California Commercial Auto Insurance: Solutions For Businesses And Fleets

Running a business with vehicles in California means navigating strict insurance requirements. California commercial auto insurance isn’t optional-it’s a legal mandate that protects your company, employees, and anyone else on the road.

At Cappuccino Insurance Agency, we help California businesses find coverage that matches their actual needs. The right policy can be the difference between staying operational after an accident and facing financial disaster.

Why Your Business Needs Commercial Auto Insurance

California law mandates liability coverage for all vehicles, and commercial operations face stricter requirements than personal drivers. According to California DMV regulations, commercial vehicles must carry minimum liability limits of $30,000 per person for bodily injury, $60,000 per incident for bodily injury, and $15,000 for property damage. If your business operates without proper coverage, the DMV will suspend your vehicle registration, making it illegal to operate on public roadways. The penalties extend beyond registration suspension-driving without required coverage triggers fines starting around $350, with repeat offenses resulting in fines up to $1,800 and license suspension lasting up to four years.

Personal Policies Leave Your Business Exposed

Many business owners mistakenly assume their personal auto policy covers work-related vehicle use, but personal policies explicitly exclude business operations. This gap leaves your company exposed to catastrophic financial liability if an employee causes an accident while visiting job sites, transporting equipment, or delivering goods. The distinction matters legally and financially-your insurer can deny claims if the vehicle was used for business purposes under a personal policy.

