High-Risk Property California: Understanding Your California FAIR Plan Options

Finding affordable insurance for a high-risk property in California feels impossible. The standard market often rejects these properties, leaving owners with limited options.

We at Cappuccino Insurance Agency help property owners navigate the California FAIR Plan and discover coverage solutions that actually work. This guide walks you through your real options.

Understanding the California FAIR Plan

What the California FAIR Plan Actually Covers

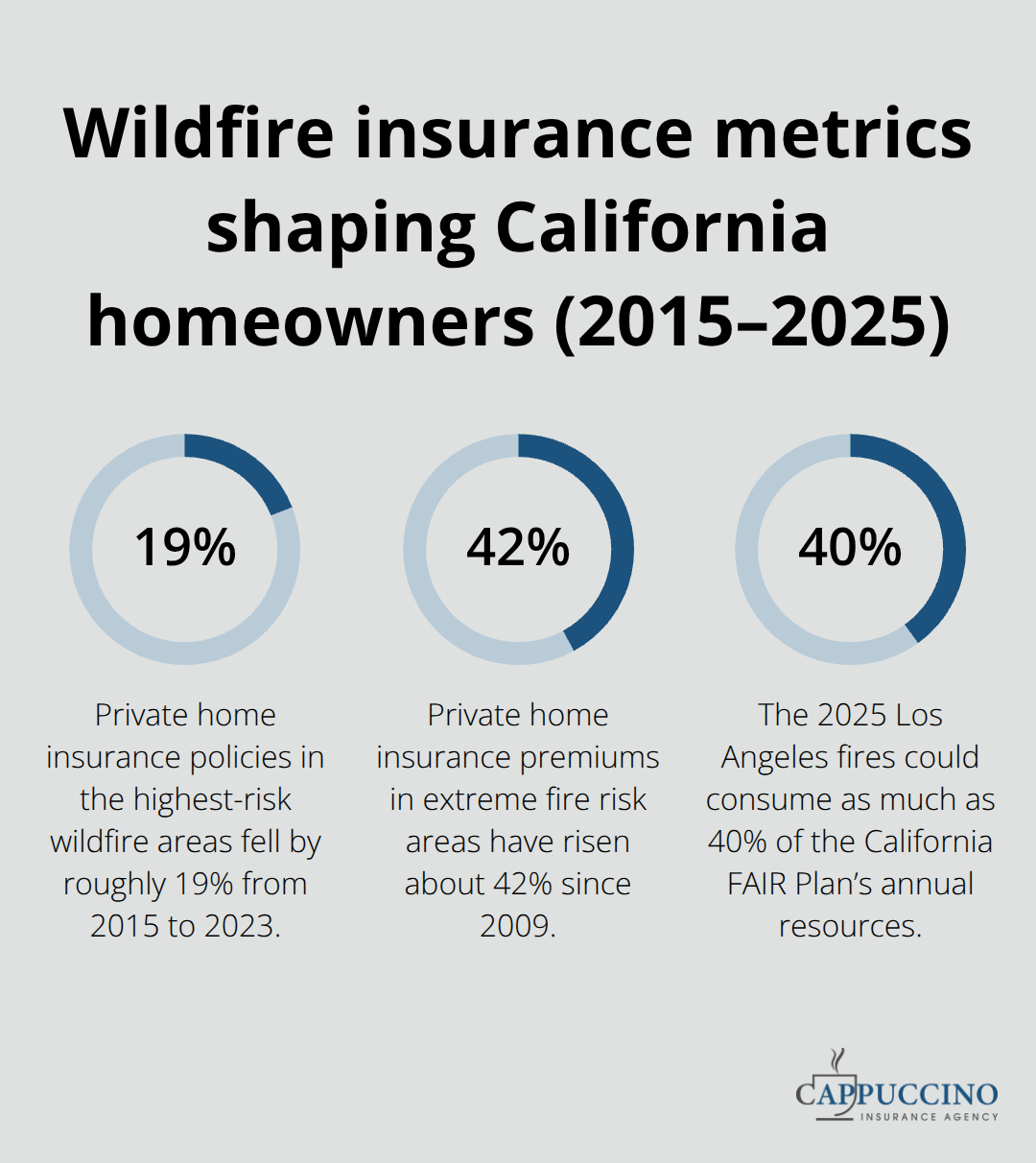

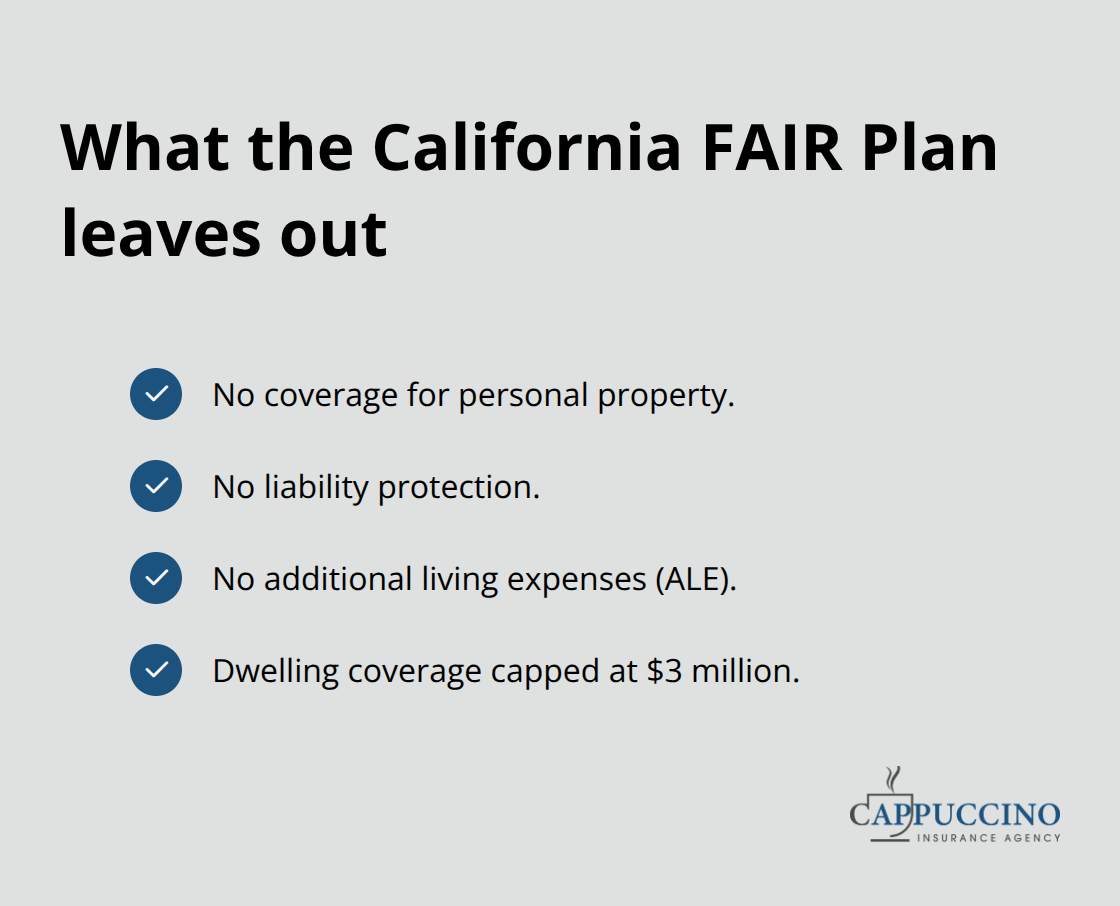

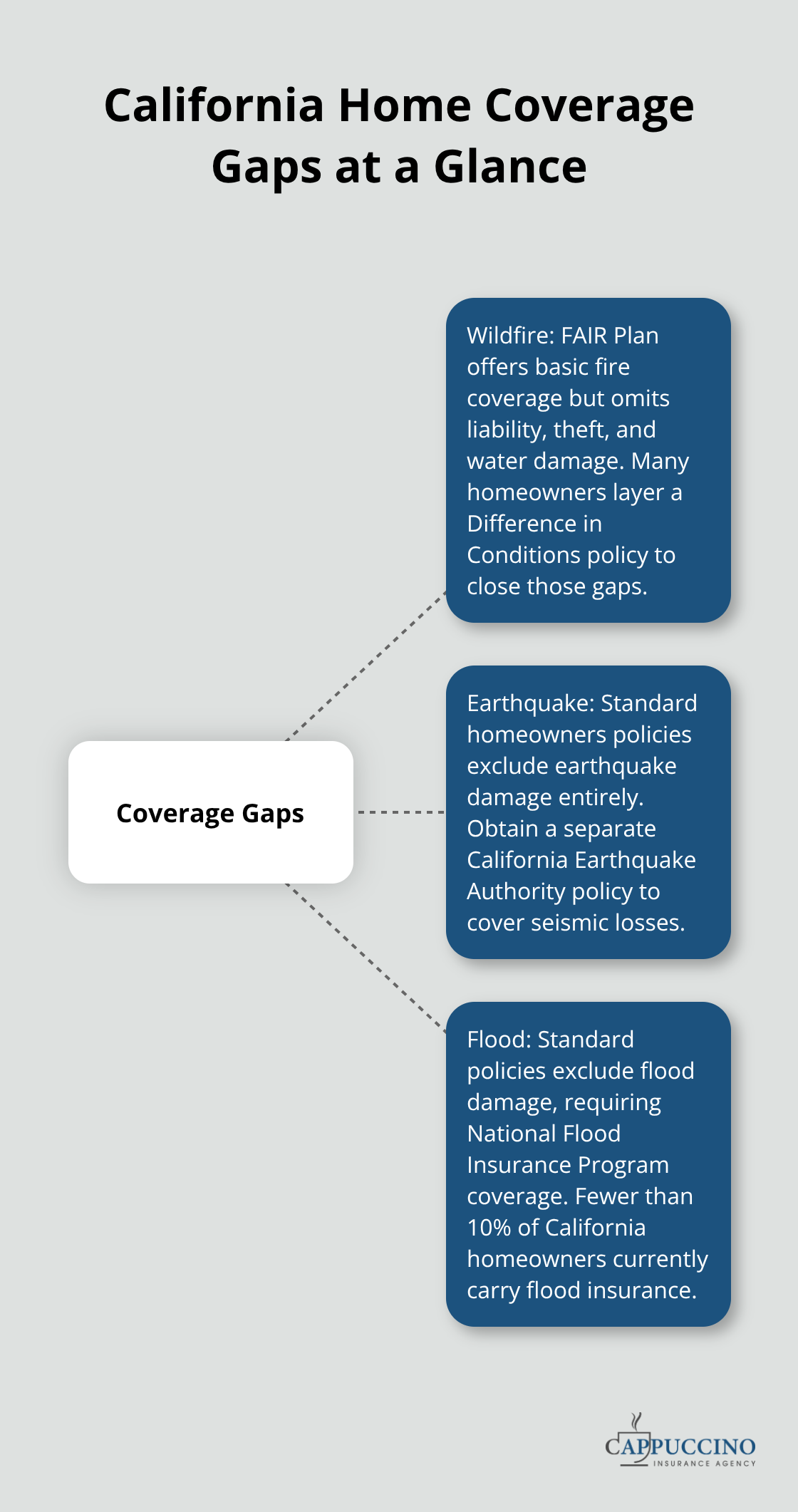

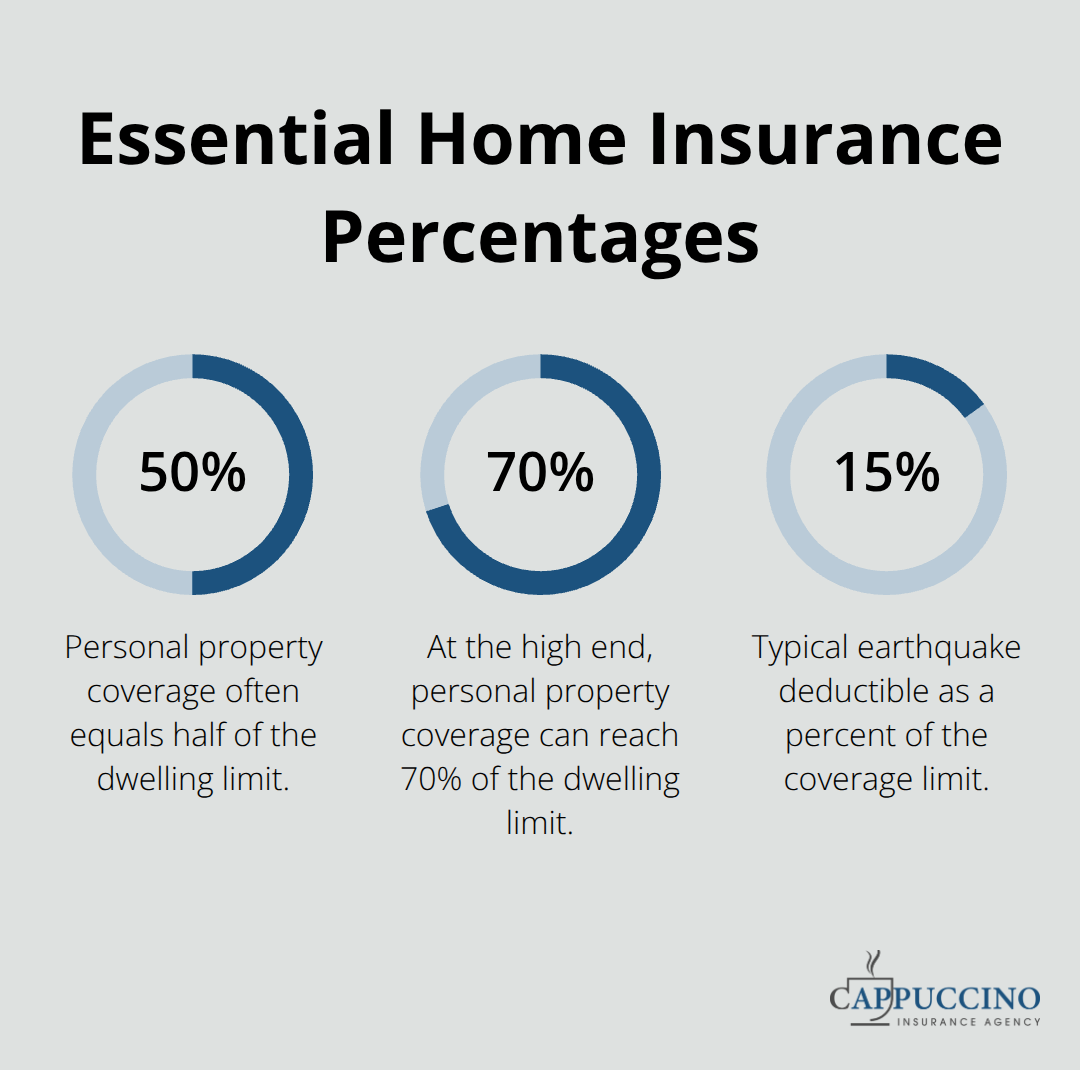

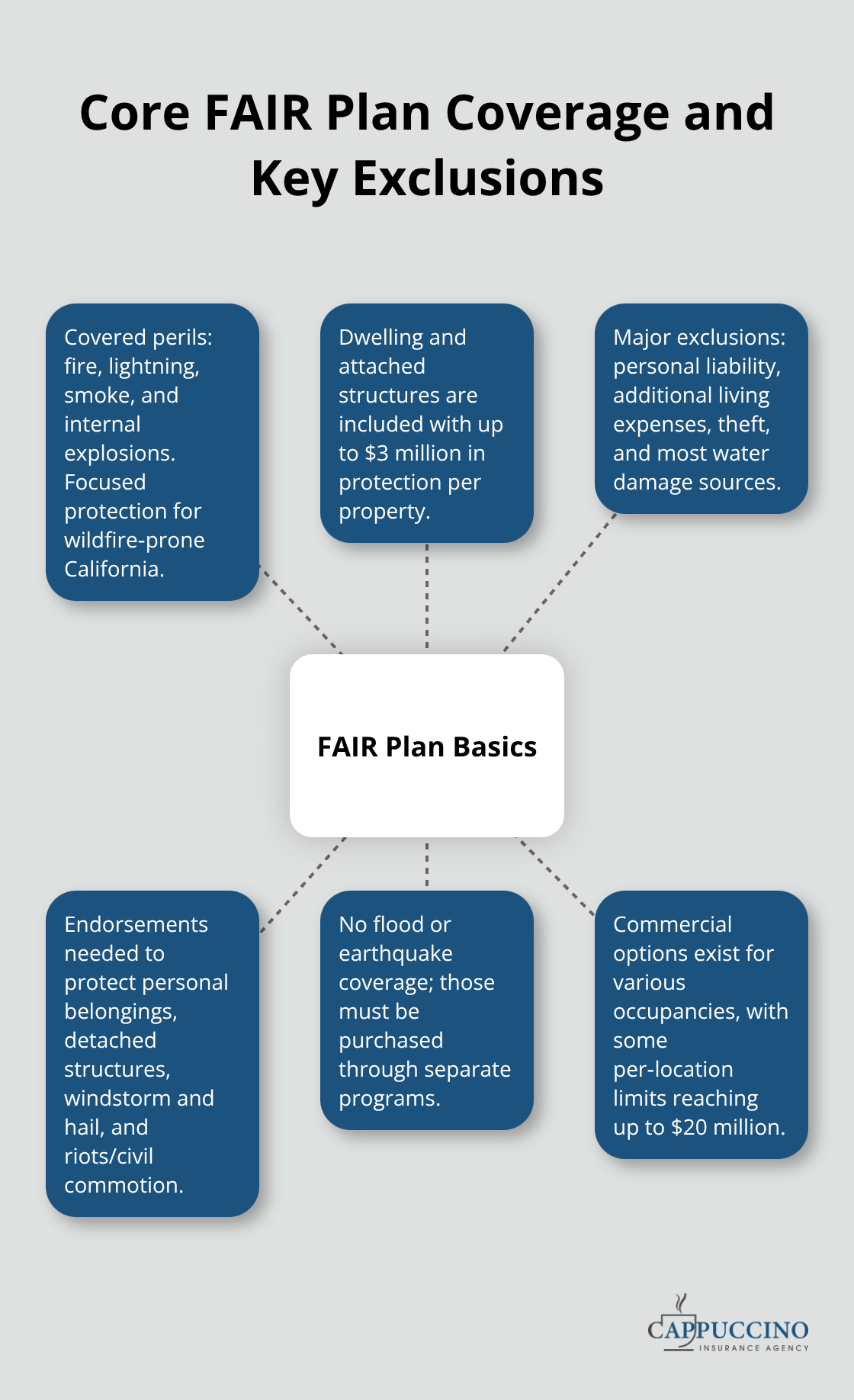

