Commercial Auto Insurance California: Competitive Quotes From Local Experts

Running a business in California means your vehicles face real risks on the road. Commercial auto insurance California isn’t optional-it’s a legal requirement that protects your company from accidents, liability claims, and financial disaster.

We at Cappuccino Insurance Agency help California business owners find competitive quotes that actually fit their budget and coverage needs. This guide walks you through what you need to know to make the right choice.

Why Commercial Auto Insurance Matters in California

Rising Accident Rates and Liability Costs

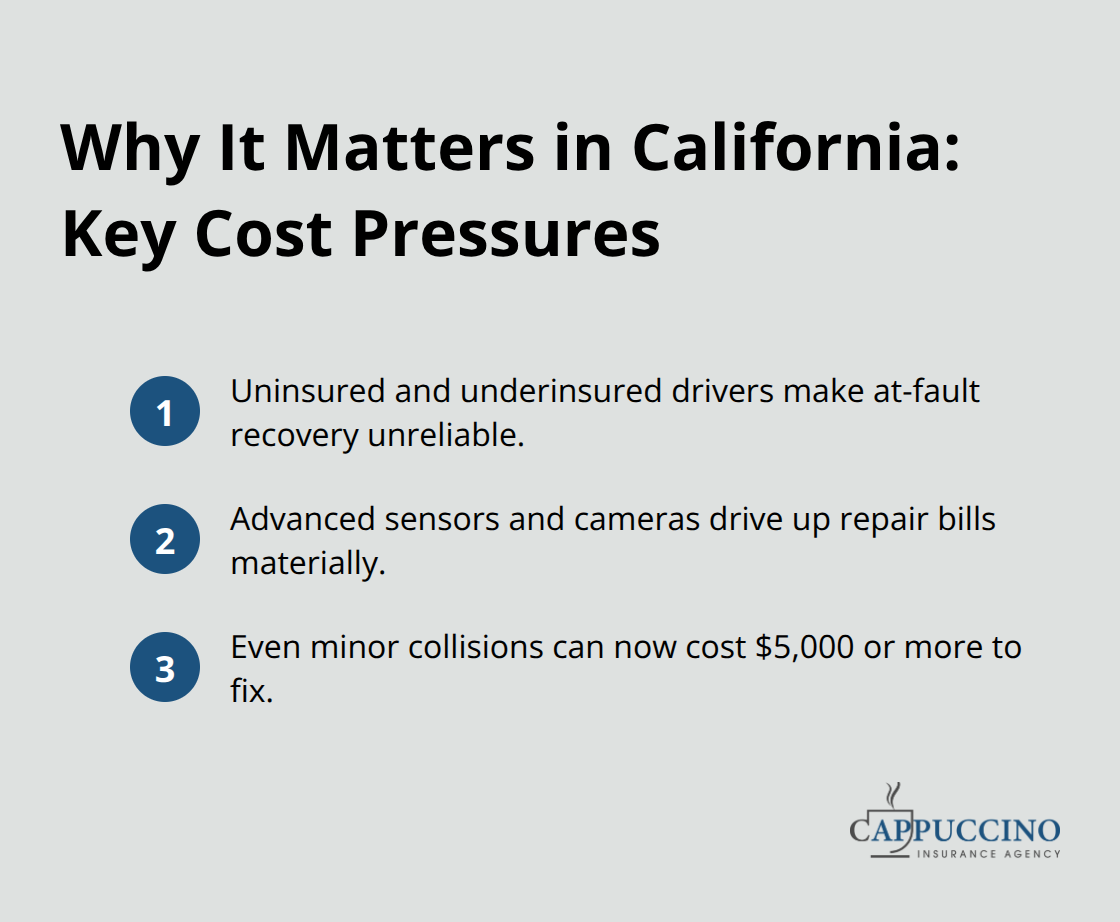

California’s accident rates and liability costs have reached levels that make commercial auto insurance non-negotiable for business owners. Nearly 1 in 5 California drivers is uninsured or underinsured, which means if one of your vehicles is hit, you cannot rely on the other driver’s policy to cover your losses. Repair costs have skyrocketed due to advanced vehicle technology like sensors and cameras that are now standard on most vehicles. A minor fender-bender that costs $2,000 to repair a decade ago now runs $5,000 or more because of ADAS systems and electronic components.