Understanding California’s Minimum Requirements

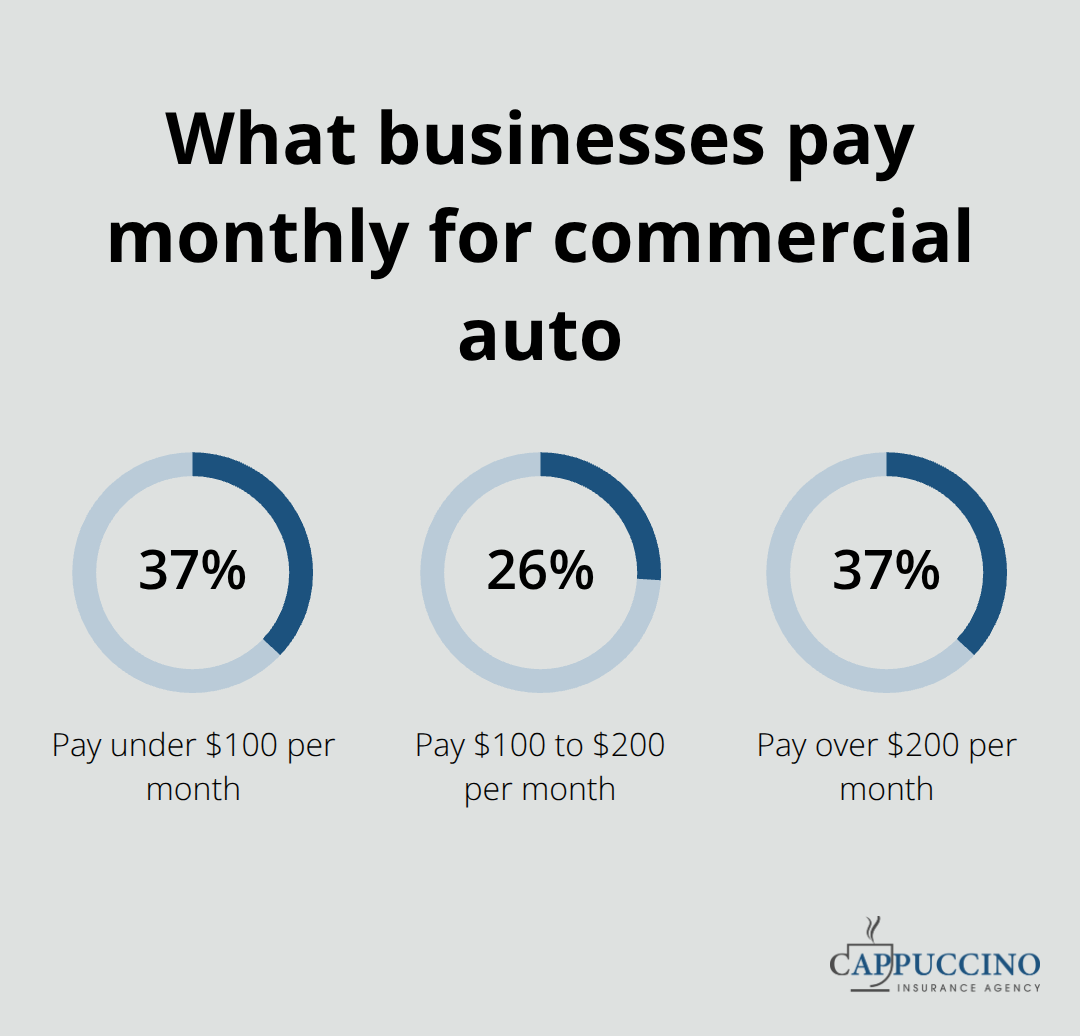

California’s minimum liability limits represent a floor, not a ceiling. A single serious accident can quickly exceed these thresholds-medical costs for severe injuries routinely surpass $100,000, and property damage claims add additional exposure. The average commercial auto insurance in California costs approximately $154 per month or $1,843 annually, according to Insureon data, but this varies significantly based on your vehicle types, industry, location, and claims history. Businesses in construction, contracting, landscaping, and delivery services face higher premiums due to increased accident risk.

Coverage That Protects Your Workforce and Assets

Uninsured and underinsured motorist coverage protects your business when another driver cannot cover damages, and this protection matters in a state where many drivers operate with minimal insurance. Medical payments coverage, or MedPay, pays for employee and passenger medical expenses regardless of fault, protecting your workforce and reducing workers compensation claims. Collision coverage handles repairs or replacement after accidents you cause, while comprehensive coverage protects against theft, vandalism, fire, and weather damage-essential for vehicles parked at job sites or left unattended.

The gap between what California requires and what your business actually needs determines whether you stay protected or face financial exposure. Understanding these coverage types helps you build a policy that matches your operation’s real risks.

Coverage That Actually Protects Your Business

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of commercial auto insurance, and California’s minimum requirements exist for a reason. The state mandates $30,000 per person for bodily injury, $60,000 per incident for bodily injury, and $15,000 for property damage according to California DMV regulations. However, these minimums apply only to third-party claims-injuries or damage you cause to someone else. A construction contractor hitting a pedestrian or a delivery driver causing a multi-vehicle pile-up can face medical bills exceeding $200,000 easily, making California’s minimum coverage dangerously inadequate for most operations. We recommend liability limits of at least $100,000 per person and $300,000 per incident for businesses operating regularly on California roads, especially those in construction, contracting, or delivery services where accident severity tends to run higher.

Collision and Comprehensive Coverage Protect Your Assets

Collision and comprehensive coverage protect your own vehicles, not third parties. Collision coverage pays for repairs or replacement after you hit another vehicle or object, regardless of fault, while comprehensive covers theft, vandalism, fire, weather damage, and other non-collision events. For businesses operating vehicles worth $15,000 or more, skipping collision coverage costs you money in the long run-a single accident can total a vehicle, forcing expensive replacement or leaving you without equipment to serve clients.

Uninsured and Underinsured Motorist Protection Fills Critical Gaps

Uninsured and underinsured motorist coverage fills a critical gap that liability alone cannot address. California has roughly 15% of drivers operating with minimal or no insurance, meaning your business faces real risk when another driver causes an accident but lacks resources to pay damages. Underinsured motorist coverage activates when the at-fault driver’s insurance maxes out below your actual damages, protecting your business from absorbing the difference.

Medical Payments and Specialized Coverage Options

Medical payments coverage, separate from these protections, pays employee and passenger medical expenses without requiring you to prove fault, reducing workers compensation claims and keeping your workforce protected on the job. For specialized operations like towing services or equipment hauling, loading and unloading coverage protects against damage to cargo during transport-a specific exposure that standard policies exclude. The combination of these coverages determines whether an accident becomes a manageable insurance claim or a business-threatening financial crisis. Selecting the right mix of protections requires understanding your specific operation and the exposures your vehicles face daily.

