Low Premium California Homeowners: How to Get Great Coverage on a Budget

California homeowners paying too much for coverage don’t have to accept it. We at Cappuccino Insurance Agency know that low premium California homeowners can still get solid protection-it just takes strategy.

This guide walks you through exactly how insurers price policies, which discounts actually work, and how to compare quotes without settling for weak coverage.

What Actually Drives Your California Homeowners Premium

Insurance companies calculate rates using specific data points about your property and location. In California, wildfire risk dominates the pricing conversation, but it’s far from the only factor. According to data from the Terner Center analyzing California Department of Insurance records from 2018 to 2021, fire-related losses accounted for approximately 42 percent of total premiums across all loss types, with dwelling-fire policies hitting 73 percent. This concentration explains why your zip code matters so much. If you live in Elizabeth Lake, you pay around $2,273 per year for standard coverage, while Los Osos homeowners pay roughly $1,265-an 80 percent difference driven primarily by wildfire exposure. The geographic concentration is stark: 52 percent of California zip codes reported zero wildfire losses during that period, yet insurers still price in the risk across broader regions. Your home’s age and construction type hit your premium hard as well. Older homes built before 2009 cost roughly $200 per $100,000 of covered value, while newer construction runs about $150 per $100,000-a 33 percent premium for age alone. Mobile homes face the steepest costs at approximately $483 per $100,000 of covered value, making them dramatically more expensive to insure than single-family homes at $182 per $100,000.