The California FAIR Plan provides basic fire insurance for properties that traditional insurers won’t touch. As of March 2026, the plan covers 684,388 policies with $750 billion in total exposure, according to the California FAIR Plan’s official data. The core coverage includes your dwelling, attached structures, and up to $3 million in protection per property. You receive coverage for fire, lightning, smoke, and internal explosions-the perils that matter most in wildfire-prone California. However, basic FAIR Plan coverage excludes personal liability, additional living expenses if you’re displaced, theft, and water damage. Your personal belongings and detached structures like garages require specific endorsements to protect those assets. The plan also excludes flood and earthquake coverage entirely, which represents a significant gap for California properties.

Windstorm and hail protection or coverage for riots and civil commotion require endorsements to expand what’s included. Commercial properties can access coverage for habitational units, retail spaces, mercantile operations, manufacturing risks, farms, and office buildings, with per-location limits reaching up to $20 million for some business structures.

Eligibility Requirements and the Application Process

To qualify for FAIR Plan coverage, you must own or rent property in California and prove that traditional market insurers rejected you. The California Department of Insurance requires that you demonstrate a diligent search for private coverage before the FAIR Plan accepts your application. You cannot qualify if private insurance is reasonably available to you, and vacant properties that sit empty more than 50 percent of the year won’t qualify. Your property must also meet California building codes and not have extensive unrepaired damage. The application process starts with a licensed broker-the California FAIR Plan maintains a broker finder tool on their website. Your broker performs the market search on your behalf at no additional cost to you, then calculates your home’s replacement cost value, which differs from market value and affects your coverage limits. A home inspection is standard; the FAIR Plan uses this to assess insurability and risk level. Once approved, you can add endorsements or pair your FAIR Plan policy with a Difference-in-Conditions policy to fill coverage gaps.

New business averaged 16,466 policies monthly in the first half of fiscal year 2026, down from the previous year but still substantially higher than 2022 levels, reflecting ongoing demand from property owners in high-risk areas.

