Specialty Wildfire Coverage California: Tailored Protection For Hotspots

California’s wildfire season grows more intense each year, putting homeowners in high-risk zones under constant pressure. Standard insurance policies often leave dangerous gaps in coverage when fires strike.

At Cappuccino Insurance Agency, we’ve helped countless property owners navigate specialty wildfire coverage in California to find protection that actually matches their exposure. This guide walks you through your real options.

California’s Wildfire Threat: What Homeowners Face Today

The Scale of California’s Fire Problem

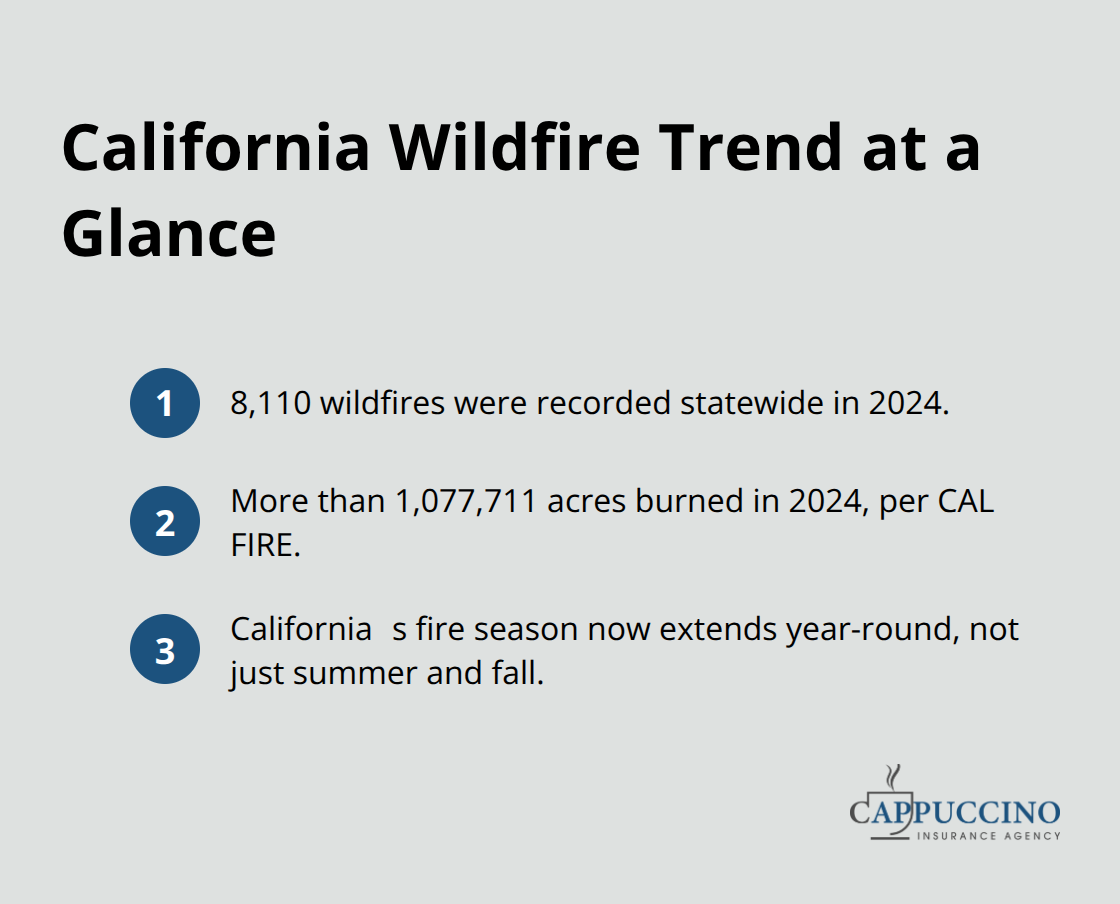

California experienced 8,110 wildfires in 2024 alone, which burned over 1,077,711 acres according to CAL FIRE data. This represents a consistent upward trend over the past two decades, with the state averaging roughly 7,000 fires annually since 2015. The 2023 fire season produced particularly destructive megafires, and 2024 continued that pattern with multiple large incidents that destroyed thousands of homes. What makes this trend alarming is that fire seasons now extend year-round rather than peak in summer and fall-recent fires have ignited in winter months when homeowners historically felt safer.

