California FAIR Plan Insurance: Safeguarding Hard-To-Place Properties

California’s wildfire season grows more intense each year, leaving many homeowners unable to find coverage through standard insurance companies. At Cappuccino Insurance Agency, we understand how frustrating this situation can be.

The California FAIR Plan exists specifically for these hard-to-place properties, offering protection when private insurers won’t. This guide walks you through how it works and whether it’s the right solution for your home.

What the California FAIR Plan Actually Covers

The California FAIR Plan is a state-mandated insurance program established in 1968 to provide basic property coverage when traditional insurers refuse to write policies. It operates as a syndicated fire insurance pool backed by all licensed property and casualty insurers in California, meaning every carrier licensed to do business in the state participates in both profits and losses. This structure creates stability across different geographies and risk profiles, so your coverage does not depend on a single company’s financial health. The Plan was designed as a temporary safety net, not a permanent solution, with the explicit goal of helping homeowners until traditional carriers are willing to offer coverage again. If you own a property in California and cannot find coverage through standard channels, the FAIR Plan serves as your insurer of last resort.

How You Access the FAIR Plan

You do not apply directly to the Plan itself. Instead, you work with a licensed broker who conducts a diligent market search through traditional insurers first. Only if that search fails to produce coverage can your broker submit an application to the California FAIR Plan on your behalf at no additional cost to you. This process protects you by ensuring that brokers exhaust all traditional market options before turning to the FAIR Plan as a backup.

