Landlord Insurance Premiums California: How to Budget Without Surprises

Landlord insurance premiums in California can feel unpredictable, especially when rates shift without warning. We at Cappuccino Insurance Agency know that unexpected cost spikes derail even the most careful budgets.

This guide walks you through the real factors that shape your premiums and shows you concrete ways to control them. You’ll learn how to plan ahead so insurance costs never catch you off guard.

What Actually Drives Your Landlord Insurance Cost in California

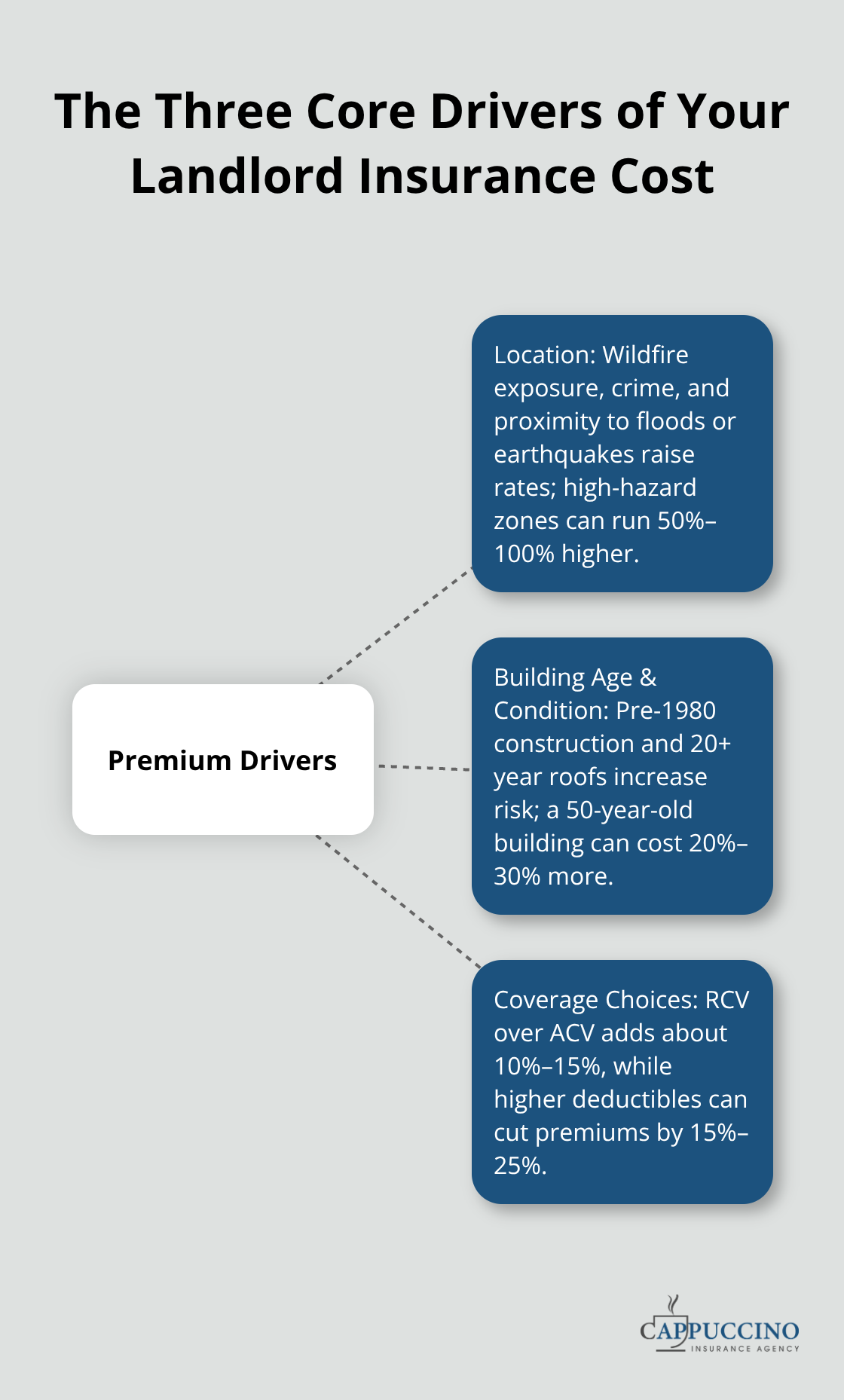

Location Creates the Biggest Premium Gap

Your location determines your premium more than almost any other factor. Properties in fire-prone areas like the Inland Empire, including cities such as Highland and Yucaipa, face significantly higher costs due to wildfire exposure. A single-family rental in suburban Los Angeles with $480,000 in dwelling coverage might cost around $1,260 annually for that coverage alone, while an identical property in a high fire-hazard zone could cost 50% to 100% more.

Crime rates matter too. Areas with higher theft or vandalism claims push insurers to charge more because claim frequency directly correlates to premium pricing. If your property sits near a flood plain or in an earthquake-prone neighborhood, expect additional surcharges or policy exclusions unless you purchase separate coverage. Location accounts for roughly 40% of premium variation between properties of similar size and condition.

The number 100% seems to be not appropriate for this chart. Please use a different chart type.

Building Age and Condition Shape Your Rate

Properties built before 1980 typically cost more to insure because older construction materials and electrical systems increase fire risk and repair costs. A 50-year-old building might cost 20% to 30% more than a newly constructed equivalent. Your roof condition matters intensely-insurers often require roof inspections, and roofs over 20 years old can trigger rate increases or coverage denials.

A well-maintained property with recent updates, modern plumbing, and updated electrical systems qualifies for better rates. Tenant type affects pricing significantly too. Long-term rentals to stable tenants cost substantially less than short-term or vacation rentals because turnover creates higher claim frequency. Some insurers won’t even cover short-term rentals without substantial premium increases.

Coverage Choices Control Your Bottom Line