Coverage Gaps That Matter

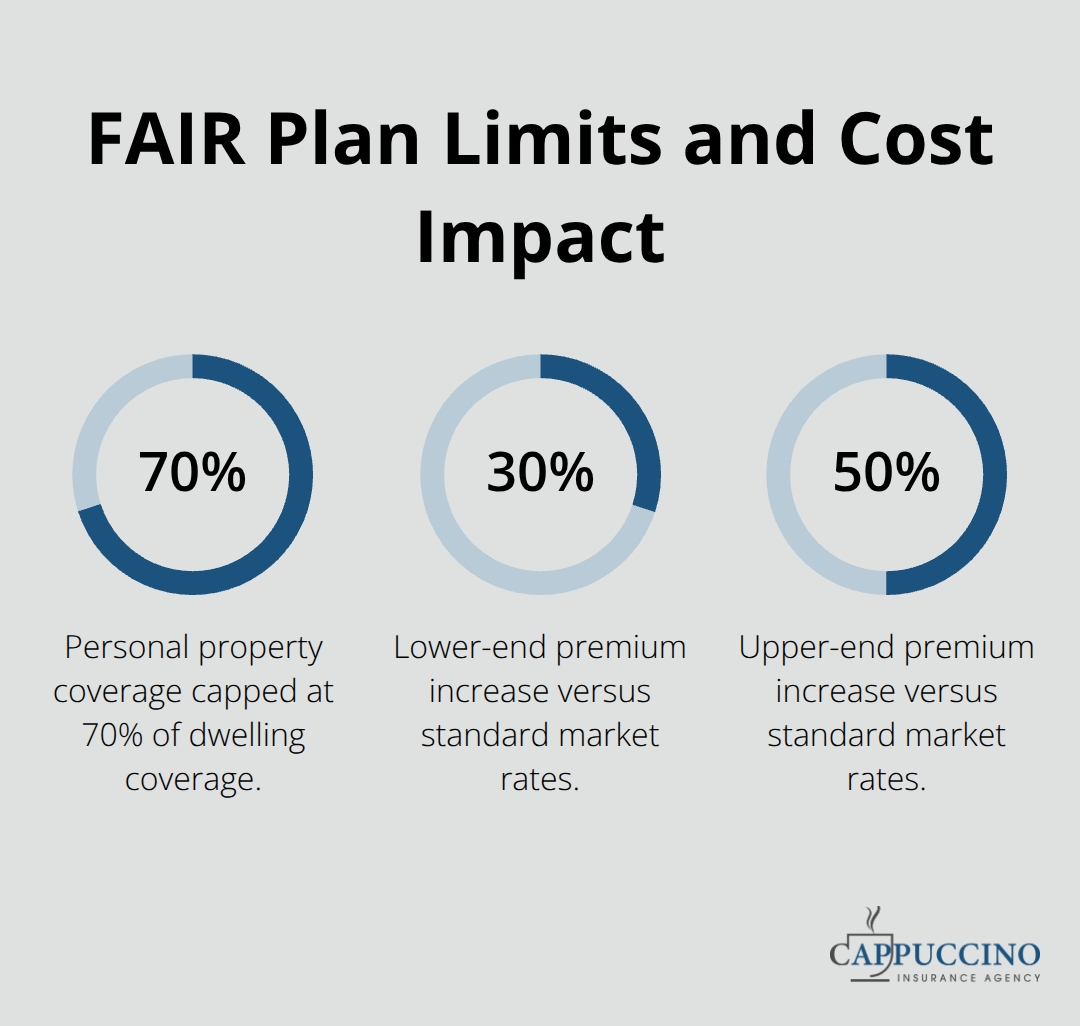

FAIR Plan premiums are considerably higher than private market rates, and costs are rising sharply. The California Department of Insurance projects an average premium increase of about 35.8 percent starting in early 2026, with roughly half of current customers facing increases between 40 and 55 percent. The $3 million dwelling coverage limit becomes a real problem for high-value homes that cost more to rebuild than that threshold, forcing owners to seek additional coverage strategies. The plan’s narrower scope means you lose critical protections that standard homeowners policies provide: no liability coverage if someone is injured on your property, no additional living expenses if fire displaces you, no theft protection, and no water damage coverage from sources other than the covered perils. Many property owners combine FAIR Plan policies with Difference-in-Conditions coverage to create comprehensive protection. This layered approach addresses the gaps that leave you vulnerable when the FAIR Plan’s basic coverage ends.

Closing FAIR Plan Gaps With Strategic Add-On Coverage

Why Basic FAIR Plan Coverage Falls Short

The FAIR Plan’s basic protection stops short of what most property owners actually need. A $3 million dwelling limit and zero liability coverage create real exposure that requires additional layers. Your property faces risks that the FAIR Plan simply doesn’t address: someone gets injured on your property and sues you, fire displaces you and you need temporary housing costs covered, theft occurs, or water damage happens from sources outside the FAIR Plan’s covered perils. These gaps leave you financially vulnerable when claims happen.

How Difference-in-Conditions Insurance Fills the Gaps

Difference-in-Conditions insurance wraps around your FAIR Plan policy to cover what’s missing. A DIC policy adds personal liability protection if someone gets injured on your property, covers additional living expenses if fire displaces you temporarily, protects against theft and water damage from sources outside the FAIR Plan’s perils, and extends protection to personal belongings and detached structures. The California Department of Insurance acknowledges that DIC policies remain the primary way to fill these gaps until a more comprehensive FAIR Plan residential option becomes available. Premiums for DIC coverage vary based on your property’s risk profile and the specific coverages you add, but pairing a DIC with FAIR Plan coverage typically costs significantly less than abandoning the FAIR Plan entirely if private market options won’t accept your property.