Medical costs for injuries have climbed even faster, with emergency response, hospitalization, and ongoing rehabilitation pushing per-claim costs higher every year.

Legal Requirements and DMV Compliance

California’s liability minimums recently increased to $30,000 per person and $60,000 per accident, but this baseline is inadequate for most businesses. A single serious accident involving your vehicle can easily exceed these limits, leaving your company personally liable for thousands or even hundreds of thousands of dollars in damages, legal fees, and settlements. State law requires liability coverage on all business vehicles, and the California DMV electronically verifies this insurance starting in 2023. If your insurer does not report your coverage to the DMV, your vehicle registration will be suspended until you submit proof of insurance.

Protection Beyond the Minimum

Beyond legal compliance, commercial auto insurance protects your assets when accidents happen. Collision and comprehensive coverage safeguard your vehicles against theft, weather damage, and accidents caused by your drivers. Uninsured motorist protection covers your drivers if they are hit by someone without adequate insurance, which is a real concern given that one in five California drivers lacks proper coverage. The cost of not carrying adequate coverage is catastrophic: a single claim exceeding your liability limits can bankrupt a small business. Your coverage must match both legal requirements and the actual risks your business faces on the road, not just the minimum threshold required by law.

Understanding what you need is only the first step. The next section covers the specific coverage types that California businesses should evaluate when shopping for quotes.

