Home Auto Life Bundle: Convenience and Coverage In One Package

Managing multiple insurance policies feels like juggling. You’re tracking separate renewal dates, different customer service numbers, and scattered paperwork across your desk.

A home auto life bundle simplifies everything. At Cappuccino Insurance Agency, we’ve seen firsthand how bundling your home, auto, and life insurance into one package cuts through the complexity while putting real money back in your pocket.

What Bundling Actually Means

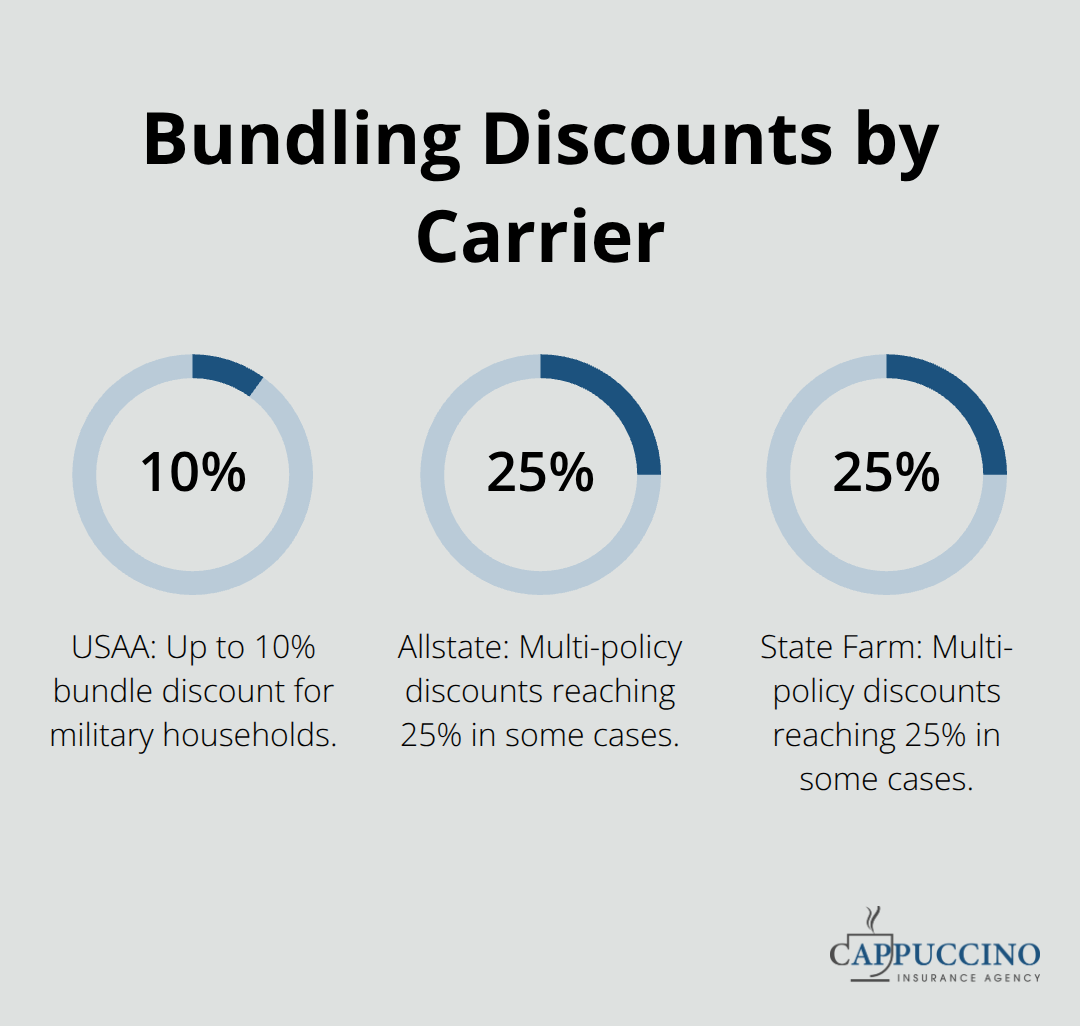

A home auto life bundle combines your homeowners, auto, and life insurance policies under one carrier, giving you a single renewal date, one bill, and coordinated coverage across your assets. This isn’t just marketing language-it’s a structural change that affects how you pay, manage claims, and receive support. When you bundle with carriers like Progressive, new customers save an average of $1,086 annually, according to their 2024–2025 customer data. USAA reports bundle discounts up to 10% for military households, while Allstate and State Farm offer multi-policy discounts reaching 25% in some cases. The savings come directly from the carrier’s reduced administrative costs when handling multiple policies for one household rather than shopping your business across competitors.