Your coverage selections directly control cost. Selecting Replacement Cost Value (RCV) instead of Actual Cash Value (ACV) increases your premium by roughly 10% to 15%, but protects you from depreciation losses after a major event. A $1 million liability limit costs more than a $300,000 limit, and higher deductibles (like $2,500 instead of $500) reduce premiums by 15% to 25%.

California properties average around $1,700 annually for standard coverage, but this range spans from $700 for low-risk single-family homes to $8,300 for high-value properties in hazardous zones. Understanding these three cost drivers-location, building characteristics, and coverage selections-positions you to make informed decisions about where to invest in protection and where to adjust limits. The next section shows you how to actively reduce these costs through strategic policy choices and maintenance decisions.

How to Actually Lower Your Landlord Insurance Costs

Bundle Policies for Immediate Savings

Bundling policies delivers the most immediate savings, and California insurers reward multi-policy customers aggressively. If you carry auto, home, or commercial coverage alongside landlord insurance, combining them under one carrier typically cuts 10% to 25% off your total premium bill. A landlord with bundled auto and landlord policies might save $300 to $500 annually compared to separate policies.

Shop this aggressively-prices vary by up to 40% between carriers for identical coverage. Farmers, Travelers, Liberty Mutual, and Safeco all offer competitive bundled rates, so comparing quotes across multiple carriers reveals genuine savings opportunities. An independent insurance agency can accelerate this process by accessing quotes from 20+ carriers at once, saving you hours of phone calls and paperwork.

Maintain Your Property to Lower Claims

Loss prevention directly influences what insurers charge because claims data proves that well-maintained properties file fewer claims. Deadbolts, security cameras, and smoke detectors reduce premiums by 5% to 10%. Roof maintenance matters enormously-keeping your roof under 20 years old prevents rate increases and coverage denials that cost far more than preventive repairs.

Requiring tenants to carry renters insurance through your lease protects your liability exposure and signals to insurers that you manage risk responsibly, which can lower rates. Property managers who conduct regular inspections and maintain vendor networks for quick repairs reduce claim frequency and severity, which translates to lower premiums over time.