Getting a Complete Picture of Your Costs

When you work with a licensed broker, they can quote both your FAIR Plan policy and a DIC simultaneously to show you the combined cost and total protection you’d receive. This approach transforms the FAIR Plan from a bare-bones safety net into actual comprehensive coverage. You see exactly what you pay and what you get in return, rather than discovering gaps after a loss occurs.

FAIR Plan vs. Traditional Homeowners Insurance: The Real Differences

Traditional policies cover dwelling, personal property, liability, medical payments, and additional living expenses in one streamlined package with broader peril coverage. FAIR Plan policies require endorsements for windstorm and hail, riots and civil commotion, and aircraft damage, while earthquake and flood coverage must come from entirely separate policies through the California Earthquake Authority or the National Flood Insurance Program. Traditional insurers typically offer replacement cost coverage with higher limits, flexible deductibles, and lower premiums than the FAIR Plan’s rising rates.

When the FAIR Plan Becomes Your Best Option

If you can secure traditional coverage, that’s always preferable. However, for properties in high-risk wildfire zones or with challenging characteristics, the FAIR Plan combined with a DIC policy becomes the practical path forward. Your next step involves working with a licensed broker who can evaluate whether traditional market options exist before you default to the FAIR Plan, then structure DIC wraps that deliver protection equivalent to what standard homeowners policies provide. This assessment determines not just whether you qualify for the FAIR Plan, but whether better alternatives exist in the private market.