Coverage Types California Businesses Actually Need

Liability Coverage: Why State Minimums Fall Short

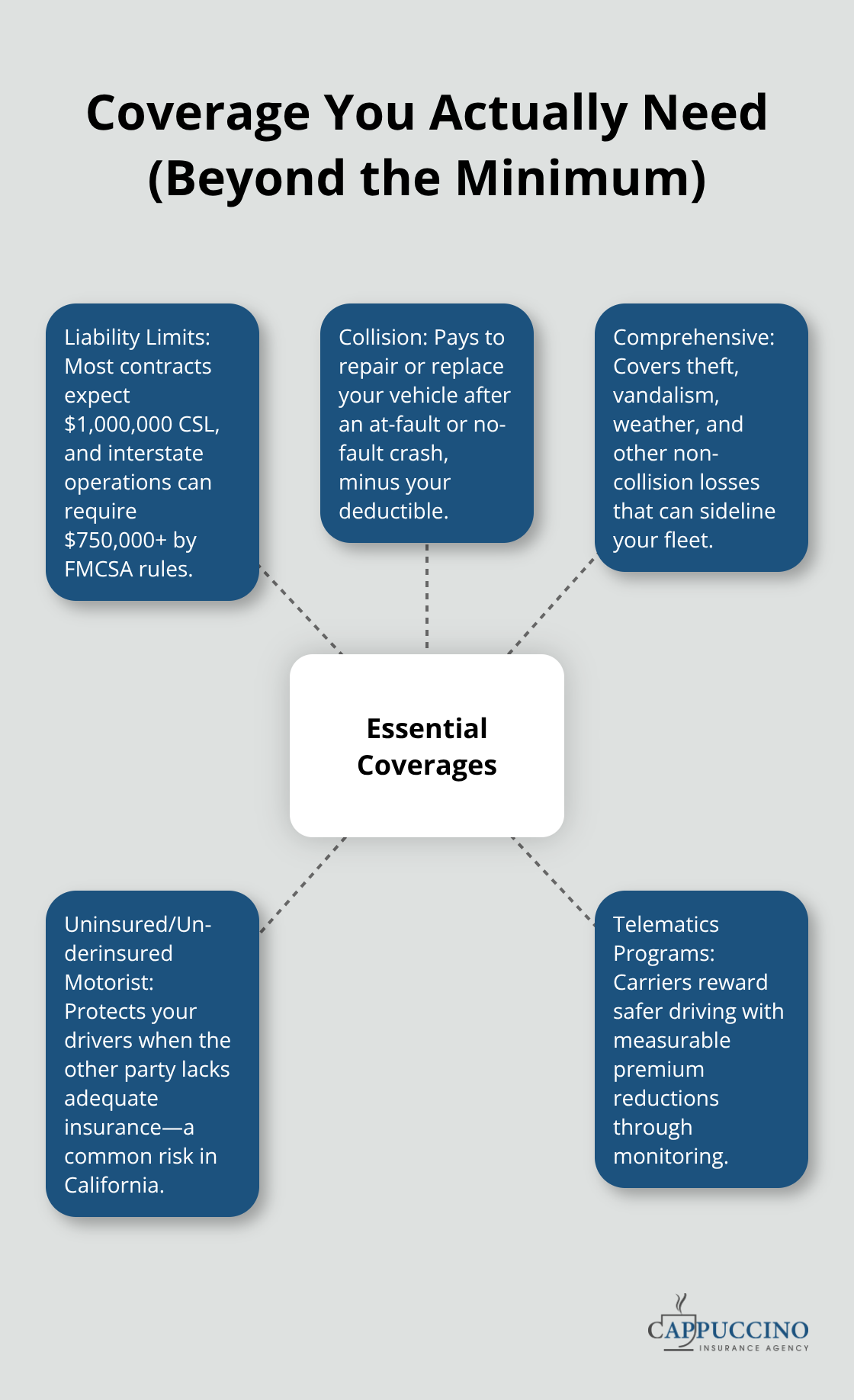

Liability coverage forms the foundation of any commercial auto policy, but California’s $30,000 per person and $60,000 per accident minimums expose your business to serious financial risk. A single serious injury claim easily exceeds these limits-medical costs alone for hospitalization and rehabilitation run $50,000 to $150,000. Most contracts and client agreements require you to carry $1,000,000 in combined single limit liability, which is standard across industries from construction to delivery services. Federal FMCSA rules push that requirement even higher for interstate work, mandating $750,000 or more in combined single limits. The gap between state minimums and real-world exposure is massive, and underinsuring creates personal liability for your company’s assets.

Evaluate your specific business activities and contract requirements before selecting limits-do not default to the minimum.

Physical Damage Protection: Collision and Comprehensive

Collision and comprehensive coverage protect the vehicles themselves, not just third-party liability. Collision covers damage from accidents regardless of fault, while comprehensive handles theft, weather, vandalism, and natural disasters. For financed or leased vehicles, your lender will require both coverages. The cost of vehicles and repair work has climbed sharply due to advanced technology like sensors and cameras that now appear standard on most models; a $1,000 deductible on a modern vehicle means you absorb significant repair costs out of pocket. Light-duty commercial vehicles typically cost $130 to $185 monthly for basic coverage, while cargo vans run $160 to $265 monthly-these benchmarks help you evaluate whether quotes are competitive.

Uninsured Motorist Coverage: Protection Against Underinsured Drivers

Uninsured motorist coverage is non-negotiable in California, where nearly one in five drivers lacks adequate insurance. If your driver gets hit by an uninsured or underinsured motorist, this coverage pays for injuries and vehicle damage up to your selected limits. California law allows you to decline uninsured/underinsured motorist coverage in writing, but doing so exposes your drivers and company to serious financial risk. This protection matters because you cannot control whether other drivers carry sufficient insurance.

Telematics Programs: Lower Premiums Through Safety Monitoring

Telematics programs from carriers like Travelers and Nationwide reduce premiums by 10 to 15 percent by monitoring driver behavior and rewarding safe practices. These programs track acceleration, braking, speeding, and distracted driving patterns, then translate that data into measurable savings. Implementing telematics makes practical sense-you lower costs while improving safety outcomes simultaneously. When you shop for quotes, ask carriers about their specific telematics offerings and discount percentages, since programs vary significantly across insurers.