How the Structure Works

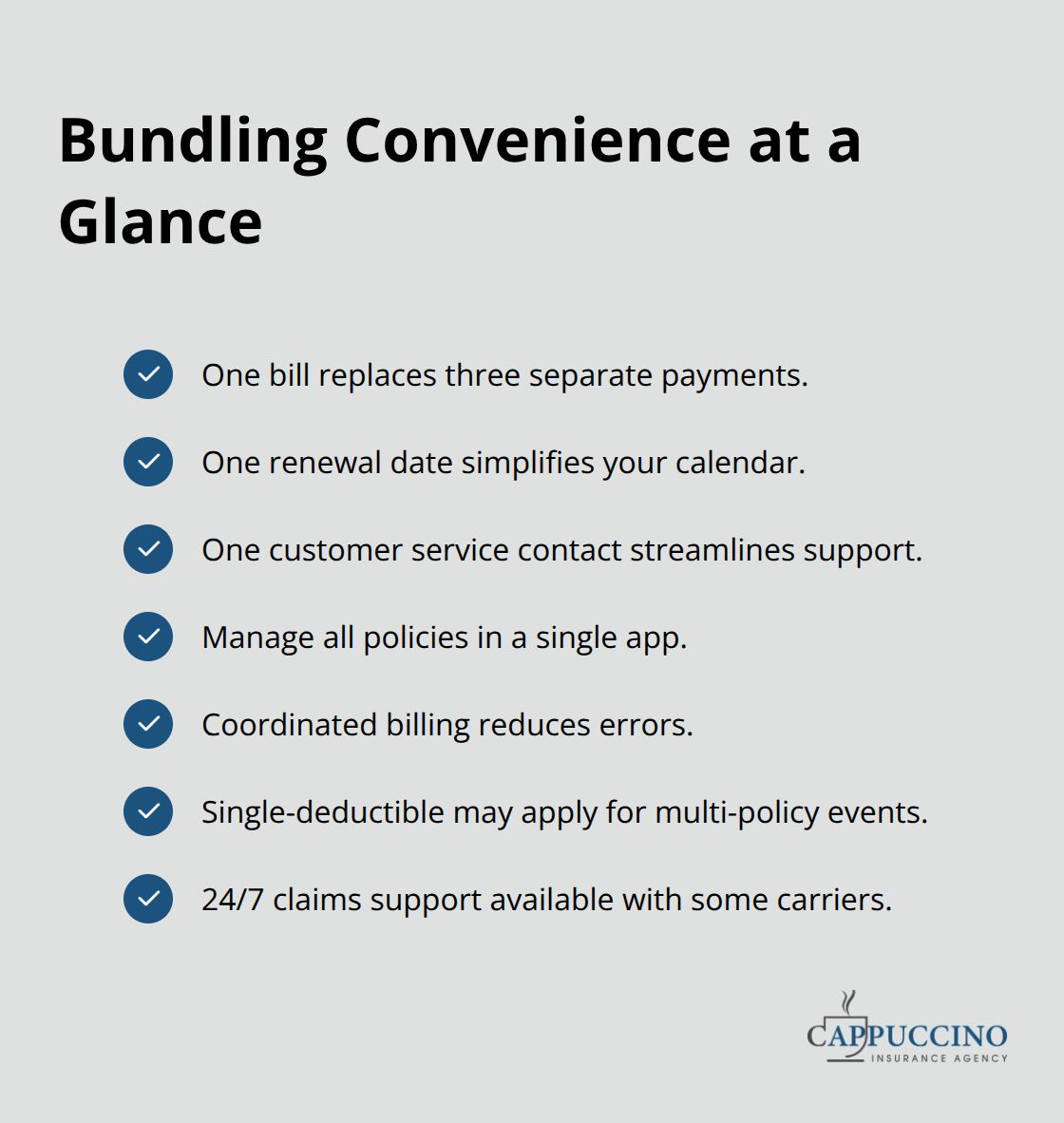

Bundling doesn’t mean your policies merge into one legal document. Instead, each policy-home, auto, and life-maintains its own coverage terms, limits, and deductibles. What changes is the backend: one login, one renewal cycle, one customer service contact, and coordinated billing. If both your home and auto policies are underwritten by the same carrier, some insurers offer a single-deductible feature, meaning you pay only one deductible if a covered incident damages both your home and vehicle. This matters in real situations like a house fire that damages a parked car or a storm that hits your garage and vehicles simultaneously. The practical advantage extends to your mobile experience-Progressive and GEICO both offer apps where you manage all bundled policies in one place, file claims across multiple coverages, and access digital ID cards for both auto and home policies without switching between applications.

Why Carriers Push Bundling

Insurance companies aggressively promote bundling because it reduces their costs and increases customer retention. A customer with one policy cancels more easily than a customer with three. Bundling also gives carriers more complete information about your household risk profile-they see your driving record, home location, claims history, and life insurance needs together, allowing them to price more accurately and cross-sell additional coverage. From your perspective, this matters because bundled customers typically experience better claims handling when events affect multiple policies. You’re not dealing with separate claim adjusters; one team coordinates the response.

When Bundling Doesn’t Win on Price

Bundling isn’t always the cheapest option. According to U.S. News data comparing real quotes across carriers, bundled rates vary significantly-USAA averages $149 monthly for a home and auto bundle, while Progressive comes in around $215 for the same coverage. Shopping separate quotes from different carriers sometimes beats a single-carrier bundle. The takeaway: bundling delivers real convenience and meaningful savings for most households, but you need to compare your options carefully. An independent agent can help you evaluate whether one carrier’s bundle or a mix of carriers saves you more money while still giving you the convenience you want.

What You Actually Save by Bundling

New customers bundling auto and home with Progressive save an average of $1,086 annually, according to their 2024–2025 customer survey. State Farm reports similar figures, with bundled customers saving around $1,356 on average. These aren’t theoretical numbers-they come from actual policyholders who switched to bundled coverage. The savings range depends on your state and current rates, but average annual savings from bundling typically fall between 5% and 30% across major carriers. USAA tops out at 10% for military households, while Allstate and Progressive can reach 25% in certain scenarios.

