Difference in Conditions Policies: Expanding Coverage for Hard-To-Place Risks

Some properties are nearly impossible to insure through standard channels. Unusual construction, high-risk locations, or unique exposures leave owners scrambling for protection.

Difference in Conditions policies fill this gap by providing secondary coverage where traditional insurance won’t. At Cappuccino Insurance Agency, we help property owners secure the protection they need, even when conventional options fall short.

What Difference in Conditions Policies Actually Cover

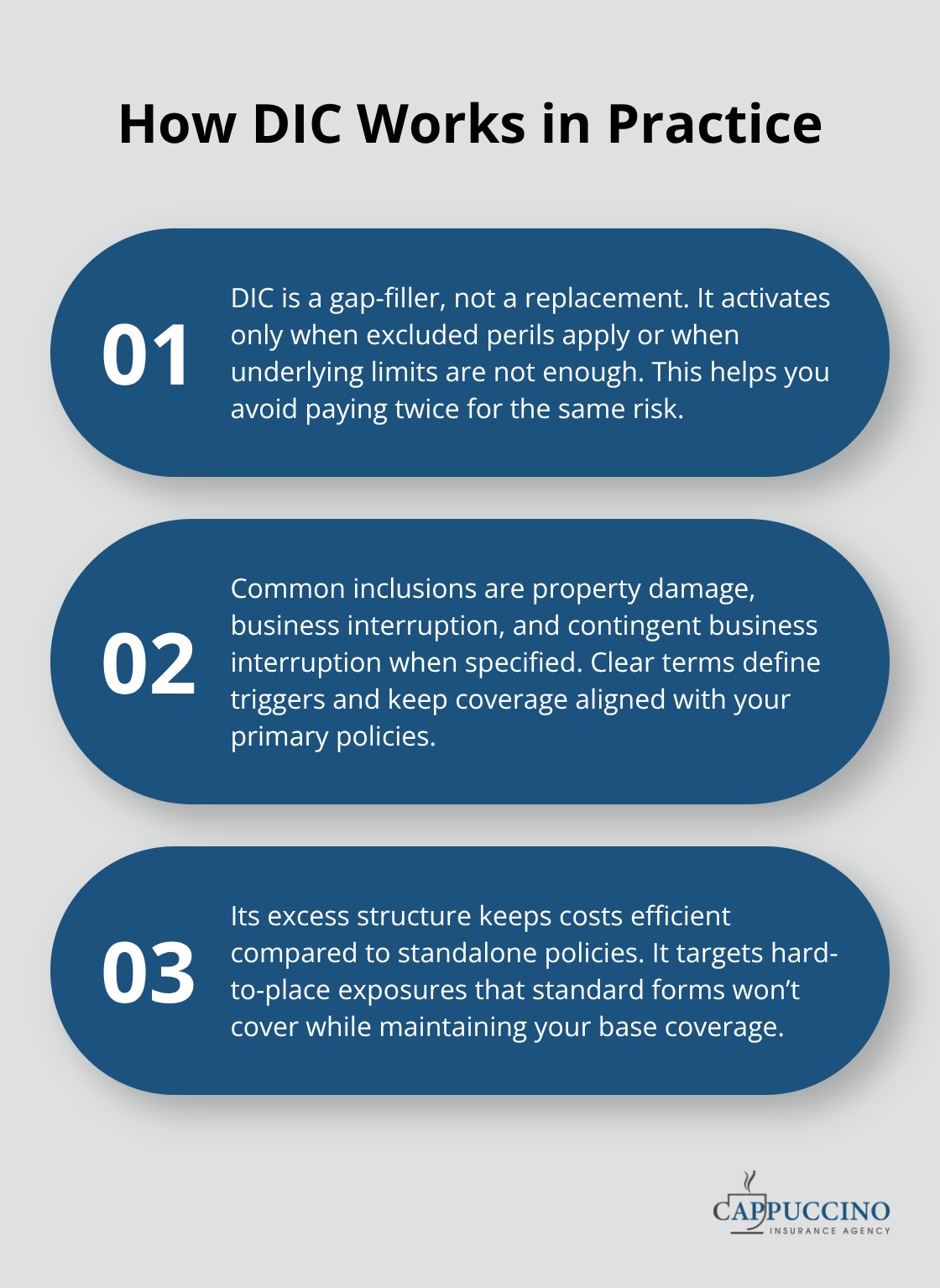

A Difference in Conditions policy sits on top of your existing insurance and covers what your primary policies don’t. It’s not a replacement-it’s a gap-filler. When standard property insurance excludes certain perils, limits coverage to specific locations, or caps payouts below your actual exposure, DIC steps in to bridge that shortfall. The Insurance Information Institute reports growing interest in DIC as climate risk and supply chain complexity drive demand for more flexible risk transfer. This matters because the gap between what you think you’re protected against and what you actually are can be substantial. DIC policies typically cover property damage, business interruption, and contingent business interruption if specified in the contract. The key distinction is that DIC only pays when your underlying policies don’t-it operates as excess coverage, not primary coverage. This structure means lower premiums than purchasing standalone policies while still addressing hard-to-place exposures that standard forms simply won’t touch.

How DIC Differs from Standard Insurance

Traditional property insurance works with broad exclusions baked into the policy language. Flood, earthquake, wear and tear, and certain types of equipment damage are commonly excluded. DIC flips this approach: it covers named perils that your underlying policy excludes, provided those perils are specifically listed in the DIC endorsement. A comprehensive gap analysis before purchasing DIC identifies exactly what the underlying policies do not cover. Underwriting factors including location risk, construction type, occupancy, asset value, and exposure growth all influence DIC pricing and limits. This means a historic property in a flood zone pays differently than a modern warehouse in a low-risk area. DIC doesn’t replace primary coverage-it expands protection without duplicating what’s already in place. You maintain your standard policies with their deductibles and limits intact. The DIC then responds only after those policies are exhausted or when excluded perils occur. This layered approach prevents paying twice for the same protection while ensuring no exposure slips through uninsured.