Review Coverage Limits Annually

Annual policy reviews catch outdated coverage limits and identify new discounts that emerged since your last renewal. Many California landlords discover that their dwelling coverage significantly exceeds current replacement costs, allowing them to lower limits and reduce premiums without sacrificing protection.

Review your policy each year alongside your property manager or insurance agent to align coverage with your actual property value and risk profile rather than keeping limits static. This simple step often reveals $200 to $400 in annual savings that accumulate over years of ownership.

These cost-reduction strategies work best when combined with accurate budgeting practices. Understanding what you currently pay and planning for future increases ensures that insurance costs never derail your rental property cash flow.

How to Build a Landlord Insurance Budget That Actually Works

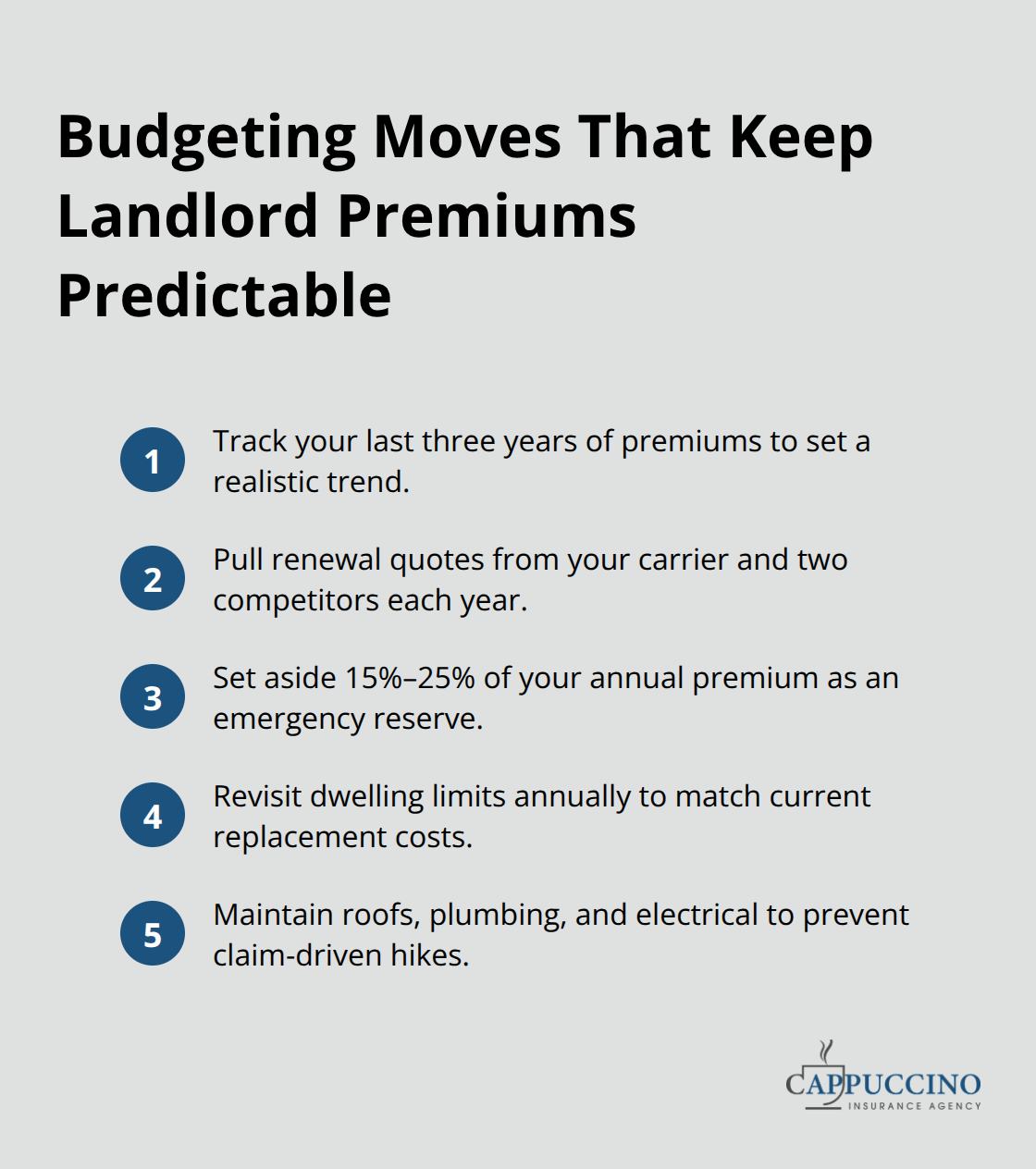

Track Your Actual Premium History

California landlords face premium increases of 7.8% annually, making static budgets obsolete within months. You should track your actual premiums over the past three years to identify your specific trend line rather than relying on statewide averages that may not reflect your property’s risk profile. If your premiums climbed from $1,400 to $1,550 to $1,720 over three years, that’s roughly 10% annual growth, which means next year’s budget should anticipate approximately $1,890.

Properties in fire-prone areas like the Inland Empire often experience steeper increases because insurers continuously adjust rates based on wildfire claims data, so your historical trend matters more than generic projections. Pull renewal quotes from your current carrier and two competing carriers each year, even if you don’t switch, because rate shopping reveals whether your increases reflect market-wide trends or your carrier’s specific risk assessment.

Shop Aggressively to Catch Rate Disparities

A landlord who discovers their carrier increased rates 18% while competitors raised rates only 8% has concrete justification to switch carriers and recover hundreds of dollars annually. This comparison takes roughly two hours but often yields $300 to $600 in annual savings that compound over years of ownership.

An independent insurance agency can accelerate this process by accessing quotes from 20+ carriers at once, saving you hours of phone calls and paperwork. The effort you invest in shopping prevents overpaying for coverage that competitors offer at substantially lower rates.

Build Emergency Reserves for Insurance Surprises