Each additional policy qualifies for its own multi-policy discount, so adding life insurance to an auto-home bundle generates additional savings beyond what you already receive. Raising your deductibles within a comfortable range amplifies these savings further-moving from a $500 to $1,000 deductible on your auto policy, for example, can reduce your premium by 15% to 30%, and this works the same way whether you’re bundled or not.

One Bill, One Renewal, One Login

Bundled policies eliminate the administrative friction that drains time and creates billing confusion. Instead of tracking three separate renewal dates throughout the year, you receive one. Instead of three different customer service numbers, you contact one carrier. Progressive and GEICO both let you manage everything through a single app-viewing policy details, making changes, accessing digital ID cards, and filing claims without switching between applications.

Life changes force policy adjustments, and bundling handles them faster. Moving to a new home, purchasing a second vehicle, or increasing coverage limits takes minutes rather than hours of phone calls and paperwork shuffling. The renewal process becomes predictable: one email, one payment, one deadline. State Farm agents review all three policies at once during bundled renewals, identifying coverage gaps and updated discounts in a single conversation rather than three separate appointments. For households with teen drivers or multiple vehicles, this consolidated approach prevents the common mistake of overlooking coverage updates on one policy while focusing on another.

Claims Coordination Saves Time and Money

When a covered incident damages both your home and vehicle-a house fire that destroys a parked car, a storm that damages your roof and vehicles, or a fallen tree that hits both structures-bundled policies create a single coordination point instead of juggling separate claim adjusters. Carriers like Progressive offer a single-deductible feature when both home and auto policies are underwritten by the same company, meaning you pay one deductible instead of two after a multi-policy event. This feature alone can save hundreds of dollars in a worst-case scenario.

One claims team handles both the home and auto aspects of the incident rather than waiting for two separate adjusters to communicate. GEICO provides 24/7 claim support and dedicated specialists for bundled policies, eliminating the frustration of explaining your situation twice to different departments. Filing a claim on one bundled policy typically doesn’t affect your rates on the other policy either, since home and auto are rated independently-a fact that many customers misunderstand.