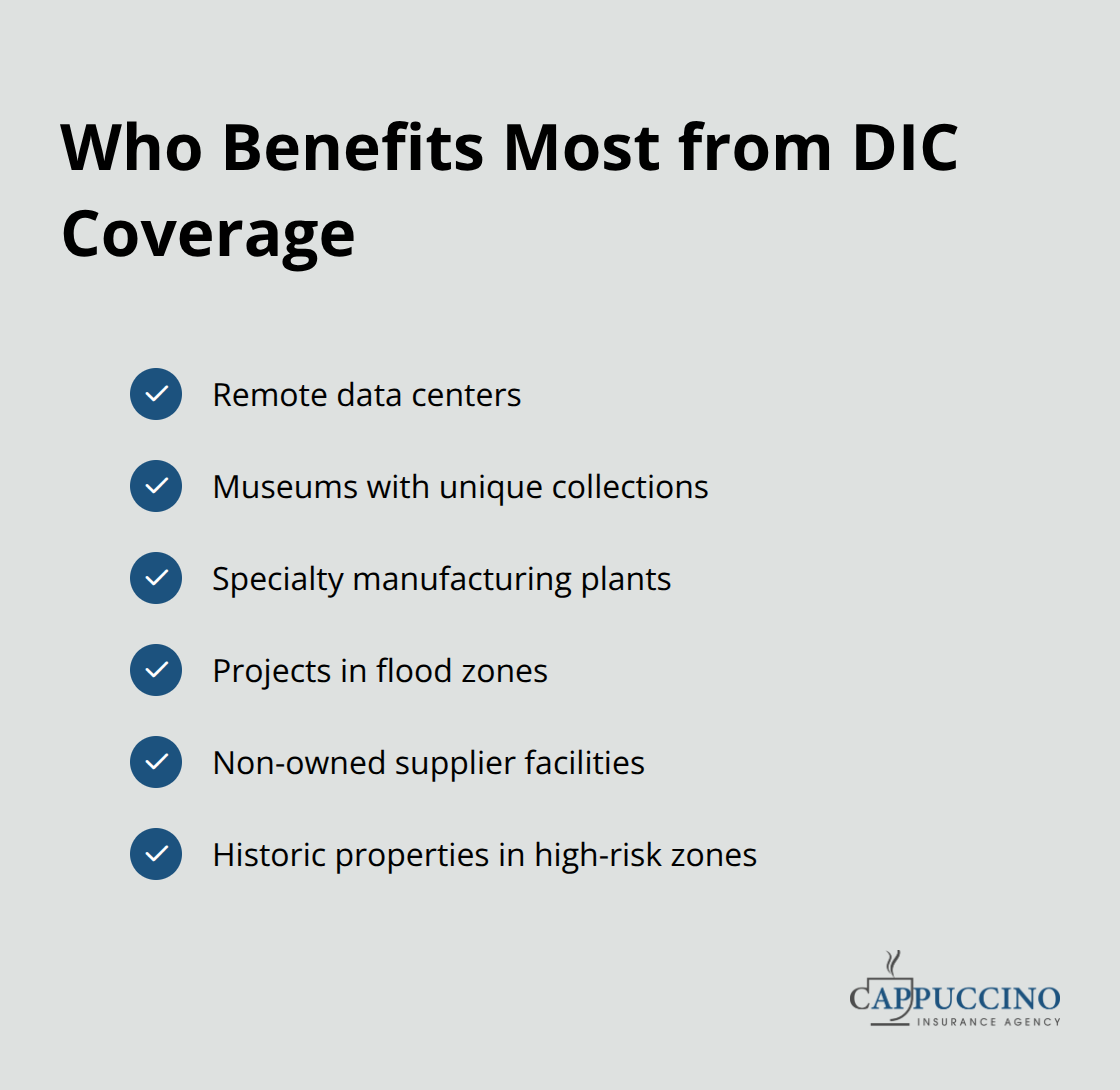

Where DIC Closes Real Coverage Holes

Non-owned properties present a common problem that DIC solves directly. If your business operates from multiple locations or relies on supplier facilities, your primary policy may exclude damage at those off-site locations. DIC can extend protection to non-owned properties if specified in the endorsement. Remote data centers, museums, specialty manufacturing plants, and projects in flood zones all benefit from DIC because standard carriers either decline them outright or impose severe restrictions. The policy language may include sublimits, deductibles, and coinsurance terms that require careful alignment with underlying policy terms and restoration needs. Brokers play a central role in designing DIC programs and coordinate with primary carriers to avoid gaps or overlaps. We conduct detailed exposure reviews to identify exactly which perils and locations need additional protection, then structure DIC coverage to fill those specific holes rather than purchasing blanket excess coverage that wastes premium dollars.

What Happens Next in Your DIC Journey

The transition from identifying coverage gaps to securing DIC protection requires a strategic assessment of your current policies and exposure profile. Your next step involves working with an experienced insurance partner who understands both your underlying coverage and the specific perils that standard forms exclude. This foundation sets you up to explore how DIC can address your hard-to-place risks and what the actual implementation process looks like.

Why Standard Insurance Fails Hard-To-Place Properties

The Cookie-Cutter Problem

Properties that fall outside conventional underwriting parameters face a brutal reality: standard carriers either reject them outright or impose such severe restrictions that coverage becomes economically useless. A historic mansion in a flood zone, a data center in a remote location, a specialty manufacturing facility with outdated