers, which fundamentally changes what’s possible for your coverage. When a captive agent can only offer policies from one company, they’re limited by that insurer’s appetite for risk, their underwriting guidelines, and their pricing strategy. That single-carrier constraint means you get one answer to your insurance problem, not the best answer. Our relationships with 20+ carriers mean we shop your profile across companies with different risk tolerances, different pricing models, and different specialty products.

Multiple Carriers Create Real Competition for Your Business

A homeowner in Westlake Village with a property in a high-fire zone might find that one carrier won’t write the home at all, another charges a 40% premium for wildfire exposure, and a third offers competitive rates through a specialized underwriting team. Without multiple carriers to access, you either overpay or go uninsured. Clients who spent years with a captive agent often paid inflated premiums because their agent had no alternative to offer.

Switching to an independent agency and accessing a full carrier network typically saves clients 15% to 30% on their annual premiums, sometimes more when coverage restructures to better match actual risk profile.

Hard-to-Place Properties Need Specialized Carriers

Properties in Westlake Village frequently fall into categories that mainstream carriers avoid or heavily penalize. High-value homes, properties in wildfire-prone zones, older homes with outdated electrical systems, or houses with swimming pools represent elevated risk under standard underwriting. Rather than accepting rejection letters or sky-high quotes, an independent agent connects you with carriers that specialize in these exact scenarios. For properties that fall outside admitted carrier guidelines, the California FAIR Plan and Difference-in-Conditions coverage wraps layer protection where standard policies won’t. FAIR Plan policies cost roughly 20% to 40% more than standard homeowners insurance, so pairing them with a DIC wrap from a specialty carrier often produces better coverage at a lower total premium than FAIR Plan alone. Knowing which carriers accept which risks and how to structure policies to optimize both price and protection separates an independent agent from someone who can only offer a single company’s standard form.

Annual Reviews Keep Your Coverage Current as Life Changes

Many Westlake Village homeowners buy insurance once and forget about it until a claim happens or their renewal notice arrives with a 20% rate increase. Free coverage assessments and annual policy reviews catch gaps, eliminate overage, and identify rate reductions before your renewal date. During these reviews, replacement-cost coverage verification confirms that your limits still match current rebuilding expenses in Westlake Village, where construction labor and materials have climbed steadily over the past three years. Changes in your risk profile-new additions to your home, increased property values, life events like marriage or children-trigger coverage adjustments. If your neighborhood’s wildfire risk rating has changed or a new carrier with better pricing entered the market, an independent agent knows about it and shops your policy proactively. A homeowner with replacement-cost coverage set at $380,000 when their home would actually cost $520,000 to rebuild faces a $140,000 gap and significant underinsurance. That gap means substantial out-of-pocket costs after a total loss. Annual reviews catch these discrepancies. Bundling opportunities-combining auto, home, and umbrella coverage-yield multi-policy discounts ranging from 10% to 25% depending on the carrier.

Why Coverage Assessments Matter for Westlake Village Residents

The goal of annual reviews is straightforward: pay a fair price for adequate protection, not overpay for unnecessary coverage or underpay and face gaps when you need protection most. Life changes fast in Westlake Village, and your insurance should adapt just as quickly. An independent agent who conducts regular policy reviews catches rate increases before they hit your renewal notice and identifies new coverage options that fit your evolving situation. This proactive approach means you’re never caught off guard by a claim that falls outside your policy limits or a premium spike that could have been prevented. As your circumstances shift-whether through home improvements, vehicle changes, or business growth-your insurance protection should shift with you.

Insurance Protection Tailored to Westlake Village’s Real Risks

Home Insurance Must Address Wildfire and Natural Disaster Exposure

Westlake Village residents face wildfire and natural disaster risks that standard nationwide policies ignore. The Insurance Information Institute reports that California homeowners insurance costs have risen significantly due to higher rebuilding costs and labor expenses, yet many residents still carry inadequate replacement-cost limits or miss endorsements that protect against region-specific losses. Properties in high-fire zones carry standard deductibles of 5% to 10% of the home’s insured value-a $500,000 home faces a $25,000 to $50,000 deductible for fire losses, substantially higher than the $1,000 to $2,500 deductibles most homeowners expect.

Carriers like State Farm and Allstate have reduced or closed their books to new business in California’s highest-risk zones, forcing residents into the California FAIR Plan, which costs 20% to 40% more than standard policies. The solution involves layering coverage: a FAIR Plan policy for basic protection paired with a Difference-in-Conditions wrap from a specialty carrier that covers gaps FAIR Plan excludes. This approach often produces better overall protection at lower cost than FAIR Plan alone.

Replacement-cost coverage must reflect current Westlake Village rebuilding expenses, not estimates from five years ago. Construction labor and materials in Southern California have increased 8% to 12% annually over the past three years, meaning a home with $400,000 in coverage today may need $480,000 within three years to cover a total loss. Annual reviews catch these shortfalls before a loss occurs.

Auto Insurance Addresses Distinct Local Driving Conditions

Westlake Village drivers face high-speed commutes on the 101 Freeway, canyon roads with limited visibility, and seasonal flooding in specific neighborhoods that damage vehicles parked at home. Liability limits of 100/300/100 (the California minimum) provide almost no protection if you cause a serious accident on the freeway, where medical costs and vehicle damage routinely exceed $500,000. Most Westlake Village residents benefit from 250/500/100 liability limits or higher, especially if they have significant assets to protect.