Your property faces wildfire exposure during months when many people drop their guard entirely.

How Climate Change Rewrites Fire Dynamics

Climate change has fundamentally altered California’s fire dynamics in ways that standard homeowner policies simply don’t account for. Rising temperatures dry out vegetation faster, which creates more combustible fuel across broader landscapes. According to research from the California Department of Insurance, the hazard assessment used to map fire risk zones covers a 30 to 50-year horizon and does not factor in mitigation measures like defensible space or home hardening. Official fire hazard severity zones classify your property’s danger based purely on physical conditions without considering any protective steps you have already taken.

Why Embers and Location Matter Most

Homes in State Responsibility Areas designated as Very High fire hazard severity zones face genuine exposure-embers alone can ignite buildings up to about a mile away from the main fire front (which is why exterior materials and clearance matter so critically). Properties in moderate to high hazard zones are not safe either; they simply face lower frequency but still catastrophic potential loss. The geographic pattern is stark: coastal mountain ranges, inland valleys, and foothill communities throughout Northern and Central California experience the highest concentration of destructive fires. Southern California’s San Diego County, Ventura County, and Los Angeles County areas have seen repeated major incidents.

Why Your Zip Code Determines Your Insurance Options

This geographic concentration means your zip code largely determines your wildfire insurance options and costs far more than your home’s construction quality or age. Understanding where your property sits within California’s fire hazard landscape is the first step toward securing adequate protection. The next section explores the specialty coverage options that actually address these regional and structural vulnerabilities.