equipment, or a museum housing irreplaceable assets all share one problem. Their risk profiles don’t fit the templates that drive traditional insurance pricing and terms. Standard policies are built for volume and predictability. They exclude entire categories of peril, cap limits at predetermined levels, and refuse coverage for locations deemed too risky or properties deemed too unusual. When a property doesn’t match those parameters, the insurer’s answer is no.

The Real Cost of Coverage Gaps

This is where hard-to-place risks become a genuine business problem. Property owners face a choice between accepting inadequate coverage, paying astronomical premiums to specialized carriers, or operating uninsured. The gap isn’t theoretical. A remote facility damaged by a peril excluded from primary coverage leaves owners responsible for the full loss. DIC policies eliminate this false choice by providing secondary protection precisely where primary coverage stops. The structure works because DIC focuses on specific excluded perils and locations rather than attempting to cover everything. This targeted approach lets underwriters price risk accurately and provide genuine protection for exposures that standard forms won’t touch.

Identifying Your Specific Coverage Shortfalls

The properties that benefit most from DIC are those with specific, identifiable coverage gaps rather than those requiring wholesale replacement of their entire insurance program. A high-value data center might have solid primary coverage for fire and theft but face a gap in contingent business interruption coverage if a non-owned supplier facility goes down. A historic property in a coastal zone might be insurable for standard perils but face an earthquake exclusion that creates unacceptable exposure. A specialty manufacturer with aging equipment might find primary carriers will only cover newer machinery, leaving older production lines uninsured. In each case, DIC fills the exact hole without duplicating primary coverage.