Finding Your Best Bundle Option

The carrier you choose shapes both your savings and your experience. Shopping separate quotes from different carriers sometimes beats a single-carrier bundle, so comparing your options carefully matters. An independent agent can help you evaluate whether one carrier’s bundle or a mix of carriers saves you more money while still giving you the convenience you want. The next step involves assessing what coverage you actually need across all three policy types.

Picking the Right Bundle for Your Situation

Know Your Coverage Needs First

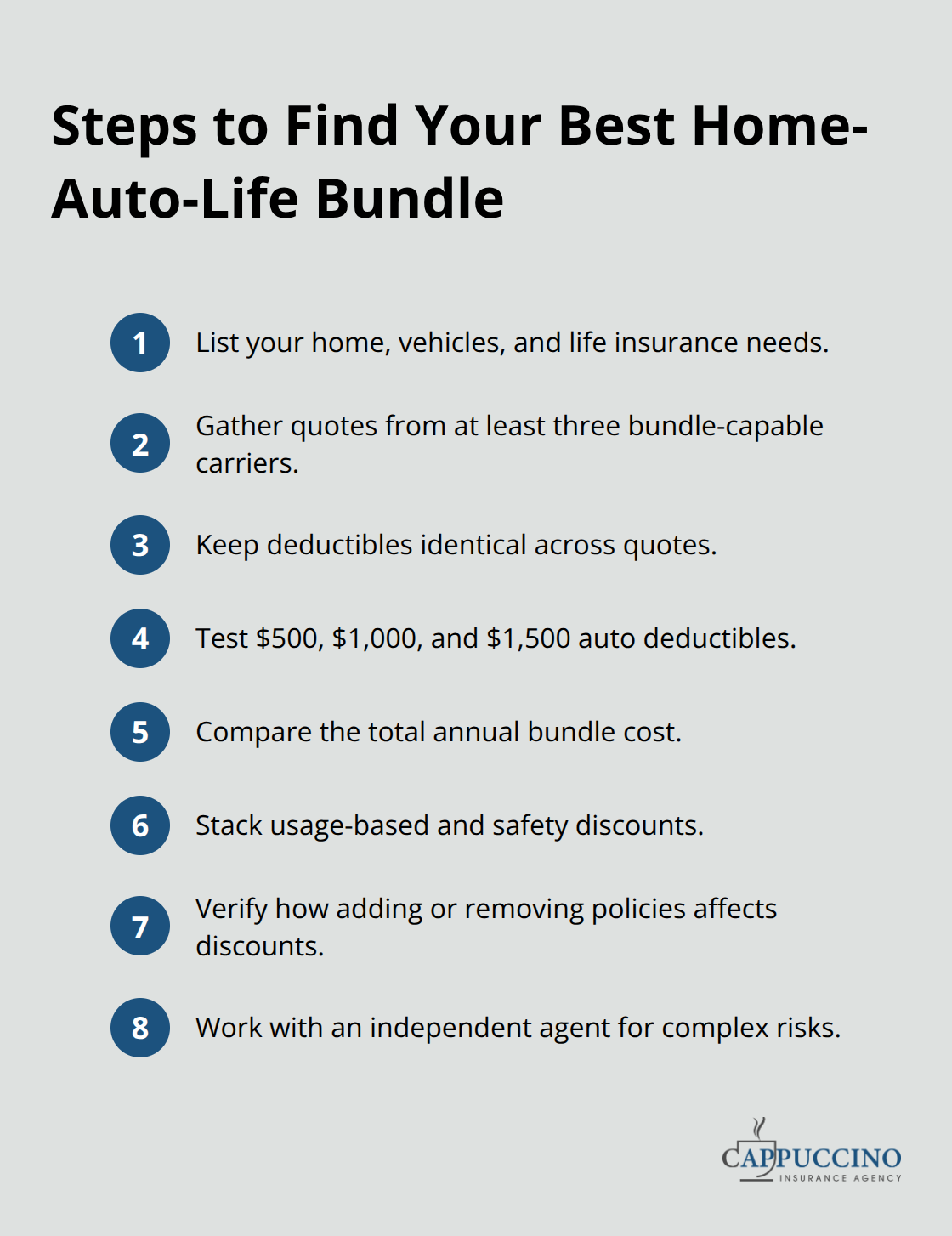

Start by listing what you actually own and what could go wrong. Your home’s replacement cost, your vehicles’ values, your dependents’ financial needs if something happened to you-these numbers drive your coverage decisions, not the bundle itself. A $300,000 home needs different homeowners limits than a $600,000 home. A 16-year-old driver needs different auto coverage than a 45-year-old with a clean record. Life insurance needs depend on whether you have a mortgage, dependents, or significant debt.