Roof Age and Building Materials Shape Your Rate

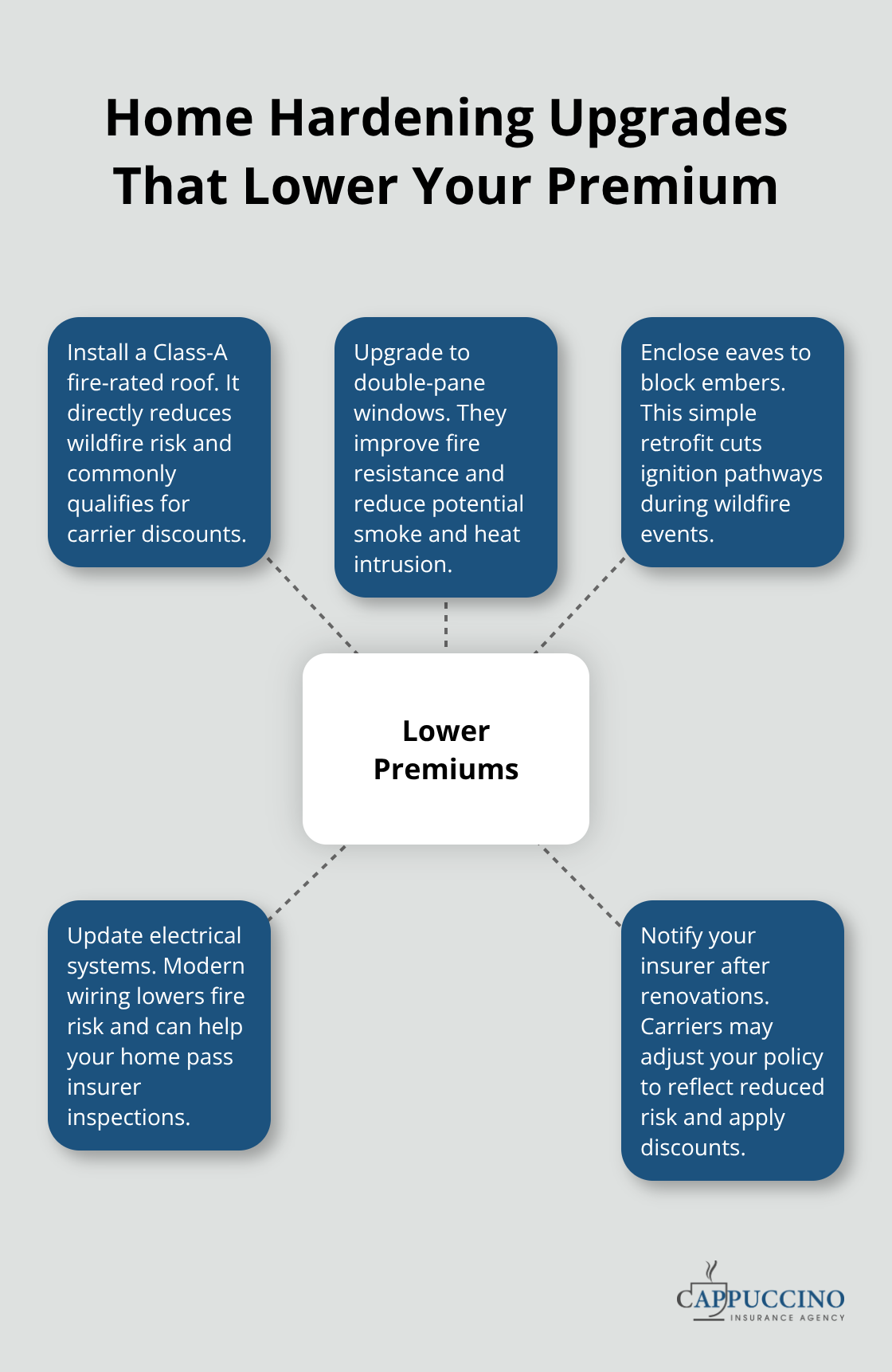

Your roof’s age and material rank among the first things insurers examine. A Class-A fire-rated roof qualifies for discounts with most carriers because it demonstrably reduces wildfire risk. If your roof exceeds 20 years old, expect your rates to reflect that vulnerability-insurers view older roofing materials as higher risk regardless of condition.

Double-pane windows, enclosed eaves, and updated electrical systems all lower your premium because they reduce both fire and water damage exposure. A home inspection will confirm these details before your policy issues, and insurers won’t hesitate to require upgrades or adjust your coverage if major components don’t meet their standards. If you’re considering renovations, prioritize your roof and windows first, then notify your insurer about completed work so your policy reflects the reduced risk.

How Location and Fire Risk Models Affect Your Quote

Insurers use detailed wildfire risk models that go far beyond simple zip code proximity to past fires. They examine fire hydrant access, defensible space around your property, local vegetation density, and historical fire patterns specific to your neighborhood. Los Angeles premiums run roughly 21 percent above the state average, not just because of wildfire but also because of higher rebuild costs and urban density. Rural properties in high-risk areas sometimes struggle to find coverage at any price, which is why the California FAIR Plan exists as the insurer of last resort. If you’re in a challenging location, an independent agent can assess whether private market options still exist or whether the FAIR Plan becomes necessary. Rate increases at renewal often signal that insurers have updated their risk models for your area-these moments are ideal times to shop around, as new carriers may price your risk differently than your current insurer.

How to Actually Cut Your California Homeowners Premium

Bundle Your Policies for Immediate Savings

Bundling your home and auto policies remains the most straightforward way to lower your overall insurance costs. Most California carriers offer multi-policy discounts ranging from 10 to 25 percent, though the actual savings depend on which insurer you choose and what coverage levels you select. If you currently insure your car and home separately, consolidating with one carrier typically saves between $200 and $400 annually. The math works because insurers reward customer loyalty and reduce their acquisition costs when they write multiple policies.

However, bundling only makes financial sense if the combined rate beats what you’d pay shopping each policy independently. Run quotes for both bundle and standalone options before committing, since a cheaper auto rate elsewhere might outweigh the bundling discount.