What the FAIR Plan Covers

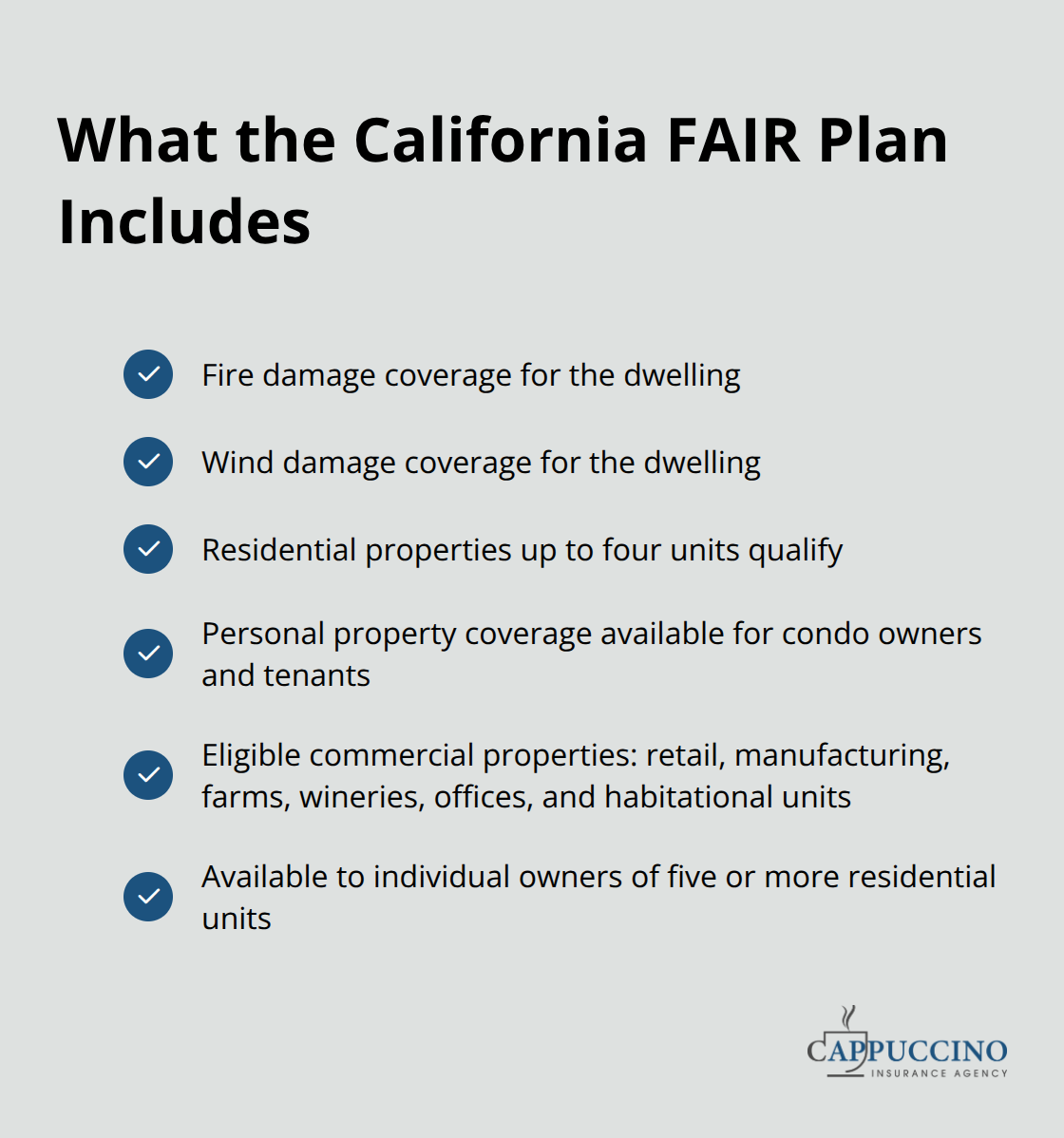

The FAIR Plan provides fire and wind coverage for residential dwellings with up to four units, whether you own the property or rent it. If you own a condo or rent as a tenant, you can insure your personal property through the Plan. Commercial properties qualify too, including retail spaces, manufacturing facilities, farms, wineries, office buildings, and habitational units.

Individual owners of five or more residential units can access FAIR Plan coverage as well. However, this is critical: the FAIR Plan covers fire and wind damage only. It does not include flood coverage, earthquake coverage, or theft. You set the dwelling coverage limit yourself with your broker based on your home’s rebuild cost, not its fair market value (these figures can differ significantly).

Coverage Gaps and Supplemental Solutions

Most homeowners find that basic FAIR Plan coverage leaves substantial gaps. A Difference-in-Conditions policy acts as a wrap that fills the holes left by the FAIR Plan, approximating a more complete homeowners policy. Flood insurance must be obtained separately and covers building damage, personal property, or both depending on your location and needs. Earthquake coverage for individual residences is available through the California Earthquake Authority, a separate program entirely. Your broker can help you layer these policies together to create comprehensive protection. Many homeowners in high-risk zones combine a FAIR Plan base policy with DIC coverage, flood insurance, and earthquake protection to achieve the security they need.

Financial Stability and Track Record

The California FAIR Plan publishes financial reports and participation data annually, providing transparency about how the program operates and its financial stability. This data shows the Plan has successfully insured high-risk properties since its creation, making it a proven mechanism for protecting homes that commercial insurers will not touch. Understanding what the FAIR Plan covers is only half the battle-knowing how to layer supplemental coverage is what transforms a basic safety net into real protection. The next section explores why properties become hard-to-place in the first place and what factors push homeowners toward the FAIR Plan.

Why Carriers Are Abandoning California Properties

The Systematic Exodus from California

California’s property insurance market has contracted dramatically over the past five years, with major carriers systematically exiting the state or tightening underwriting standards to the point where coverage becomes unattainable. Historically, California had roughly 15 major competing insurers; today that number has shrunk substantially, leaving property owners with far fewer options. Catastrophic wildfire seasons produced unprecedented claim losses, forcing insurers to reassess their entire California portfolios. This exodus accelerated after these disasters, with carriers withdrawing from entire regions rather than adjusting rates or coverage terms. Properties in wildfire-prone zones face the harshest treatment, but the problem extends well beyond fire risk alone.