How to Choose the Right Coverage for Your Fleet

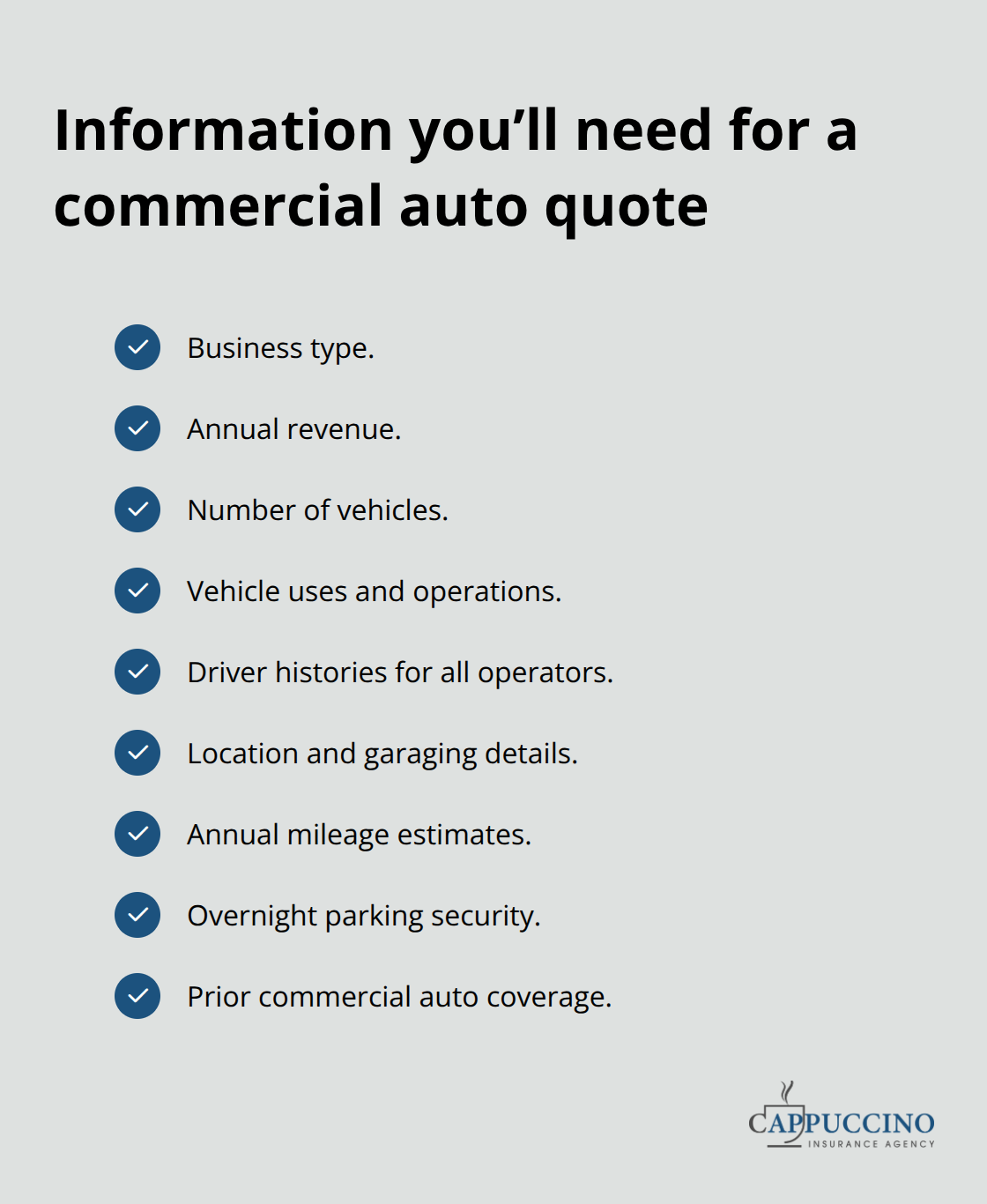

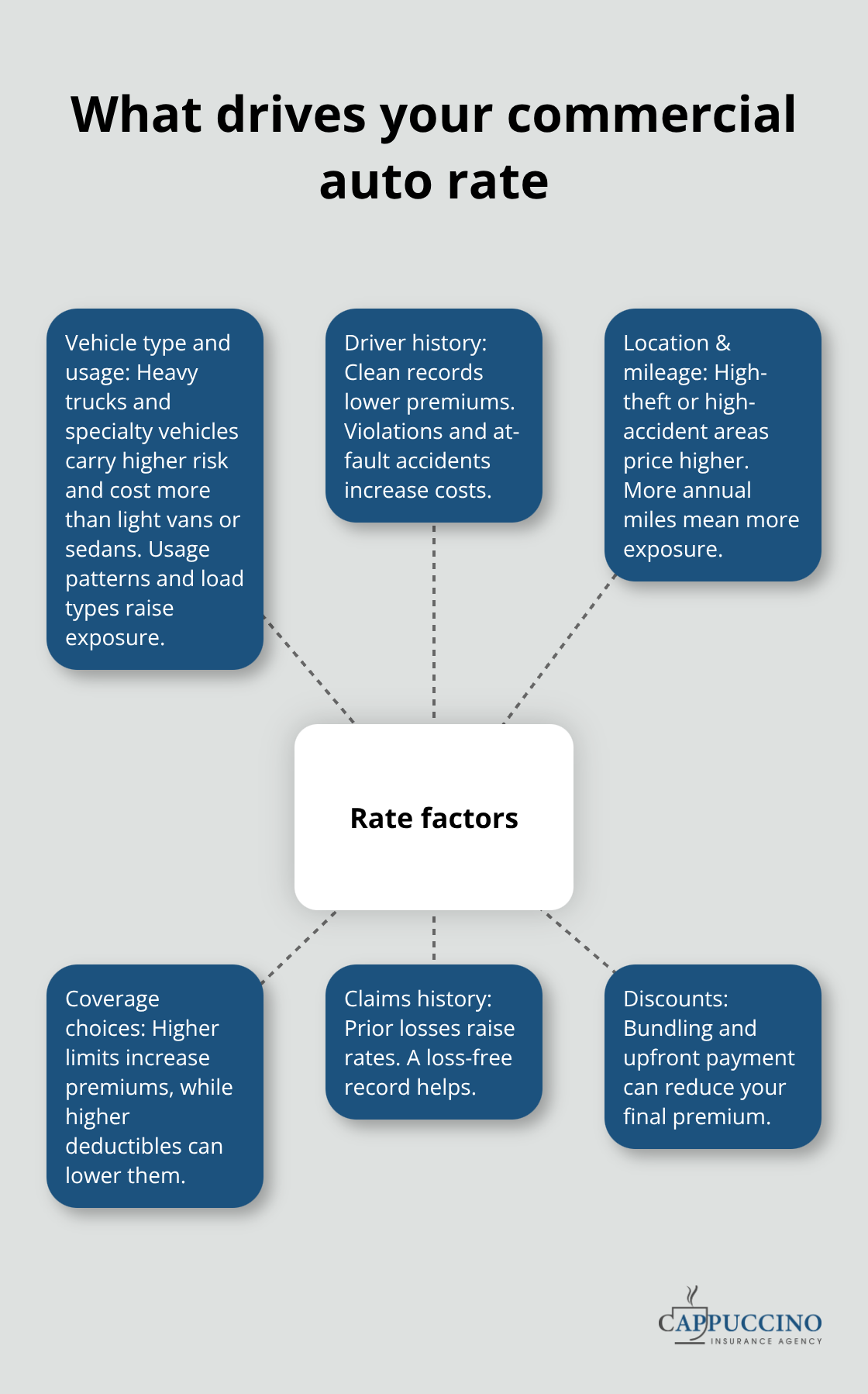

Start with a detailed inventory of your actual business operations rather than relying on industry averages. A plumbing contractor visiting three job sites daily faces different exposures than a consulting firm with one company vehicle used occasionally for client meetings. Document your vehicle types, annual mileage, cargo weight, employee count, and primary service areas-this inventory becomes your baseline for accurate quote comparisons. Insurance carriers price policies on specific operational details: vehicles worth $8,000 versus $25,000, drivers with five years of clean records versus new hires, and operations in rural areas versus dense urban centers like Los Angeles. Vague information produces quotes that don’t match your actual risk, forcing you to add coverage later at higher costs or leaving gaps unaddressed.