Raise Your Deductible Strategically

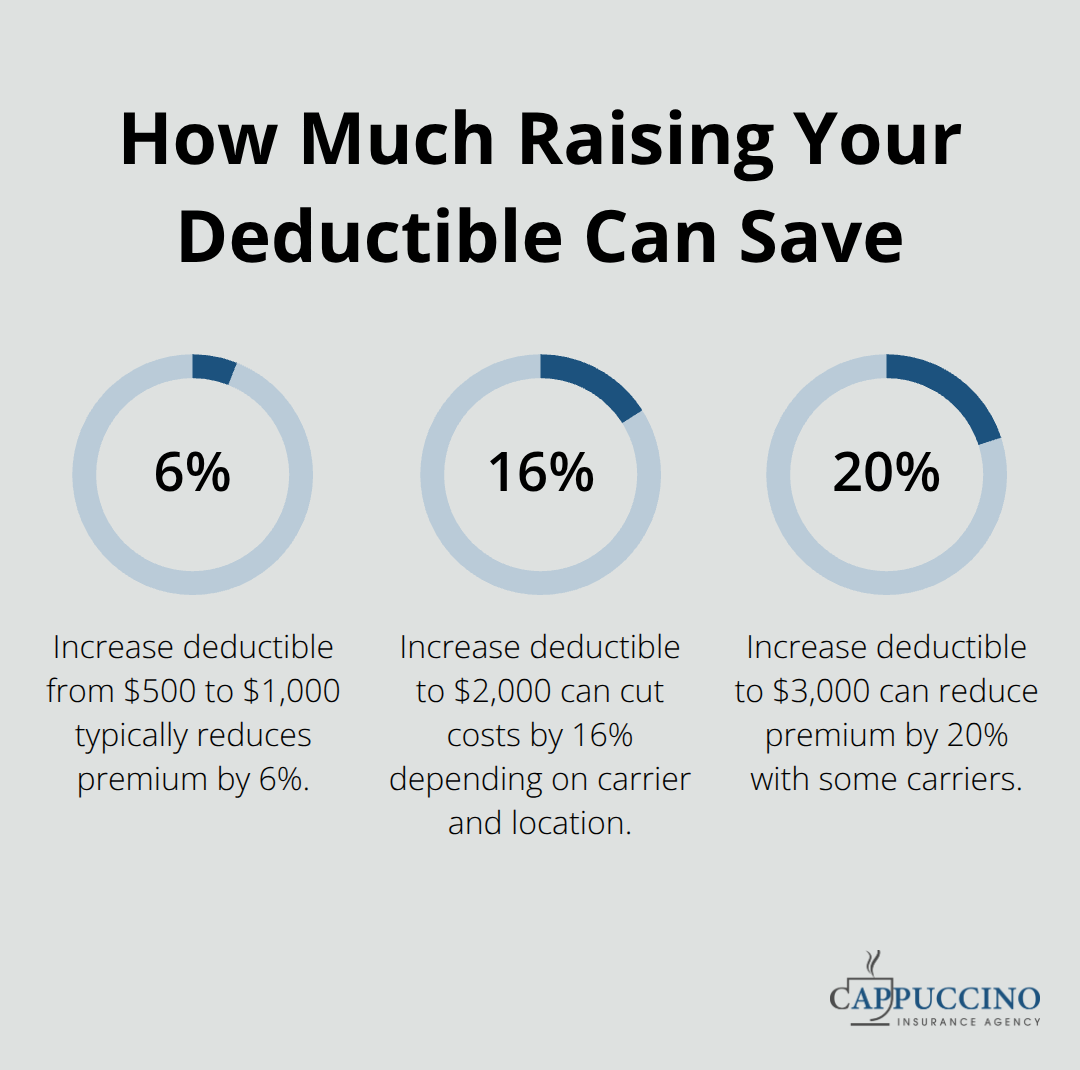

Your deductible choice directly controls your premium. Raising your deductible from $500 to $1,000 typically reduces your premium by 6 percent, while jumping to $2,000 can cut costs by 16 percent and $3,000 by 20 percent depending on your carrier and location. The catch is straightforward: you pay more out of pocket when you file a claim.

This strategy only works if you have liquid savings to cover the higher deductible without financial stress. California homeowners in stable housing situations with solid emergency funds should seriously consider the $1,500 or $2,500 deductible tier, since most claims involve smaller amounts that fall within your coverage anyway.

Install Security and Fire-Resistant Upgrades

Home security and fire-resistant upgrades deliver measurable premium reductions that most homeowners overlook. Installing a monitored security system typically qualifies for a 5 to 15 percent discount, while upgrading to a Class-A fire-rated roof can lower your premium by 10 to 25 percent depending on your current risk profile. Enclosing eaves, installing double-pane windows, and clearing vegetation within five feet of your home all reduce wildfire exposure and often trigger discounts with carriers.

The challenge is that not every upgrade qualifies for discounts with every insurer, so contact your carrier directly before spending money on renovations and ask which specific improvements they reward. After completing work, notify your insurer so your policy reflects the upgrades and you actually receive the discount. Some homeowners invest in improvements without ever mentioning them to their carrier, which means they pay the same premium for a lower-risk home.

Document your completed work with photos and keep receipts, then request a policy review to capture the savings. For wildfire-prone areas, these physical improvements sometimes matter more to insurers than your claims history, making them worth the upfront investment if you plan to stay in your home long-term.

Compare Quotes Across Multiple Carriers

Shopping around separates homeowners who overpay from those who secure genuine value. Different insurers price California risk differently based on their own loss data and underwriting models, which means your quote from one carrier can vary significantly from another. Visit multiple insurers’ websites and gather online quotes using identical coverage amounts and deductibles so you can compare apples to apples.