Your Coverage Options When Standard Insurance Falls Short

Why the FAIR Plan Falls Short for Most Homeowners

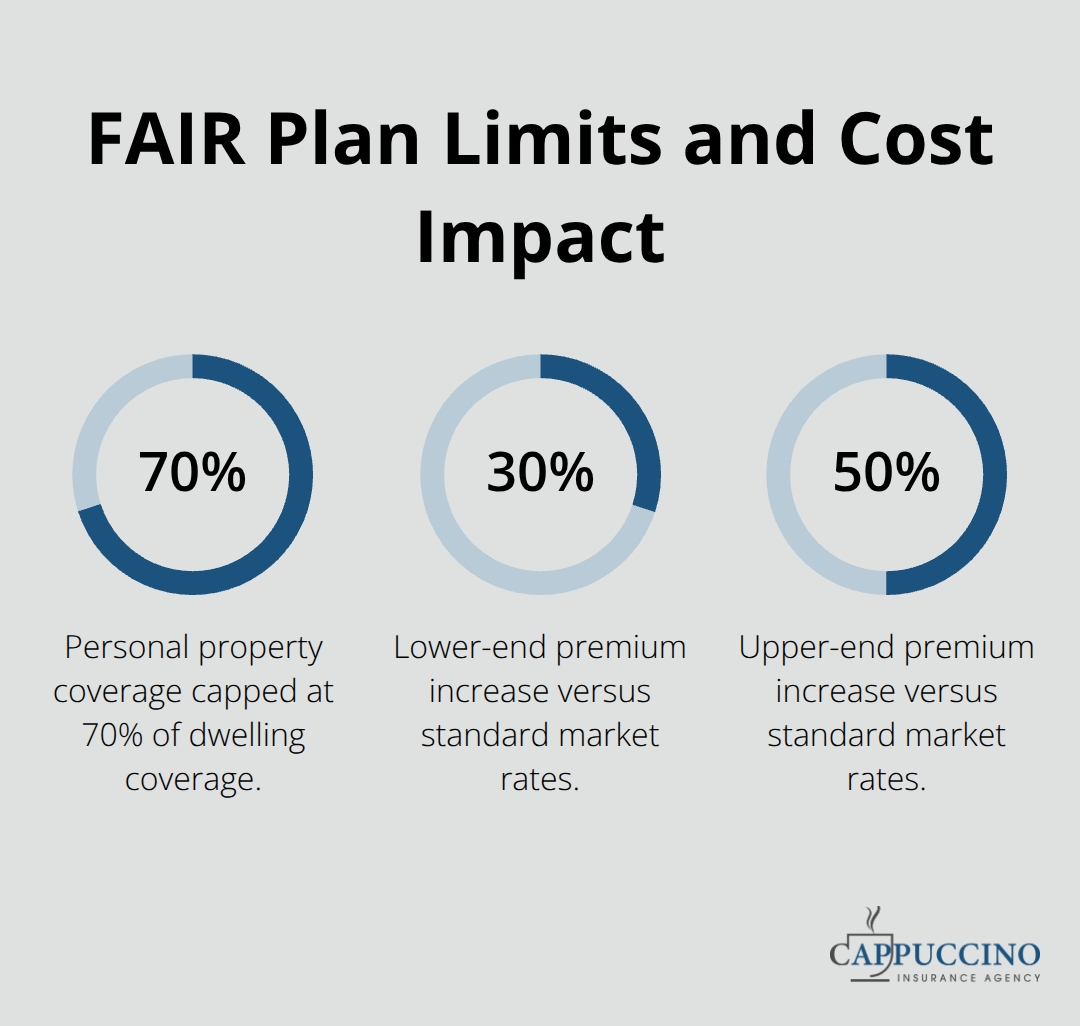

California’s FAIR Plan exists precisely because standard insurers have largely abandoned high-risk wildfire zones. The plan functions as a last-resort carrier of record, meaning if you cannot obtain coverage in the private market, you can access it through your state. However, we need to be direct: FAIR Plan coverage carries significant limitations that leave most homeowners dangerously underprotected. The plan covers dwelling, other structures, and personal property, but it excludes loss of use coverage entirely and caps personal property at 70 percent of dwelling coverage. For a home with a replacement cost of $1.5 million in a very high fire hazard severity zone, this creates a protection gap that could cost you hundreds of thousands out of pocket when a fire strikes.

FAIR Plan premiums also tend to run 30 to 50 percent higher than standard market rates for comparable properties, and availability fluctuates based on state enrollment thresholds.

How Difference-in-Conditions Wraps Close Coverage Gaps

Difference-in-Conditions insurance wraps fill the exact gaps that FAIR Plan leaves open. These wraps add loss of use, additional living expenses, and enhanced personal property limits on top of your base FAIR coverage. They also typically include coverage for debris removal and other costs that standard FAIR policies exclude. A wrap transforms your FAIR Plan from a bare-minimum solution into actual protection that addresses the financial realities of wildfire displacement and recovery. The combination of FAIR Plan plus a quality wrap provides substantially better protection than either product alone, though the layered approach requires coordination between two separate policies.

Private Market Solutions for High-Value Properties

Private market solutions from carriers like PURE Programs offer broader coverage with granular pricing that rewards specific risk-reduction measures you implement. PURE targets homes with rebuilding costs exceeding $1.5 million and provides in-house claims adjusters, proactive wildfire mitigation assessments, and emergency response support during active fires. The Wildfire Mitigation Program component includes vulnerability inspections and up to $2,500 in loss prevention benefits to reduce future damage likelihood. These specialized carriers understand California’s specific wildfire dynamics in ways the FAIR Plan simply cannot accommodate.

How Your Property Profile Determines Available Options

Your property’s hazard zone classification, construction materials, defensible space compliance, and proximity to community hardening efforts all influence what coverage options remain available and at what cost. A home with Class-A fire-rated roofing, noncombustible exterior materials, and verified defensible space qualifies for better pricing and broader coverage terms than an identical home without these protections. Properties in moderate hazard zones typically access private market solutions more easily than those in very high zones, where FAIR Plan or specialty E&S carriers become your primary options. An independent agent who understands both the FAIR Plan’s limitations and the specialty market alternatives can identify which path makes financial sense for your specific situation. The next section walks you through the assessment process that determines your actual risk level and narrows your realistic coverage options.

