Landlord Insurance California: Protect Your Rental Portfolio

Owning rental properties in California comes with real financial exposure. A single liability claim or property damage incident can wipe out years of rental income.

Standard homeowners insurance won’t cover your rental units, leaving you vulnerable. Landlord insurance in California is specifically designed to fill those gaps and protect what you’ve built.

What Landlord Insurance Covers in California

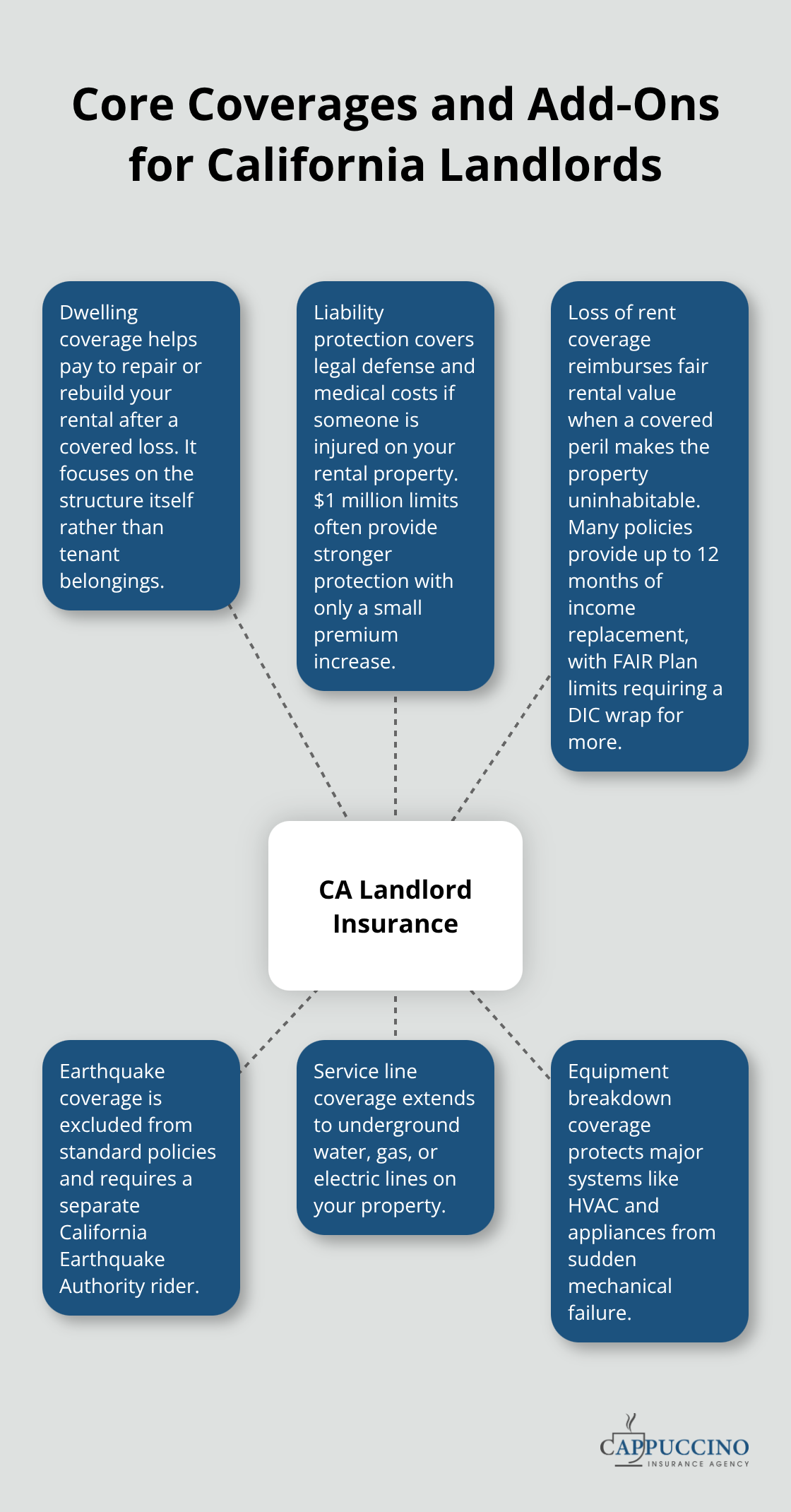

Landlord insurance in California protects three distinct areas that homeowners policies ignore entirely. The first is dwelling coverage, which helps pay to repair or rebuild your home after a covered loss. The second core component is liability protection, which covers legal expenses and medical costs if someone is injured on your rental property and sues you. Standard limits start around $300,000 for single-family rentals, but $1 million offers better protection-the premium difference is minimal. The third pillar is loss of rent coverage, which reimburses you for the fair rental value if a covered peril makes the property uninhabitable. Most policies cover about 12 months of lost income, though in California the FAIR Plan caps this at 20% of your dwelling limit, which is why pairing a FAIR Plan policy with a Difference in Conditions wrap often becomes necessary for full protection.

Property damage claims strike without warning

Fire, water damage, vandalism, and falling objects all fall under a standard DP-3 policy, which works best for most California landlords. The distinction between replacement cost and actual cash value matters enormously-replacement cost pays what it actually costs to rebuild or repair today, while actual cash value deducts depreciation, leaving you with a smaller check. In California’s high-construction-cost environment, upgrading from actual cash value to replacement cost can mean tens of thousands of dollars in your pocket after a claim. Earthquake damage is explicitly excluded from standard landlord policies and requires a separate California Earthquake Authority rider, costing roughly $35 per year for additional personal property and living expenses coverage. You can also add endorsements for service line coverage (water, gas, electricity lines on your property) and equipment breakdown protection for HVAC systems and appliances-practical additions that address real failure modes in rental properties.

Loss of rent coverage maintains your cash flow