Location and Construction Drive Underwriting Decisions

Properties in flood zones, earthquake zones, or areas with high wildfire risk benefit particularly from DIC because standard carriers either exclude these perils entirely or impose limits so low they provide minimal protection. Remote locations, non-owned properties, and facilities with unique construction materials all present underwriting challenges that DIC solves effectively. A comprehensive gap analysis identifies exactly which perils and locations need additional protection, then structures DIC coverage to fill those specific holes rather than purchasing blanket excess coverage that wastes premium dollars. Underwriting factors including location risk, construction type, occupancy, asset value, and exposure growth all influence DIC pricing and limits. This means a historic property in a flood zone pays differently than a modern warehouse in a low-risk area.

Moving Forward with Targeted Solutions

The result is coverage that matches the actual risk profile rather than forcing property owners into inadequate standard policies or prohibitively expensive specialty programs. The transition from identifying coverage gaps to securing DIC protection requires a strategic assessment of your current policies and exposure profile. Your next step involves working with an experienced insurance partner who understands both your underlying coverage and the specific perils that standard forms exclude. This foundation sets you up to explore how DIC can address your hard-to-place risks and what the actual implementation process looks like.

How to Secure DIC Coverage for Your Property

Assess Your Current Coverage and Identify Gaps

Start with your existing policies in hand. Pull out your current property insurance declarations page, your commercial general liability policy, and any specialty coverage you carry. The goal is straightforward: identify what each policy covers, what it excludes, and where the gaps actually exist. Most property owners assume their standard policies protect them completely, then discover exclusions only after a loss occurs. That’s too late.

A gap analysis conducted now prevents that shock later. Look specifically for perils your primary carrier explicitly excludes-flood, earthquake, wildfire, equipment breakdown-and note the locations those policies cover. Does your primary coverage apply to non-owned supplier facilities? Does it protect contingent business interruption if a vendor goes down? Does it cover your remote satellite office?

Write down the actual limits too, not just the coverage types. A policy that caps business interruption at 30 days of lost income might leave you severely underinsured if recovery takes longer. Underwriting factors including location risk, construction type, occupancy, asset value, and exposure growth all influence DIC pricing and limits, which means your assessment needs to be detailed.

Don’t estimate. Measure square footage, document equipment age, note construction materials, and verify occupancy classification with your current carrier. This information becomes your foundation for determining exactly what DIC needs to cover.