How to Cut FAIR Plan Costs and Stay Covered

Work with a licensed broker to access real options

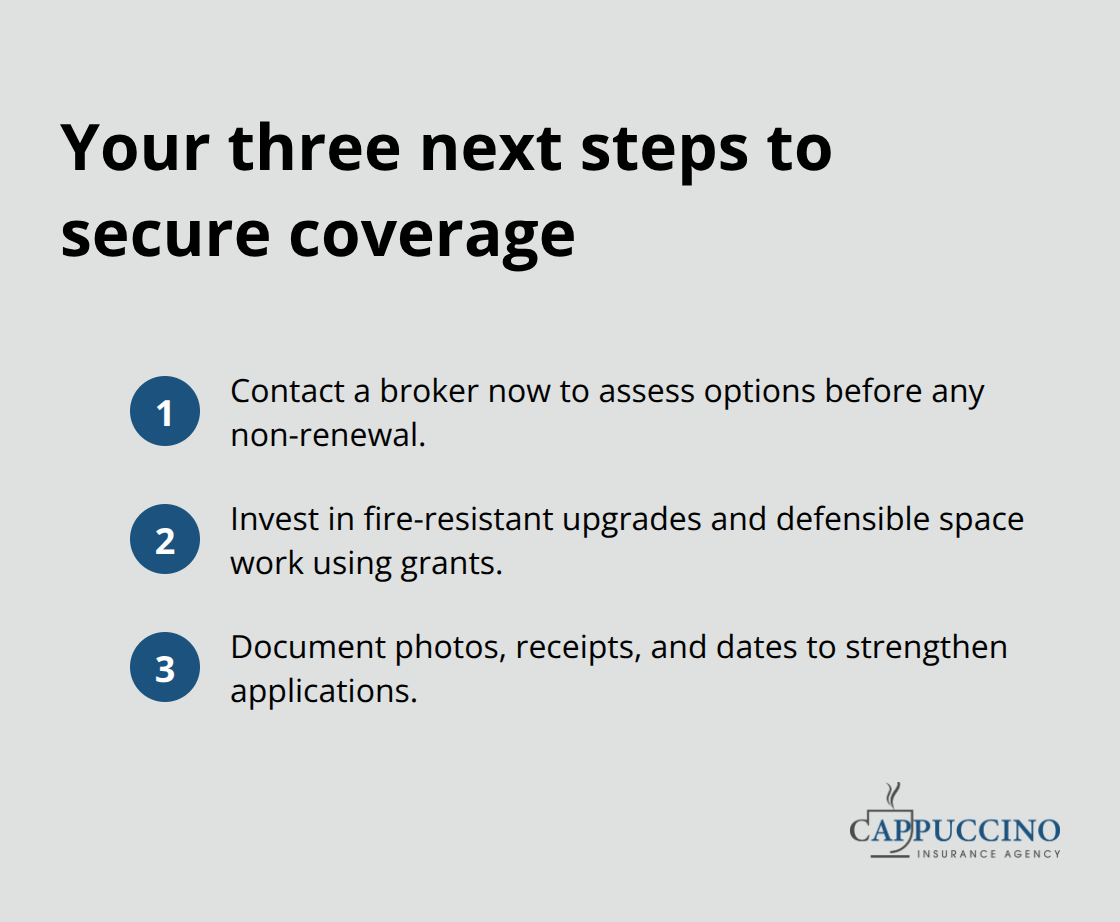

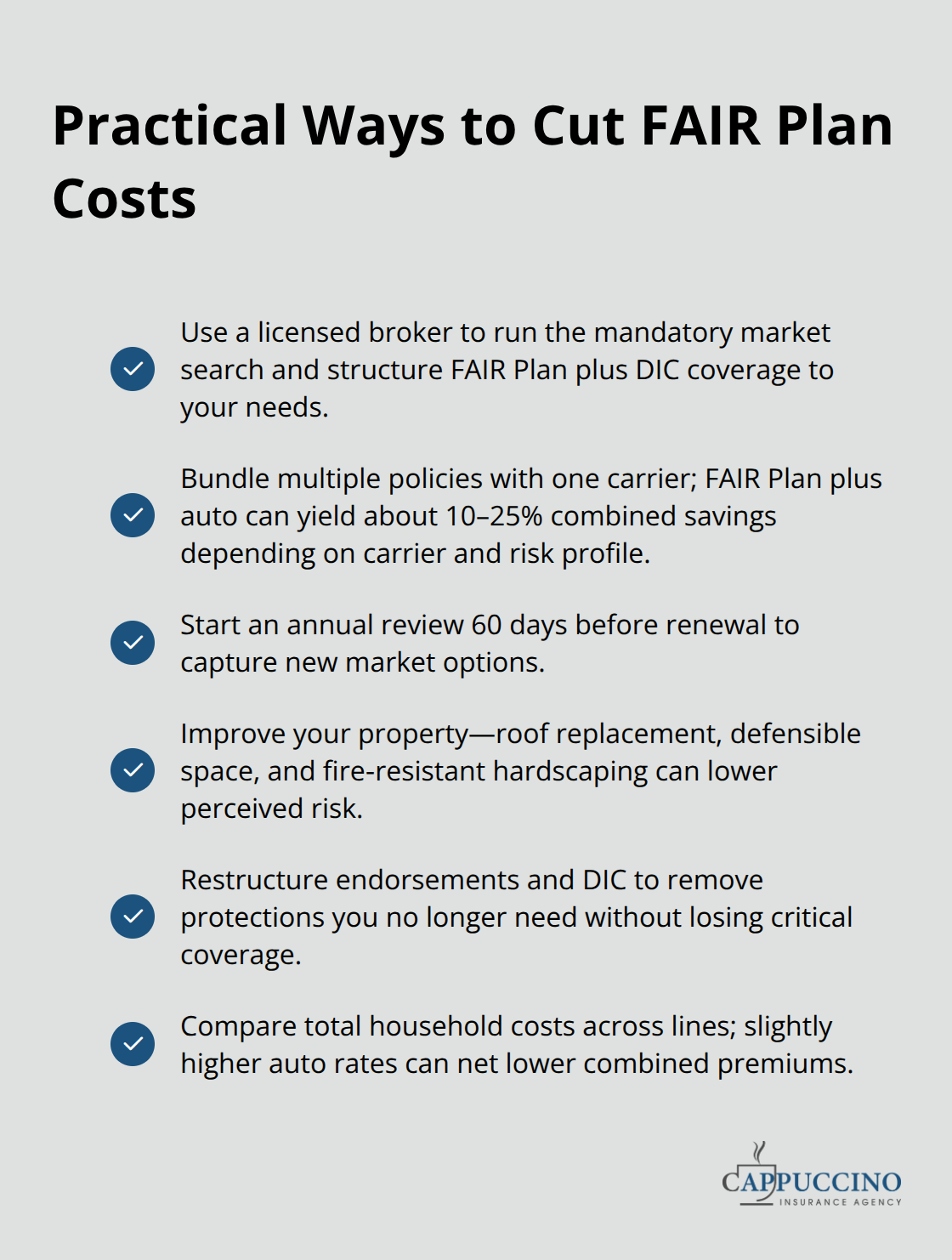

Licensed brokers are your only practical path to affordable coverage in high-risk California, and this decision matters more than most property owners realize. A broker performs the mandatory diligent search for private market options at zero cost to you, then structures FAIR Plan coverage with the right endorsements and Difference-in-Conditions wraps to match your actual needs. The broker advantage extends beyond paperwork: they access underwriting guidelines from multiple carriers simultaneously, identify which insurers might accept your property despite its risk profile, and negotiate endorsement pricing that reduces your total annual cost. Without a broker, you either apply directly to the FAIR Plan and accept whatever basic coverage arrives, or you waste weeks contacting private insurers individually who will likely reject you anyway. The California FAIR Plan’s own broker finder tool exists specifically because brokers are the efficient gatekeepers to coverage. When comparing broker fees, understand that the best ones charge nothing upfront because they earn commissions from carriers. Your only real cost is the premium itself.