When a covered loss occurs and your property becomes uninhabitable, loss of rent coverage activates automatically. This differs from rent guarantee insurance, which covers missed rent due to tenant nonpayment or eviction-a separate product costing 2–5% of annual rent with 6–12 months of coverage. Loss of rent from a covered peril is invaluable because it maintains your cash flow during repairs, preventing you from absorbing months of zero income while contractors rebuild. The coverage duration and limits vary by carrier and policy design, so reviewing your specific policy language matters before you need it. Understanding exactly what your policy covers sets the foundation for selecting the right protection-which is why comparing options across multiple carriers becomes your next critical step.

Why Standard Homeowners Insurance Fails Rental Properties

Explicit exclusions void your coverage

Your homeowners insurance policy contains explicit language that voids coverage the moment you rent out your property. Most carriers will deny claims on rental units outright, leaving you exposed to the full cost of repairs, liability judgments, and lost income. This isn’t a gray area or a technicality-it’s a hard exclusion written into the policy document. If a tenant’s guest suffers a serious injury on your rental property and wins a $500,000 lawsuit, your homeowners insurer will reject the claim because the property generates rental income. You would be personally liable for the entire judgment, potentially forcing you to sell the property or liquidate retirement accounts to cover it.

Liability limits leave you dangerously underprotected

The liability limits on a standard homeowners policy max out around $100,000 to $300,000, which sounds adequate until you face a catastrophic injury claim. Medical costs for permanent disability or wrongful death lawsuits regularly exceed $1 million in California, and your homeowners policy won’t contribute a single dollar to your defense. Landlord insurance starts with $300,000 in liability coverage for single-family rentals and scales to $1 million for multifamily properties-a meaningful difference that costs only slightly more in premium. This protection matters because one serious claim can destroy your financial security.

Loss of rent coverage exposes a critical gap

When a fire, roof collapse, or major water damage makes your rental uninhabitable, your homeowners policy covers the structure but leaves you absorbing months of zero income while repairs happen. Loss of rental income coverage activates automatically when a covered peril damages the property, maintaining your cash flow during repairs. Landlord policies specifically include this protection in California’s high-cost construction environment. This gap forces landlords to piece together multiple policies to achieve adequate protection.