Emergency reserves for insurance represent 15% to 25% of your annual premium, which accounts for rate spikes, deductible payments after claims, and policy adjustments when property conditions change. A landlord paying $1,700 annually should maintain a $255 to $425 reserve fund specifically for insurance surprises, separate from maintenance reserves.

When your roof ages past 20 years or your property experiences a claim, expect your next renewal to cost substantially more-sometimes 20% to 40% higher-which depletes unprepared budgets instantly. Setting aside $50 monthly for insurance contingencies prevents scrambling to cover premium increases or claim deductibles from operating income.

Integrate Insurance Reserves Into Your Property Tracking

Many California landlords integrate insurance reserves into their property management software alongside rent collection and maintenance tracking, creating visibility into total annual housing costs. Property owner insurance with multiple units compounds this need because a single claim affecting one unit can trigger rate increases across your entire portfolio, making reserves even more critical for multi-property owners.

This integrated approach prevents insurance costs from surprising you at renewal time and ensures that premium increases fit within your overall investment strategy rather than forcing reactive decisions.

Conclusion

Landlord insurance premiums in California respond directly to three factors you control: your location and building condition, your coverage selections, and your willingness to shop aggressively at renewal time. Tracking your actual premium history over three years reveals your specific cost trajectory far better than statewide averages, and comparing quotes across multiple carriers typically uncovers $300 to $600 in annual savings that most landlords leave on the table. Setting aside 15% to 25% of your annual premium as an emergency reserve prevents rate spikes or claim deductibles from derailing your cash flow.

We at Cappuccino Insurance Agency work with landlords across California who manage wildfire risk, high-value properties, and complex multi-unit portfolios. Our team accesses quotes from 20+ carriers and conducts free coverage assessments to identify gaps and savings opportunities specific to your property, then handles annual policy reviews and manages specialty coverage for hard-to-place properties. Contact Cappuccino Insurance Agency to pull your last three renewal statements and compare competitive quotes from multiple carriers in your market.

This single action typically reveals whether you pay market rates or overpay for coverage that competitors offer at substantially lower costs. The time investment pays for itself within months through premium savings that compound across years of property ownership.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.