Getting the right coverage mix protects your business, but finding competitive quotes requires knowing how to compare carriers effectively and identify which options actually fit your budget.

How to Get Competitive Quotes and Save Money

Request Quotes From Multiple Carriers

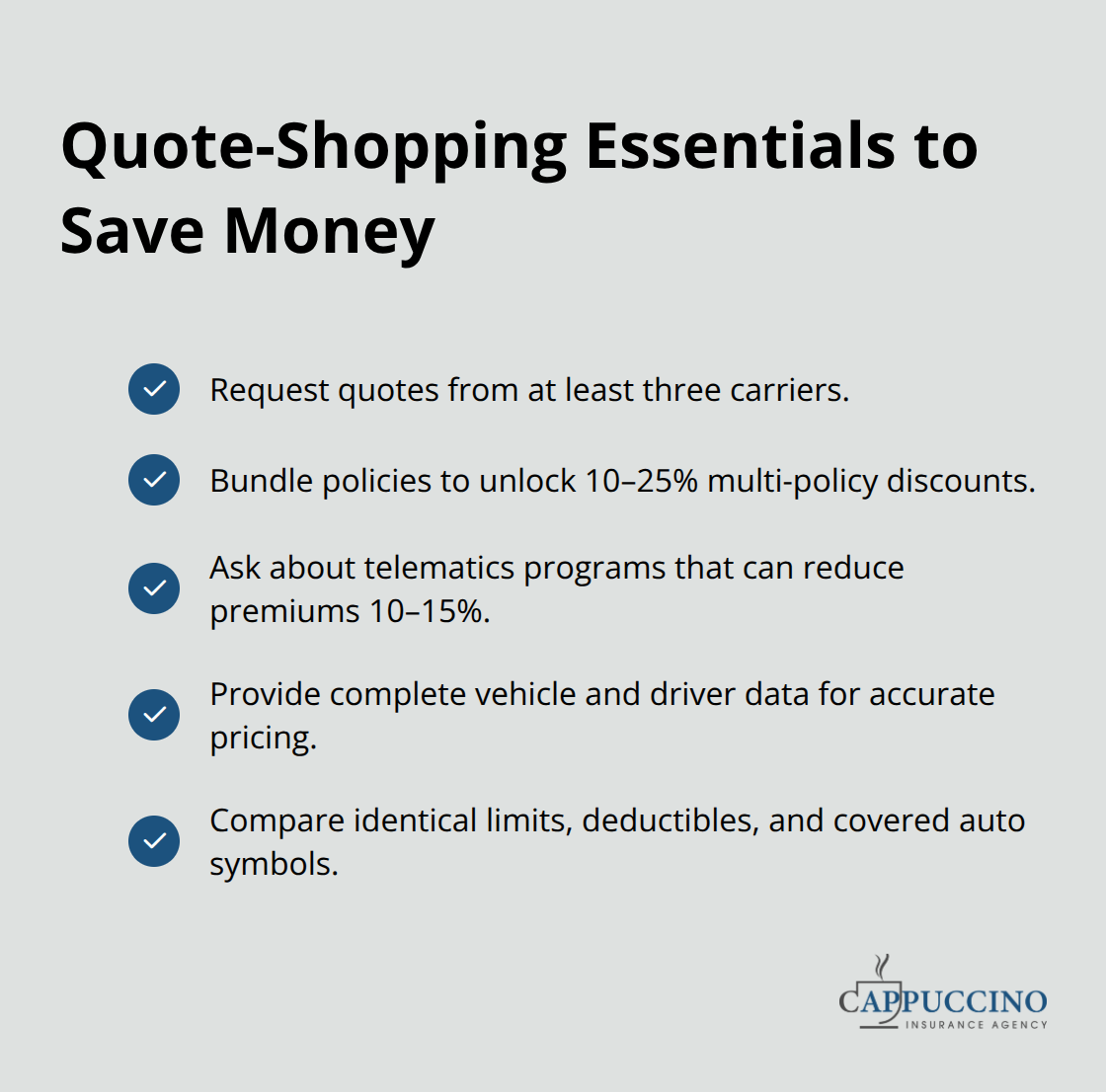

Multiple quotes from different carriers are non-negotiable if you want competitive pricing. Most California businesses accept the first quote they receive, which is a costly mistake-premium differences between carriers for identical coverage regularly exceed 40 percent. When you request quotes, have your vehicle information ready: VINs, gross vehicle weight ratings, years in operation, driver details, and your complete business description.