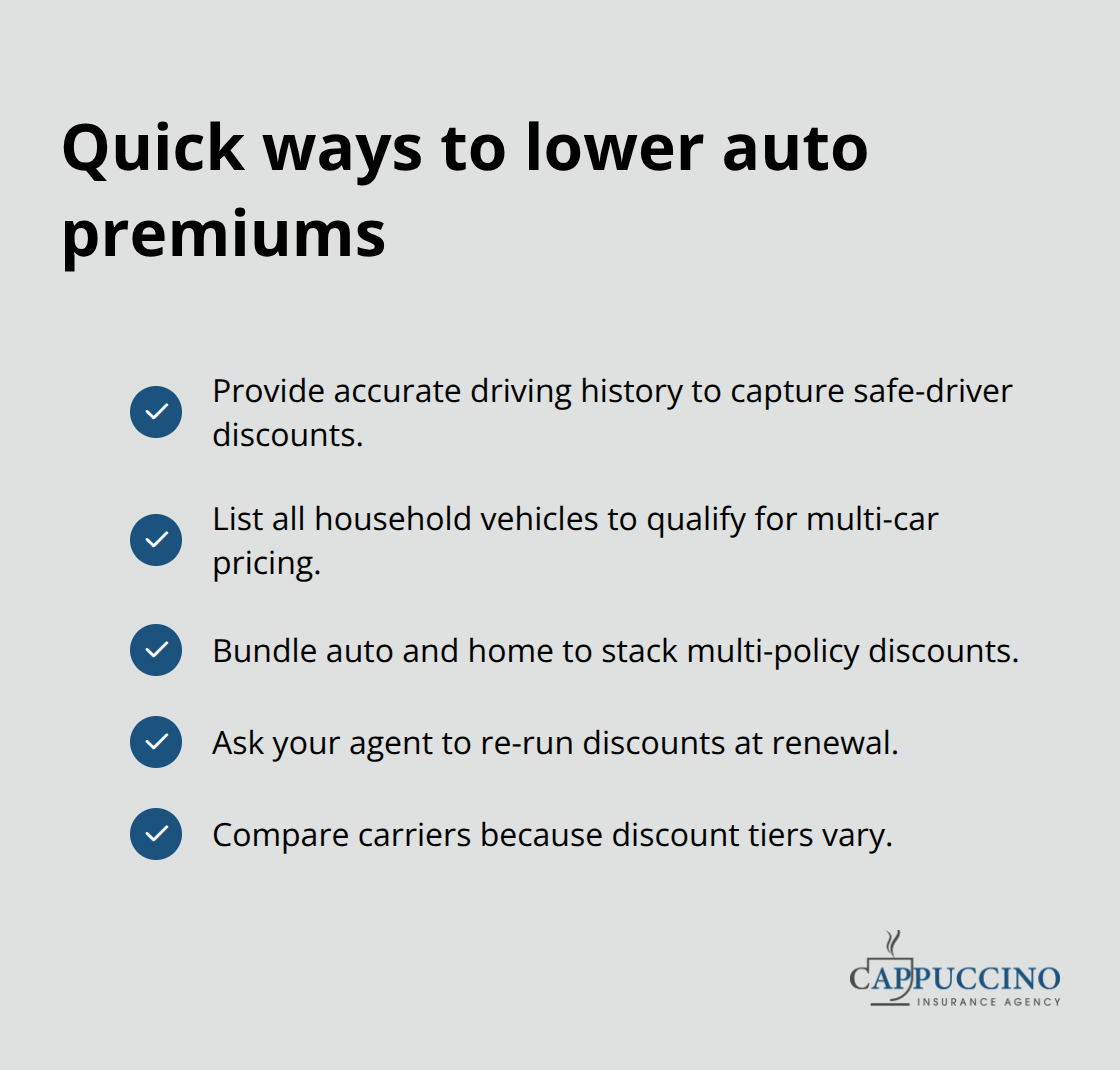

Stack multiple policies with one carrier for meaningful savings

Stacking multiple policies with the same insurer produces discounts that individual policies never receive. If a carrier will insure your dwelling through FAIR Plan coverage, ask whether they also write auto insurance, umbrella liability, or life insurance for your household. Stacking a FAIR Plan policy with auto coverage can reduce your combined premium by 10 to 25 percent depending on the carrier and your risk profile, according to common industry bundling structures. Your broker knows which carriers offer the most aggressive bundle discounts for high-risk properties and can structure your policies to maximize savings across all lines. The math works in your favor: paying slightly higher auto premiums to get bundled discounts on FAIR Plan coverage often results in lower total household insurance costs than purchasing FAIR Plan and auto separately.

Adjust your coverage annually before renewal arrives

FAIR Plan premiums rose an average of 35.8 percent across the board starting in early 2026. This environment demands annual review rather than passive renewal. Sixty days before your FAIR Plan policy renews, contact your broker to request a fresh market search and updated quotes from any carriers that might now accept your property. Property improvements like roof replacement, defensible space clearing, or fire-resistant hardscaping can shift your risk profile enough to qualify for private market coverage that rejected you previously. Your broker tracks these changes and knows exactly which carriers reward risk mitigation through lower rates. If private coverage still isn’t available, your broker can restructure your FAIR Plan endorsements and DIC coverage to eliminate protections you no longer need, reducing your total premium without reducing actual coverage for the risks that matter to your property.

Final Thoughts

The California FAIR Plan exists because high-risk property California owners need access to basic fire coverage when traditional insurers won’t write policies. Understanding what the FAIR Plan covers, what it excludes, and how to layer additional protection through Difference-in-Conditions policies transforms this last-resort option into workable coverage. Rising premiums and coverage limits demand that you treat your policy as an active decision rather than a passive renewal.

Your property’s risk profile changes, carrier appetites shift, and new coverage options emerge throughout the year. Annual reviews with a licensed broker catch these changes before renewal arrives and lock in better rates or improved protection. Work with a broker who performs the mandatory market search, structures your coverage with the right endorsements and DIC wraps for your specific property, and stacks multiple policies with the same carrier to capture bundle discounts that reduce your total household insurance costs.

We at Cappuccino Insurance Agency help property owners across California navigate FAIR Plan policies and Difference-in-Conditions wraps to build coverage that actually protects their assets. Contact us for an annual policy review or to start your coverage assessment today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.