Request Quotes from Multiple Carriers Simultaneously

Submit your details to multiple carriers at once rather than shopping one at a time. Online platforms let you provide information once and receive multiple quotes, revealing how different carriers assess your specific operation. Some carriers specialize in construction fleets and price competitively for contractors, while others focus on service businesses or delivery operations. A landscaping company might find better rates with carriers experienced in seasonal staffing and equipment transport, while a food truck operation needs providers familiar with cargo-specific exposures. Compare not just premium costs but also coverage options-some carriers bundle hired and non-owned auto coverage automatically, while others charge extra or exclude it entirely. When you receive quotes, verify that liability limits, deductibles, and optional coverages match across proposals so you’re comparing equivalent protection levels.

Adjust Deductibles to Match Your Cash Flow

Higher deductibles reduce premiums significantly. Moving from $500 to $1,000 deductibles typically lowers annual costs by 10-15%, but only if your business can absorb that out-of-pocket expense after an accident. Test different deductible scenarios with carriers to find the balance between manageable monthly payments and acceptable financial risk for your operation.

Tailor Liability Limits to Your Operation’s Real Exposure

California’s minimum 30/60/15 liability limits provide legal compliance but inadequate financial protection for most commercial operations. A single serious accident involving employee injury, pedestrian impact, or multi-vehicle involvement easily exceeds these thresholds. Construction contractors, delivery services, and any operation with high-value cargo should carry at least $100,000 per person and $300,000 per incident liability coverage. For specialized operations like heavy equipment transport or hazmat delivery, higher limits become essential-federal regulations for vehicles with USDOT numbers may require minimum coverage exceeding California’s state mandates. Your fleet’s vehicle values also drive collision and comprehensive coverage decisions. Vehicles worth less than $5,000 may not justify collision coverage given the premium cost and deductible, but newer commercial vehicles worth $15,000 or more should carry collision protection to avoid catastrophic replacement costs.

Provide Specific Driver Information and Claim History

Carriers adjust pricing significantly based on individual driver history-one driver with a recent accident or traffic violation can increase your entire fleet’s premium by 10-20%. List actual employee names, ages, driving records, and years of experience rather than stating you have five drivers averaging 35 years old. Disclose all prior claims within the past three years, even minor incidents, because carriers discover this information during underwriting anyway. Transparency upfront prevents policy cancellations or coverage denials later when a claim occurs. Ask each carrier about available discounts specific to your operation-multi-vehicle policies typically save 10-15% per vehicle, safe driving programs like telematics reduce premiums another 5-10%, and paying annual premiums in full rather than monthly installments often saves 5%. Request quotes that include optional coverages you’re considering (medical payments coverage, uninsured motorist protection, and loading/unloading coverage) so you understand the actual cost of comprehensive protection versus stripped-down policies.

Final Thoughts

California commercial auto insurance protects your business from legal penalties, financial devastation, and operational shutdown. The coverage you select determines whether an accident becomes a manageable claim or forces your company to absorb catastrophic costs. Moving beyond California’s minimum 30/60/15 liability limits, adding collision and comprehensive protection, and including uninsured motorist coverage creates a safety net that matches your business’s real exposures.

Document your specific operations-vehicle types, annual mileage, employee count, and service areas-rather than relying on industry standards. Request quotes from multiple carriers simultaneously using this detailed information, comparing liability limits, deductibles, and optional coverages across proposals. Adjust deductibles and limits based on your cash flow capacity and actual accident risk, recognizing that higher liability limits cost less than you expect when spread across your fleet.

We at Cappuccino Insurance Agency understand that California businesses need more than generic insurance solutions. As an independent agency partnering with 20+ carriers, we deliver California commercial auto insurance tailored to your specific operation, whether you run a construction crew, delivery service, or specialized fleet. Contact us today for a personalized quote and coverage assessment that protects your assets and employees.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.