Carriers price commercial auto coverage based on specific risk factors, and incomplete information forces them to use default assumptions that inflate quotes. Request quotes from at least three carriers before making a decision.

Progressive, ERGO NEXT, and biBERK can generate certificates of insurance within minutes of binding, which matters if you need coverage quickly for a new vehicle or contract requirement. Travelers and Erie Insurance excel at competitive pricing for established fleets with clean loss histories. When comparing quotes, ensure you’re evaluating identical coverage: same liability limits, matching deductibles, and equivalent covered auto symbols. A $500 difference in premium might reflect lower collision deductibles or reduced uninsured motorist limits, not better pricing.

Bundle Policies to Unlock Discounts

Bundling your commercial auto policy with general liability, inland marine, or workers’ compensation coverage typically yields multi-policy discounts of 10 to 25 percent depending on the carrier and your claims history. This approach simplifies your coverage structure and reduces your overall premium burden. Cappuccino Insurance Agency partners with 20+ carriers to deliver bundled solutions and specialty coverage for hard-to-place risks, plus we conduct annual policy reviews to help you capture discounts you might miss otherwise.

Strengthen Your Risk Profile

Implementing a fleet safety program directly influences your renewal rates and future quotes. Carriers favor businesses that demonstrate genuine risk control through written safety policies, annual defensive driving training, and consistent driver monitoring. Telematics programs reduce premiums by 10 to 15 percent-Travelers, Nationwide, and Progressive all offer measurable savings for monitoring driver behavior. Regularly screen drivers and review motor vehicle records annually to catch violations or accidents early.

Maintain detailed records of vehicle maintenance, driver training completion, and safety incidents, then share this information when requesting quotes and during renewal discussions. Prompt claims reporting also matters; delaying notification signals poor risk management to insurers, which affects your renewal pricing. Resources like driver safety templates and training programs strengthen your risk profile when you apply for quotes.

Review Coverage Annually

Review your coverage annually because your business activities, fleet size, and liability exposures change over time. A policy that fit your needs two years ago may leave you underinsured today. California commercial auto premiums are rising due to increased repair costs from advanced vehicle technology, higher medical expenses, and more severe crashes driven by risky driving behaviors. Your annual review should address whether your liability limits still match your contract requirements and whether new vehicles or service lines require additional endorsements.

Final Thoughts

Commercial auto insurance in California protects your business from accidents, liability claims, and financial collapse when serious incidents occur. State minimums of $30,000 per person and $60,000 per accident leave you exposed, and nearly one in five California drivers lacks adequate coverage, which means your policy must exceed legal minimums to match your actual business risks and contract requirements (typically $1,000,000 in combined single limit liability). Collision, comprehensive, and uninsured motorist coverage complete your protection, while telematics programs reduce premiums by 10 to 15 percent through driver monitoring and safety incentives.

Getting competitive quotes requires requesting coverage from multiple carriers with identical limits and deductibles so you can compare actual pricing differences. Implementing a fleet safety program, maintaining vehicles properly, and reviewing coverage annually strengthen your risk profile and improve renewal rates. California premiums continue rising due to advanced vehicle technology, higher medical costs, and more severe crashes, making annual reviews essential to prevent underinsurance.

We at Cappuccino Insurance Agency understand that finding the right commercial auto insurance California coverage at a competitive price takes time and expertise. As an independent agency partnering with 20+ carriers, we deliver local expertise and bundle discounts across California. Contact us to request quotes from multiple carriers and explore specialty solutions tailored to your fleet’s specific needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.