California’s FAIR Plan requires additional protection

The FAIR Plan caps loss of rent at 20% of your dwelling limit, which means pairing it with a Difference in Conditions wrap becomes necessary-an extra step that homeowners insurance never requires because homeowners policies simply don’t address rental income at all. This gap forces landlords to piece together multiple policies to achieve adequate protection. Understanding these coverage shortfalls sets the stage for selecting the right landlord policy, which requires assessing your specific property and comparing options across multiple carriers.

Selecting the Right Policy for Your California Rental

Start by documenting exactly what you own and what risks threaten it. Photograph your rental property’s roof condition, note the year it was built, measure the square footage, list any recent upgrades or renovations, and record the current replacement cost based on contractor quotes rather than market value. The California Construction Cost Index is developed based on Building Cost Index cost indices for San Francisco and Los Angeles. Pull your property tax records and contact local contractors for actual rebuild estimates in your area. This foundation prevents the most common landlord mistake: underinsuring by using market value instead of replacement cost.

Assess your property’s specific risk profile

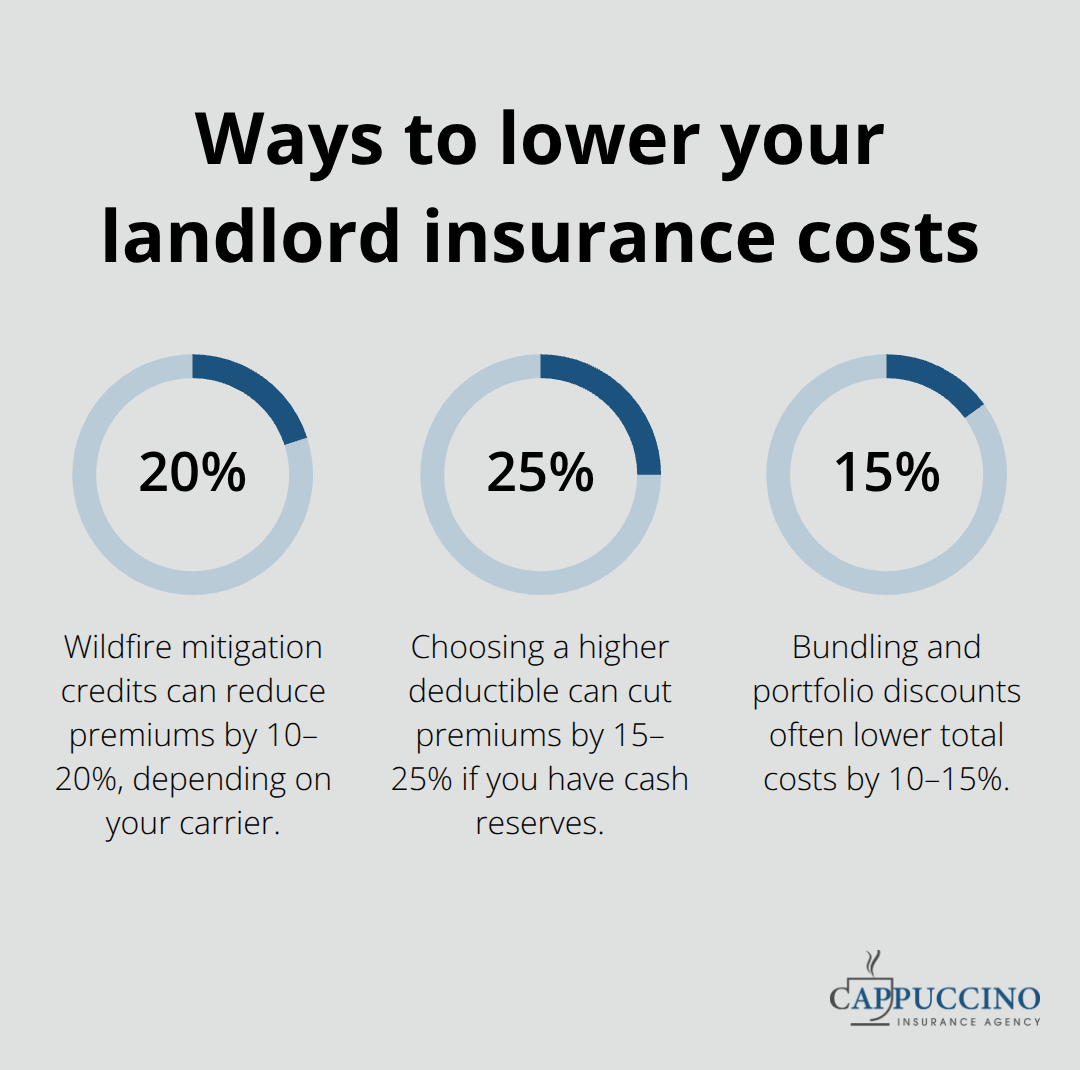

Once you know your property’s specifics, assess your risk profile by checking your property’s wildfire hazard zone, flood zone, and crime rate. Properties in California’s Very-High Fire Hazard zones cost $2,000–$3,500 annually or more, compared to $900–$1,200 for standard-risk single-family rentals statewide. If your property sits in a high-risk zone, carriers like Farmers, Travelers, Liberty Mutual, and Safeco may offer limited capacity, making the California FAIR Plan with a Difference in Conditions wrap your realistic option. Document any mitigation work you’ve completed-defensible space, metal roof upgrades, ember-resistant vents, or cleared gutters-because these credits can reduce premiums by 10–20% depending on your carrier.