Multiple Risk Factors Stack Against Homeowners

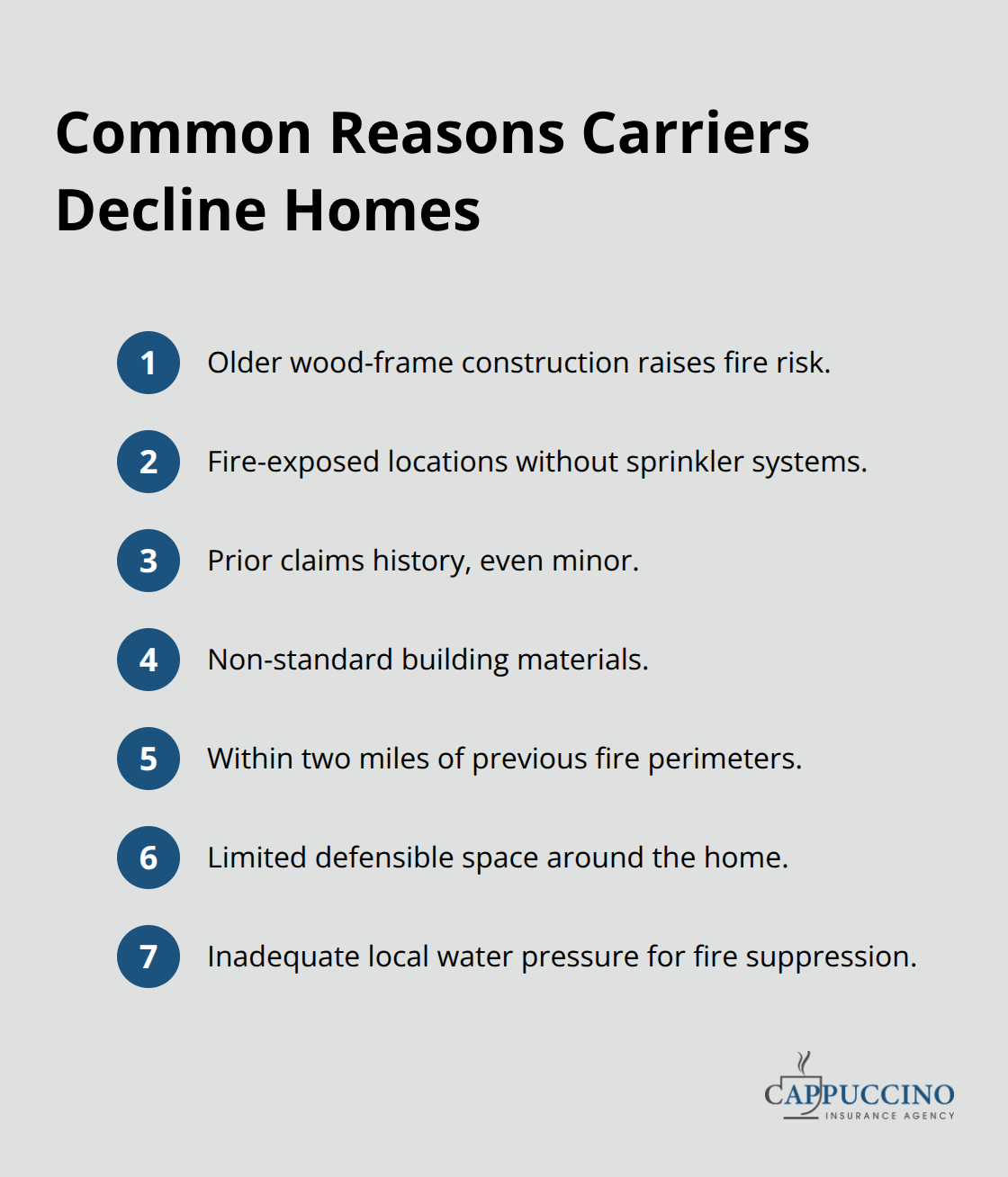

Carriers now reject applications based on multiple overlapping factors: older wood-frame construction, properties in fire-exposed locations without sprinkler systems, previous claims history regardless of severity, and non-standard building materials. A single denied claim from five years ago can disqualify a homeowner from coverage today, even if the claim was legitimate and the property has since been improved. Location compounds these challenges significantly. Homes within two miles of previous fire perimeters, in areas with limited defensible space, or in communities with inadequate water pressure for fire suppression face near-automatic rejection from traditional carriers. The California Department of Insurance reports that properties in high-fire-risk zones now represent the largest segment of FAIR Plan applicants, reflecting how systematically insurers have withdrawn from these geographies.

Why Accumulation of Risk Markers Creates Hard-to-Place Properties

What makes properties truly hard-to-place is not any single factor but the accumulation of risk markers that traditional underwriters use to decline coverage. A property with an older roof, located in a fire-prone area, with one previous claim and limited defensible space hits multiple underwriting red flags simultaneously. Each carrier maintains different appetite thresholds, meaning a property rejected by one insurer might qualify with another-but only if a broker knows which carriers currently accept those specific risk profiles. Brokers track which insurers actively write in high-risk zones and which have quietly tightened their guidelines, then position your property in ways that align with each carrier’s preferences. Without this market intelligence, property owners either overpay for coverage or receive rejections they don’t understand.