An independent agent can accelerate this process by accessing quotes from 20+ carriers simultaneously, saving you hours of individual website visits. These agents also understand which carriers reward specific improvements in your area and can identify discounts you might miss on your own. The effort pays off immediately-homeowners who compare quotes typically find savings of $300 to $600 annually compared to their current premium.

Getting the Right Coverage at the Best Price

Knowing your actual coverage needs separates smart shoppers from those who waste money on unnecessary protection or face gaps when claims arrive. Start by calculating your home’s replacement cost, not its market value-these are fundamentally different numbers. A home worth $800,000 on the market might cost $1.2 million to rebuild if labor and materials spike during a widespread disaster. The 80 percent rule matters here: insure your home for at least 80 percent of its replacement cost to avoid penalties when you file a claim. If you insure for less, insurers reduce claim payouts proportionally, which defeats the entire purpose of carrying coverage.

Request a professional replacement-cost estimate from your insurer or hire an independent appraiser if you’re uncertain.

Calculate Your Personal Property Coverage Accurately

For personal property coverage, most California homeowners dramatically underestimate what they own-furniture, electronics, clothing, and kitchen equipment add up fast. The Personal Property Coverage Calculator helps you itemize belongings and reach an accurate coverage amount rather than guessing. This exercise often reveals that homeowners need 30 to 50 percent more coverage than they initially thought. Taking time to list what you actually own prevents the frustration of discovering you’re underinsured after a loss occurs.

Address Coverage Gaps Standard Policies Exclude

Standard homeowners policies exclude flood damage and earthquake damage, leaving two major California risks unprotected. Earthquake coverage through the California Earthquake Authority costs roughly $1,770 annually for $500,000 in coverage, while separate flood insurance through the National Flood Insurance Program or private carriers becomes essential if you’re in a flood zone or near drainage patterns that create risk. These gaps matter more in California than most states because wildfire, earthquake, and flood risks concentrate in specific regions. Skipping these coverages to save money on your base premium often backfires when a loss occurs.

Compare Quotes Using Identical Coverage Levels

Different carriers price identical coverage differently because they weight California’s specific risks through their own loss data and underwriting models. Gathering quotes from at least three carriers using the same coverage limits and deductibles reveals genuine price differences-not variations based on different protection levels. An independent agent accessing 20+ carriers simultaneously accelerates this process and identifies discounts you’d miss shopping individually. Agents know which carriers reward fire-resistant upgrades in your specific zip code, whether your home’s age triggers penalties with certain insurers, and which companies actively write policies in wildfire-prone areas when major carriers have stopped accepting new business.

Shop at Renewal to Capture Rate Reductions

The savings materialize quickly: homeowners comparing quotes typically find $300 to $600 in annual savings compared to their current premium. Rate increases at renewal signal that your current insurer has adjusted their risk models for your area, making that renewal notice the perfect moment to shop rather than automatically renewing. This timing advantage means you can switch carriers before your rate spike takes effect, locking in better pricing with a new company. Many homeowners miss this opportunity simply because they assume renewal rates are non-negotiable.

Final Thoughts

Low premium California homeowners secure affordable coverage by taking three concrete actions: understanding what drives your premium, implementing cost-cutting strategies that actually work, and reviewing your policy annually to stay ahead of rate increases. Comparing quotes across multiple carriers typically saves $300 to $600 annually, while bundling home and auto policies cuts another $200 to $400 off your total costs. These savings compound year after year when you stay disciplined about shopping at renewal instead of accepting automatic rate increases.

Your next step is immediate: gather replacement-cost estimates for your home, calculate your actual personal property coverage needs, and confirm you’re not carrying gaps in earthquake or flood protection. Request quotes from at least three carriers using identical coverage levels and deductibles so you can compare genuine price differences rather than variations based on different protection amounts. If you’re in a wildfire-prone area or have struggled to find coverage, an independent agent can access 20+ carriers simultaneously and identify options you’d miss shopping alone.

Annual policy reviews prevent the slow creep of overpayment that catches most homeowners off guard. Rate increases at renewal signal that your insurer has adjusted their risk models for your area-that’s your signal to shop rather than renew automatically. Each year, ask your carrier which new discounts you qualify for based on completed home improvements, and request a policy review to confirm your coverage still matches your home’s current replacement cost.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.