Compare quotes across multiple carriers

Contact at least three to five carriers and obtain written quotes that specify replacement cost coverage, liability limits of $1 million minimum, and 12 months of loss of rent protection. Price differences between quotes routinely hit 40%, meaning a policy quoted at $1,800 from one carrier might cost $1,200 from another for identical coverage. Use platforms like Steadily and Obie for quick online quotes, but follow up with direct calls to carriers like Mercury for California-specific pricing. When comparing quotes, ignore the premium alone and examine what you’re actually buying: does the policy use replacement cost or actual cash value, what exclusions apply, how long does loss of rent coverage last, and what deductible makes sense for your cash position. A higher deductible ($2,500 or $5,000 instead of $1,000) can cut premiums 15–25% if you have emergency reserves. If you own multiple properties, ask about portfolio discounts and whether bundling with your homeowners or auto policy saves money-multi-policy discounts typically reduce total costs by 10–15%. For landlords with $500,000+ in property equity, adding a $1 million umbrella liability policy costs only $150–$300 annually and protects against catastrophic claims that exceed your base policy limits.

Select the right limits and endorsements

Your base policy should include dwelling coverage at replacement cost, $1 million liability, and 12 months of loss of rent protection. Add service line coverage for water and gas lines, equipment breakdown protection for major appliances and HVAC systems, and the California Earthquake Authority rider if you’re in a seismic zone. If you furnish the rental with appliances or furniture you own, add personal property coverage for those items. For short-term rentals on Airbnb or VRBO, standard landlord policies exclude nightly stays, so you need a home-sharing endorsement or a specialized carrier like Foremost or Proper.