The Broker Advantage in a Constrained Market

Carriers change their underwriting appetites frequently, which requires ongoing market awareness to identify available options. A broker with current market relationships can access options that may not be readily visible to property owners attempting to shop on their own. Deep industry connections help brokers translate evolving market data into actionable placement strategies. Skilled negotiation under a constrained market can achieve favorable conditions wherever possible, and consistent communication with carriers keeps brokers informed about available products and terms. A well-packaged risk profile can look more attractive to underwriters, improving the odds of coverage approval.

The FAIR Plan exists precisely because this narrowing of options has become the default experience for thousands of California homeowners, not an outlier. Understanding how the Plan protects you when traditional carriers refuse is the next step toward securing the coverage your property needs.

How the FAIR Plan Becomes Your Real Protection

The California FAIR Plan provides fire and wind coverage, but treating it as a complete solution misses the point entirely. What actually protects you is understanding how to layer the FAIR Plan with supplemental policies to eliminate the gaps that leave homeowners exposed. When you obtain FAIR Plan coverage, you secure a foundation, not a finished structure.

The Foundation: What FAIR Plan Coverage Includes

The Plan covers dwelling damage from fire and wind, which addresses the primary peril in California’s high-risk zones, but it explicitly excludes flood, earthquake, theft, and numerous other perils that can devastate a property. This is why the California Department of Insurance recommends that homeowners view the FAIR Plan as a temporary bridge to traditional coverage rather than a permanent solution. Your broker’s role shifts dramatically in this environment-instead of simply finding you any available policy, they must construct a multi-layered protection strategy that transforms basic FAIR Plan coverage into comprehensive security.