Most people underestimate life insurance needs; financial advisors recommend coverage based on your lifetime income, though many bundled policies start with modest amounts. Before comparing carriers, know your numbers. Use your mortgage statement for your home’s loan amount, check your vehicle titles for actual values, and calculate what your family would need if you weren’t there to provide income. This takes 30 minutes and prevents you from bundling the wrong coverage amounts.

Get Quotes from Multiple Carriers

Once you know what you need, request quotes from at least three carriers offering bundles in your state. Progressive, State Farm, and USAA (if military-eligible) provide online quotes within minutes. Auto-Owners and Nationwide require agent contact but often deliver competitive rates for specific situations like older homes or teen drivers.

Don’t assume the carrier with the lowest auto rate offers the best home bundle-State Farm frequently underprices auto but charges more for homeowners, while Progressive tends to price both competitively together. Real quotes from U.S. News data show monthly bundle costs ranging from $149 with USAA to $215 with Progressive for identical coverage, a $66 monthly difference that compounds to nearly $800 annually. Request quotes with identical deductibles across all carriers so you’re comparing apples to apples.

Adjust Deductibles to Find Your Best Price

Most carriers let you adjust deductibles during the quote process; try $500, $1,000, and $1,500 auto deductibles to see how premiums shift. Raising your home deductible from $500 to $1,000 typically reduces premiums by 10% to 15%, while auto deductible increases save 15% to 30% depending on your driving record and location.

If you’re bundling life insurance, ask whether it’s term or permanent coverage-term costs significantly less and works better for most households, while permanent coverage makes sense only if you need lifetime protection or have estate planning concerns. Compare the total annual cost of all three policies bundled together, not individual policy prices. A carrier might offer cheap auto but expensive home; you need the bundle total.

Stack Additional Discounts with Your Bundle

After narrowing to your two best options, ask each carrier about additional discounts beyond bundling. Progressive rewards customers with low mileage (under 15,000 miles annually) through Snapshot, potentially saving another 10% to 30%. State Farm offers discounts for completing a defensive driving course, installing security systems, or maintaining good credit. Allstate’s Drivewise program monitors safe driving habits and adjusts rates accordingly.

These stacked discounts compound with bundle savings, sometimes reaching 40% or more off standard rates. Life insurance bundled with auto and home occasionally qualifies for additional multi-policy discounts-ask explicitly whether your quoted life premium includes all applicable reductions. Finally, confirm what happens if you add or remove a policy later. Most carriers apply bundle discounts immediately when you add coverage, but some require a renewal to activate discounts. If you cancel one policy, you typically lose multi-policy discounts on remaining policies, so bundling a policy you might drop soon doesn’t make financial sense.

Work with an Independent Agent for Complex Situations

An independent agent can identify the best company for your situation and compare bundles from multiple providers while matching your actual coverage needs, rather than locking you into one carrier’s bundle because it’s convenient. This approach proves especially valuable if you live in California and face wildfire risk or other hard-to-place coverage challenges that require specialty solutions.

Final Thoughts

A home auto life bundle delivers three concrete benefits that matter in real life: lower premiums through multi-policy discounts, simplified management with one renewal date and one login, and faster claims handling when incidents affect multiple policies. New customers bundling with Progressive save an average of $1,086 annually, while State Farm reports similar savings around $1,356. These aren’t promises-they’re actual numbers from households that made the switch.

The convenience factor extends beyond cost. One bill replaces three, one customer service contact replaces three phone numbers, and one app manages all your policies instead of juggling separate logins. When life changes happen (you buy a home, add a vehicle, or need to adjust coverage), bundled policies update faster because one agent reviews everything together rather than handling separate transactions.

We at Cappuccino Insurance Agency specialize in helping California households find the right home auto life bundle for their situation. As an independent agency partnering with 20+ carriers, we compare options from multiple providers rather than pushing one company’s bundle. Contact us for a free coverage assessment and let’s find your best bundle option together.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.