How to Assess Your Property and Secure the Right Coverage

Identify Your Fire Hazard Severity Zone

Start by obtaining your property’s official fire hazard severity zone classification through the California Department of Insurance’s Fire Hazard Severity Zone map viewer. Enter your address at the FHSZ map tool to determine whether your home falls into Moderate, High, or Very High designation. This classification matters because it directly constrains which carriers will underwrite your property and at what price. Homes in Very High zones face genuine difficulty accessing private market coverage, pushing you toward FAIR Plan or specialty E&S carriers like PURE Programs. If you cannot access the map online, contact the California Department of Insurance hotline at 916-633-7655 or email FHSZinformation@fire.ca.gov for assistance.

Document Your Property’s Protective Features

Once you know your hazard zone, photograph your current exterior conditions: roof material and age, siding composition, vegetation clearance distances, and fence construction. These specifics determine whether you qualify for wildfire hardening discounts that can reduce your premium by 5 to 12.5 percent depending on the carrier. AAA Home Insurance now offers its My Home Hardening discount with up to 12.5 percent savings for policies effective after October 10, 2025, rewarding individual protective measures in 0.5 percent increments for items like Class-A fire-rated roofing, enclosed eaves, noncombustible vents, and defensible space compliance. Document any community hardening participation through Firewise USA or Fire Risk Reduction Community designation, as these can contribute additional discounts up to 5 percent. This documentation phase takes roughly two hours but directly influences your available options and costs.

Request Quotes from Specialized Carriers

Next, request quotes from at least three carriers that serve your specific hazard zone rather than shopping broadly. PURE Programs specializes in homes exceeding $1.5 million rebuilding cost and offers granular pricing that rewards risk reduction, in-house claims adjusters, and $2,500 annual loss prevention benefits. Standard market carriers typically decline Very High zone properties entirely, making FAIR Plan your fallback with its higher premiums and limited coverage. An independent agent who understands both paths can access FAIR Plan plus difference-in-conditions wraps that add loss of use coverage, additional living expenses, and enhanced personal property limits that FAIR excludes entirely.

Compare Coverage, Not Just Price

The combination of FAIR plus a quality wrap costs roughly 30 to 50 percent more than standard market rates but delivers substantially better protection than FAIR alone. Compare not just premium cost but actual coverage limits, deductible structures, and exclusions across your quotes. A policy with lower premium but higher deductibles or missing loss of use coverage creates false economy when displacement costs run $50,000 to $150,000 during recovery.

Cappuccino Insurance Agency partners with 20+ carriers to deliver specialty solutions for hard-to-place wildfire properties, including FAIR Plan options and difference-in-conditions wraps, plus free coverage assessments that identify exactly which gaps exist in your current protection. Annual policy reviews before busy seasons allow you to adjust coverage as property improvements reduce risk or market conditions shift.

Final Thoughts

Wildfire protection in California demands that you move beyond standard insurance assumptions and confront your property’s actual exposure. If you live in a moderate, high, or very high fire hazard severity zone, your standard homeowner policy likely leaves dangerous gaps when fires strike. Specialty wildfire coverage California options exist specifically to address these gaps, but they require active engagement rather than passive policy holding.

The assessment process takes genuine effort-you need your hazard zone classification, documentation of protective features, and quotes from carriers that actually serve your risk profile. This work pays dividends because it reveals exactly which coverage options remain available and what each costs. FAIR Plan coverage provides a safety net when private markets close, but difference-in-conditions wraps transform that bare-minimum protection into actual financial security by adding loss of use coverage and enhanced personal property limits that FAIR excludes.

Local expertise matters enormously in high-risk areas because wildfire insurance operates differently than standard homeowner coverage. Carriers apply different underwriting standards, pricing models, and coverage terms based on California’s specific fire dynamics. Contact an independent agent who specializes in wildfire coverage, obtain your hazard zone classification, and request quotes from at least three carriers that serve your specific risk profile-then schedule your free coverage assessment with Cappuccino Insurance Agency to identify exactly which gaps exist in your current protection.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.