Filling the Gaps with Supplemental Policies

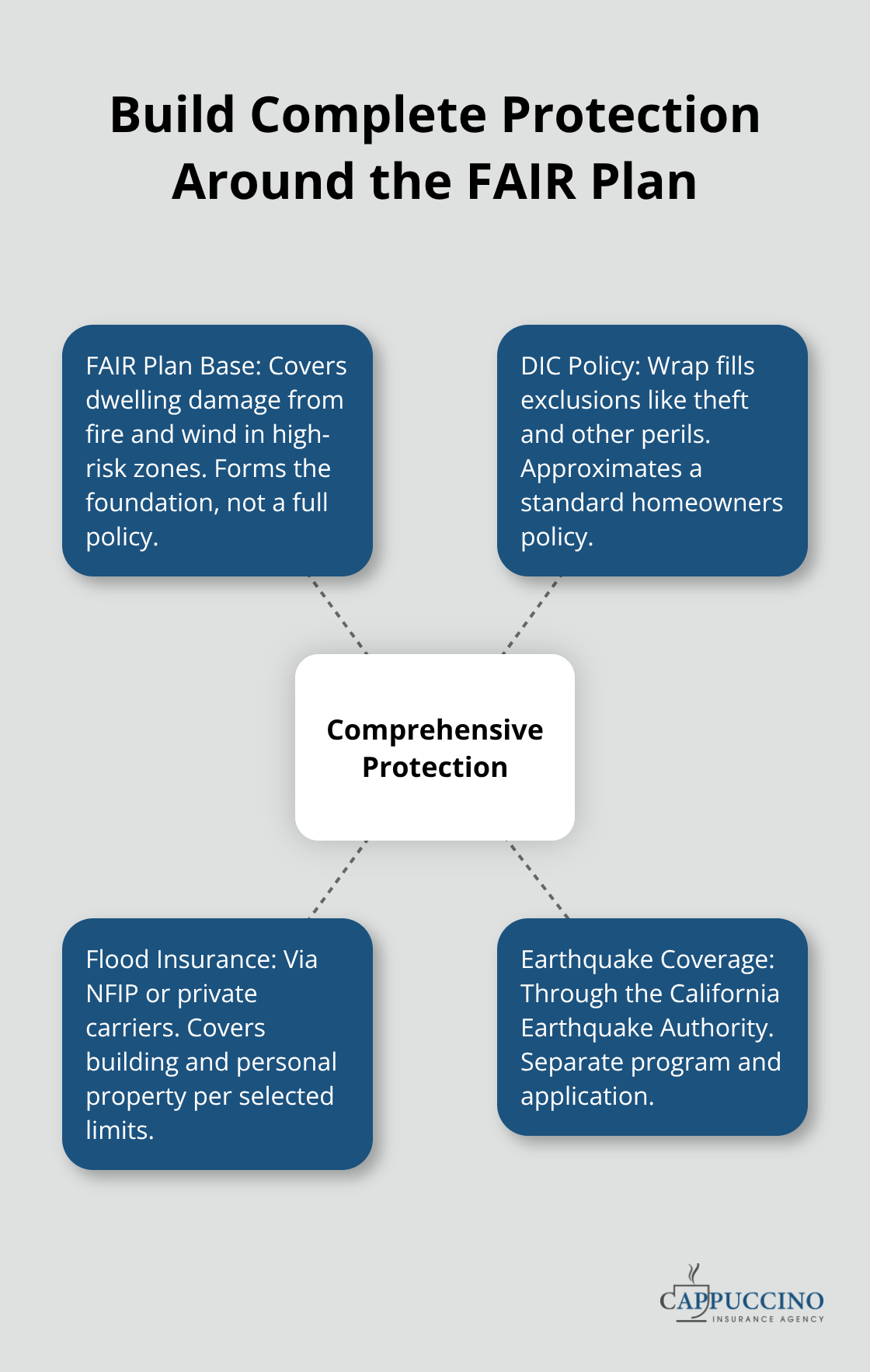

A Difference-in-Conditions policy acts as the critical wrap that fills the holes left by the FAIR Plan, approximating a full homeowners policy by covering losses the FAIR Plan excludes. Flood insurance must be purchased separately through the National Flood Insurance Program or private carriers, and it covers both building damage and personal property depending on your chosen limits. Earthquake coverage for individual residences comes through the California Earthquake Authority, a separate program with its own application process. The combination of these three components-FAIR Plan base coverage, DIC wrap, and supplemental flood and earthquake policies-creates the protection that traditional homeowners insurance would provide.

Setting Accurate Coverage Limits

You set your FAIR Plan dwelling coverage based on rebuild cost, not fair market value, and this decision directly impacts whether you can actually rebuild if a loss occurs. Many homeowners underestimate rebuild costs because they confuse property value with construction expense, leaving themselves significantly underinsured even after adding supplemental coverage. Your broker should help you calculate accurate rebuild costs by consulting local construction data and accounting for current material and labor inflation in your area.

The Hidden Exposure in Your Current Coverage

The California Earthquake Authority reports that approximately 7.5 million California residential properties lack earthquake coverage despite living in seismically active zones, exposing homeowners to catastrophic financial risk from a single peril. Similarly, flood coverage gaps are widespread because many property owners incorrectly assume their homeowners or FAIR Plan policy covers water damage, when in reality flood is almost universally excluded. A broker who understands the FAIR Plan’s limitations and knows how to efficiently layer supplemental coverages can position your property for genuine protection rather than leaving you with a false sense of security.

Final Thoughts

The California FAIR Plan insurance provides essential fire and wind coverage when traditional carriers have abandoned your property, but it functions best as a foundation rather than a complete solution. Layering supplemental policies-Difference-in-Conditions wraps, flood insurance, and earthquake coverage-transforms basic FAIR Plan protection into genuine security that actually covers the perils threatening California properties. Without this multi-layered approach, homeowners often discover too late that critical gaps remain in their coverage.

Your next step involves working with a licensed broker who understands both the FAIR Plan’s limitations and how to efficiently combine it with supplemental policies. A broker conducts the diligent market search required before FAIR Plan eligibility, then positions your property strategically to access whatever traditional coverage remains available. If traditional options truly don’t exist, your broker submits the FAIR Plan application at no additional cost to you.

Accuracy matters significantly when you set coverage limits. Calculate your rebuild cost carefully-not your home’s fair market value (these figures often differ substantially)-because underestimating this amount leaves you unable to fully reconstruct after a loss, even with supplemental policies in place. Contact Cappuccino Insurance Agency to discuss your specific situation and build a protection strategy tailored to your property’s risk profile.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.