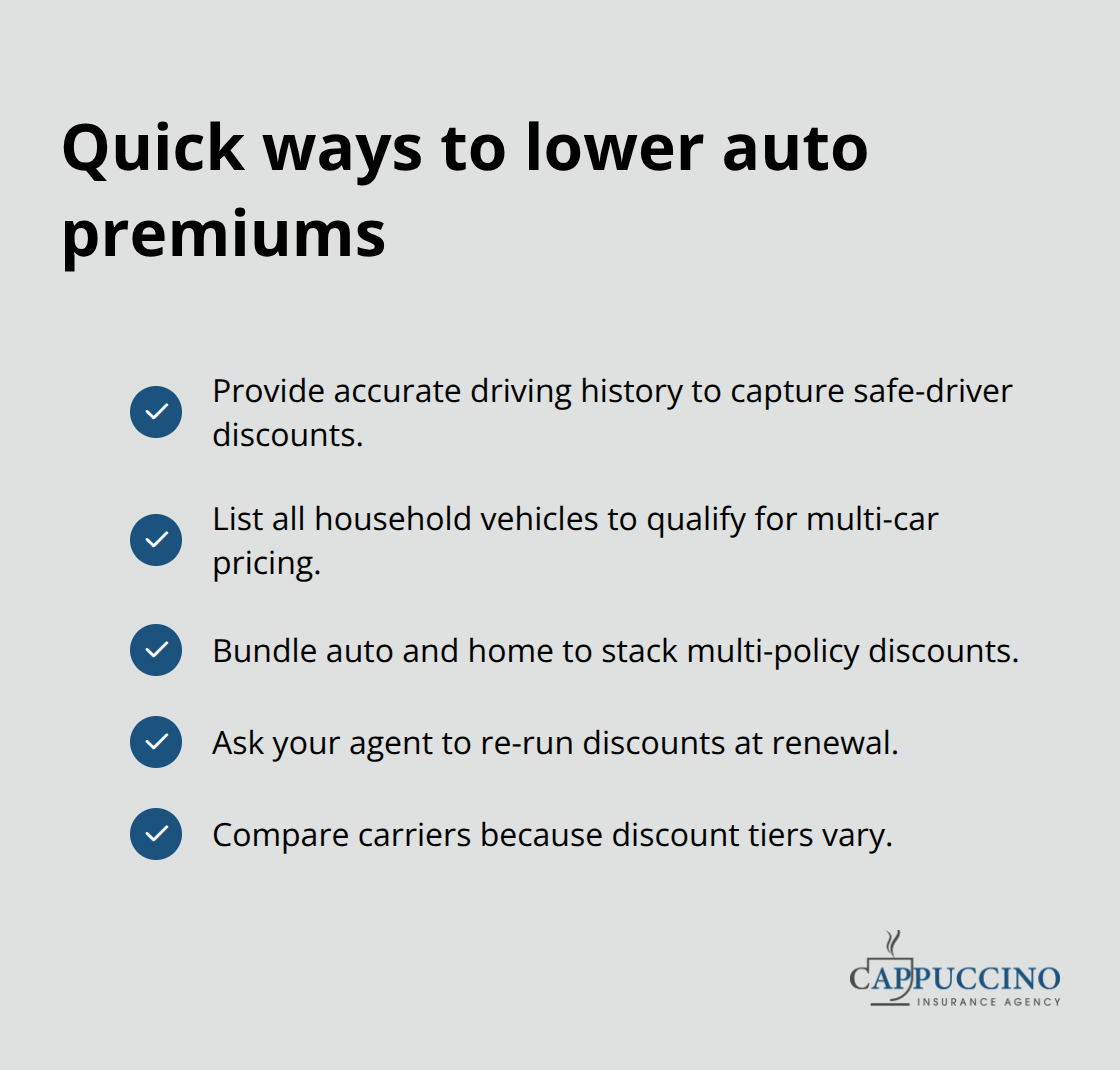

Safe-driver discounts reduce premiums 10% to 25% depending on the carrier, so providing accurate driving history matters when shopping quotes. Multi-car policies yield 15% to 25% discounts, and bundling auto with home insurance through one agent typically adds another 10% to 25% off the combined premium.

Life and Commercial Insurance Complete Your Protection Strategy

Life insurance premiums for a 40-year-old Westlake Village resident in good health range from $35 to $75 monthly for $500,000 in term coverage, making it affordable to protect your family’s mortgage and living expenses. Small business owners in Westlake Village need general liability coverage starting at $1 million per occurrence, plus property coverage for equipment and inventory, and potentially cyber liability if the business handles customer data.

Cappuccino Insurance Agency partners with carriers that specialize in each of these categories, allowing us to match your specific Westlake Village situation to the right insurance options and price rather than forcing you into one-size-fits-all solutions that national insurers promote.

Final Thoughts

Westlake Village residents who’ve spent years paying inflated premiums or fighting with national insurers over claims quickly realize that local expertise delivers measurable value. An independent agent working with multiple carriers saves you money on your annual premium while handling quote comparisons, claims coordination, and policy adjustments that would otherwise fall on you. They also protect you from coverage gaps that could cost tens of thousands after a loss.

Choosing an independent agent over a captive agent or direct-to-consumer option means you work with someone who understands Westlake Village’s specific risks, knows which carriers actively write in our area, and can access specialty solutions when standard policies won’t cover your property. A homeowner who switches from a captive agent to a Westlake Village insurance agency typically saves 15% to 30% on premiums while actually improving their coverage. A small business owner gains access to carriers specializing in their industry rather than accepting whatever a single company offers.

Contact Cappuccino Insurance Agency to schedule a free coverage assessment and see how working with a local independent agent changes what’s possible for your insurance protection and budget. We partner with 20+ carriers to deliver home, auto, life, and commercial insurance tailored to your situation and provide annual policy reviews to catch rate increases and coverage gaps before they become problems. We offer 24/7 support when you need answers.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.