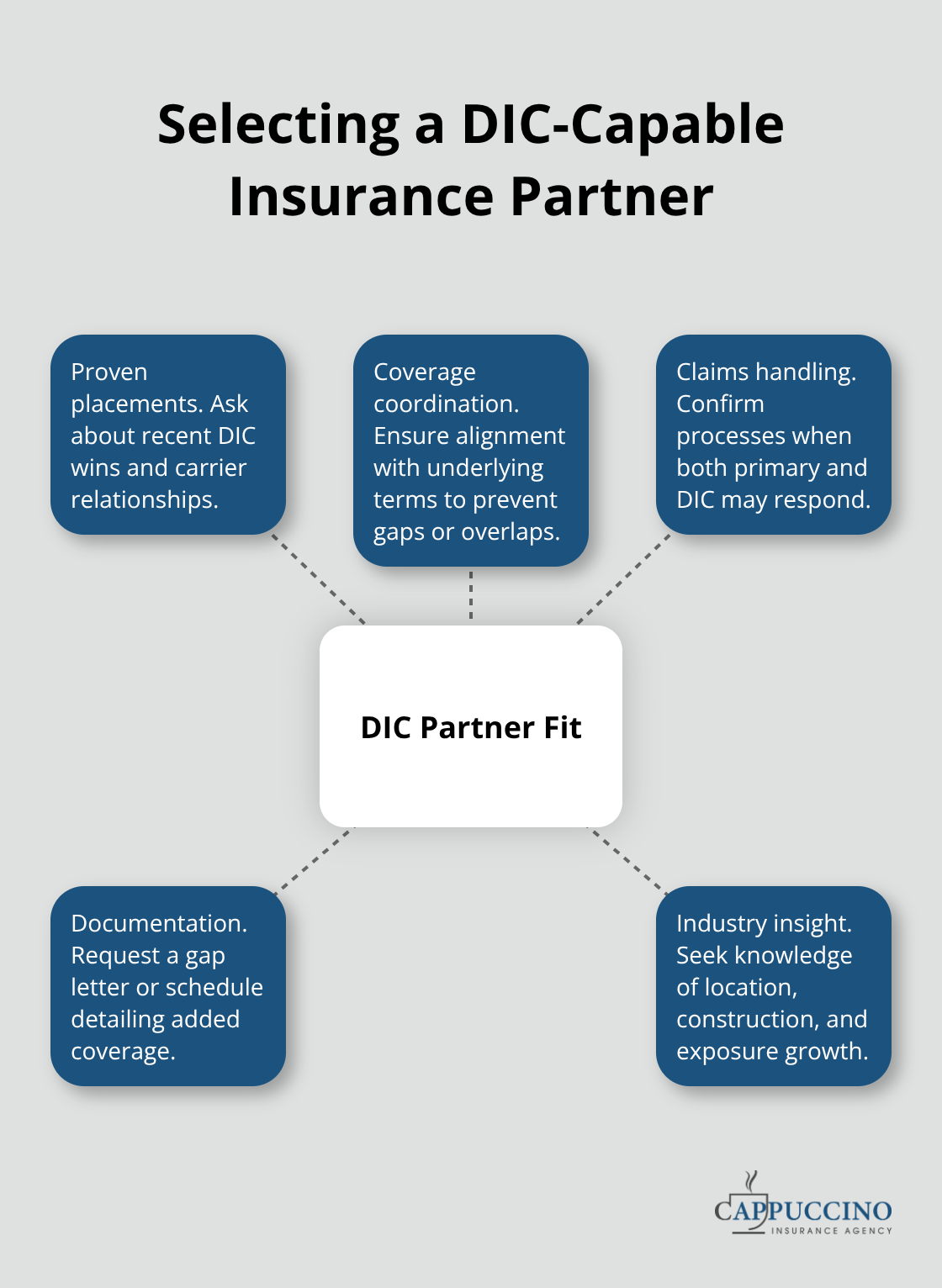

Find an Insurance Partner with DIC Expertise

Finding the right insurance partner matters more than finding the cheapest quote. DIC policies require coordination between your primary carriers and the DIC underwriter to avoid gaps and overlaps, which means your broker needs direct relationships with multiple carriers and deep experience structuring these programs.

Ask potential partners how many DIC placements they’ve completed in the past twelve months, what carriers they work with, and how they handle claims coordination when both primary and DIC policies might respond. A partner who simply quotes DIC without thoroughly reviewing your underlying coverage will create problems later.

When you’re evaluating partners, request a gap letter or schedule from the insurer outlining what the DIC adds beyond the underlying policy. This document becomes your proof that coverage is actually in place.

Understand Common Exclusions and DIC Solutions

Common exclusions that DIC addresses include flood damage, earthquake damage, wildfire damage in high-risk zones, equipment breakdown on aging machinery, and contingent business interruption at non-owned locations. But DIC policy language may include sublimits, deductibles, and coinsurance that require careful alignment with your underlying policy terms.

A hard to place property in a flood zone won’t have the same DIC structure as a modern warehouse in a low-risk area. Verify that any DIC endorsement specifies the exact perils covered, the locations protected, the deductible amounts, and how claims are triggered.

Structure Your DIC Program for Maximum Protection

Implementation requires mapping all assets and restoration priorities to determine appropriate DIC limits and sublimits. Specify triggers such as property damage or business interruption to ensure timely and full recovery.

Coordinate DIC with umbrella or wrap programs to avoid duplicative coverage and ensure consistent caps across all policies. Brokers play a central role in designing DIC programs and coordinate with primary carriers to avoid gaps or overlaps, so work closely with your partner throughout this process.

Final Thoughts

Difference in Conditions policies solve a real problem that standard insurance won’t address. Hard-to-place properties face genuine coverage gaps, and DIC fills those gaps with precision. Identifying your coverage gaps before a loss occurs saves you from catastrophic financial exposure when a property sustains damage from an excluded peril or when a loss at a non-owned location falls outside your primary policy’s protection.

The structure of DIC works efficiently because it doesn’t duplicate primary coverage or force you to purchase unnecessary blanket excess protection. Your next move is to pull your current policies and conduct a gap analysis-document what’s excluded, note which locations your primary coverage doesn’t protect, and measure your actual exposure against your policy limits. This foundation tells you exactly what DIC needs to cover and positions you to find an insurance partner with real DIC experience who can coordinate with your primary carriers.

We at Cappuccino Insurance Agency specialize in this work and deliver specialty solutions for hard-to-place properties across California, including Difference in Conditions wraps tailored to your specific exposures. Visit our website to discuss your coverage needs and discover how DIC can protect your property.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.