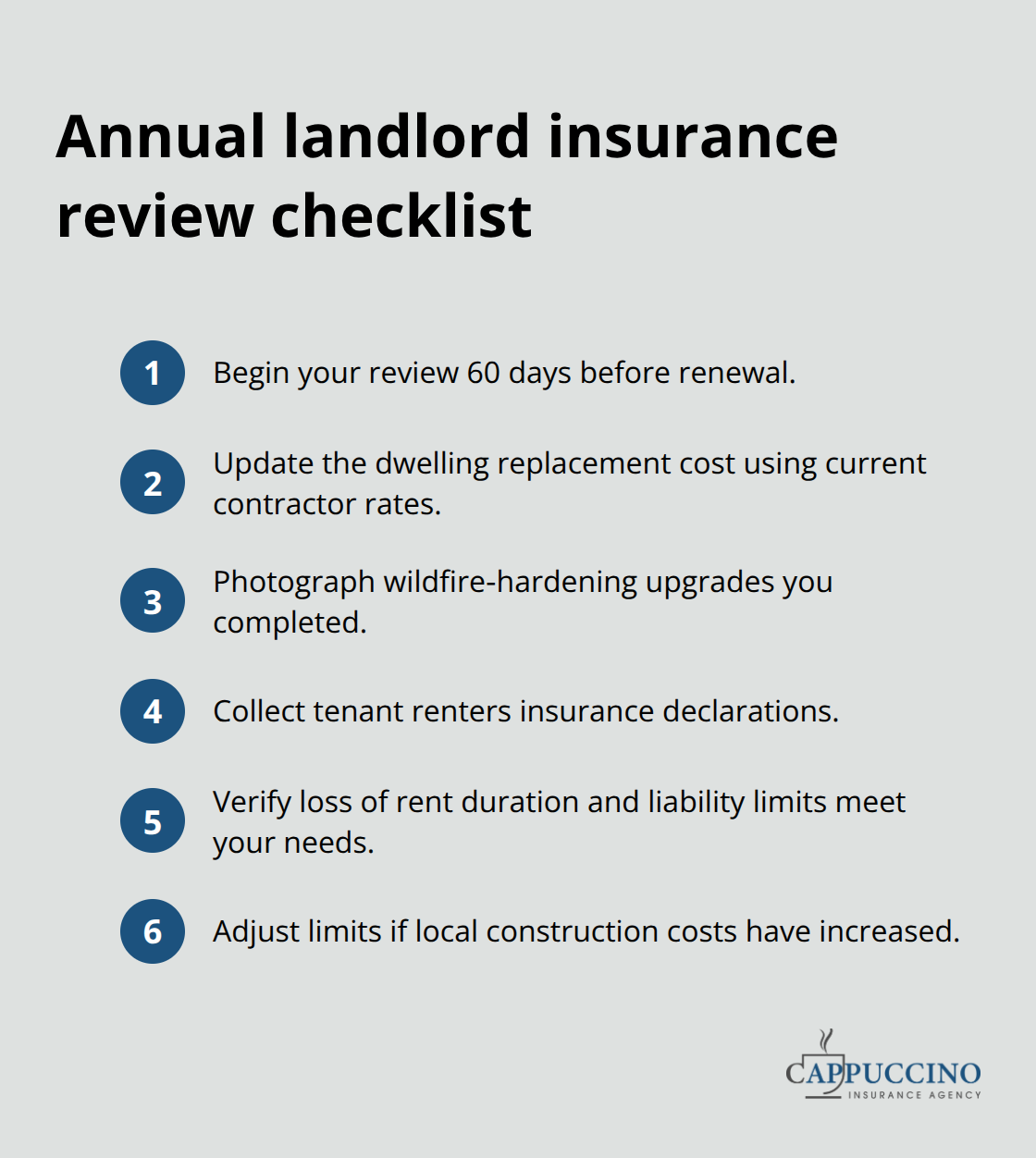

Review your policy annually before renewal

Review your policy annually 60 days before renewal, update your dwelling replacement cost based on current contractor rates, photograph any wildfire-hardening upgrades you’ve completed, and gather tenant renters insurance declarations to show your carrier you’ve shifted personal property risk away. This annual review takes 30 minutes and prevents the common scenario where you discover at claim time that your coverage limit sits $200,000 below what you actually need to rebuild. If your property value has climbed or your area’s construction costs have spiked, your old limits become inadequate fast.

Final Thoughts

Landlord insurance in California protects your rental income, property, and personal assets from the financial devastation that a single claim can cause. Standard homeowners policies won’t cover your rental units, leaving you exposed to liability judgments, repair costs, and months of lost income. The right landlord policy combines dwelling coverage at replacement cost, liability protection of at least $1 million, and loss of rent coverage for 12 months-a combination that homeowners insurance simply cannot provide.

Your next step is straightforward: gather your property details, document your replacement cost based on actual contractor quotes, and identify your risk profile by checking your wildfire hazard zone and flood risk. Then contact multiple carriers to compare quotes, because price differences routinely exceed 40% for identical coverage. Review what each quote actually includes-replacement cost versus actual cash value, liability limits, loss of rent duration, and exclusions matter far more than the premium alone.

If you own multiple properties or have significant equity, add an umbrella policy and explore portfolio discounts that can reduce your total cost by 10–15%. Contact Cappuccino Insurance Agency to secure the landlord insurance California coverage your rental portfolio actually needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.