Risk Mitigation for Homeowners: Practical Steps to Protect Your Property

Your home faces real threats every day, from severe weather to break-ins to accidents that could injure someone on your property. These risks don’t just damage your house-they can drain your finances fast.

Risk mitigation for homeowners isn’t complicated, but it does require a clear plan. We at Cappuccino Insurance Agency help homeowners like you understand what threats matter most and how to protect against them with practical steps and the right insurance coverage.

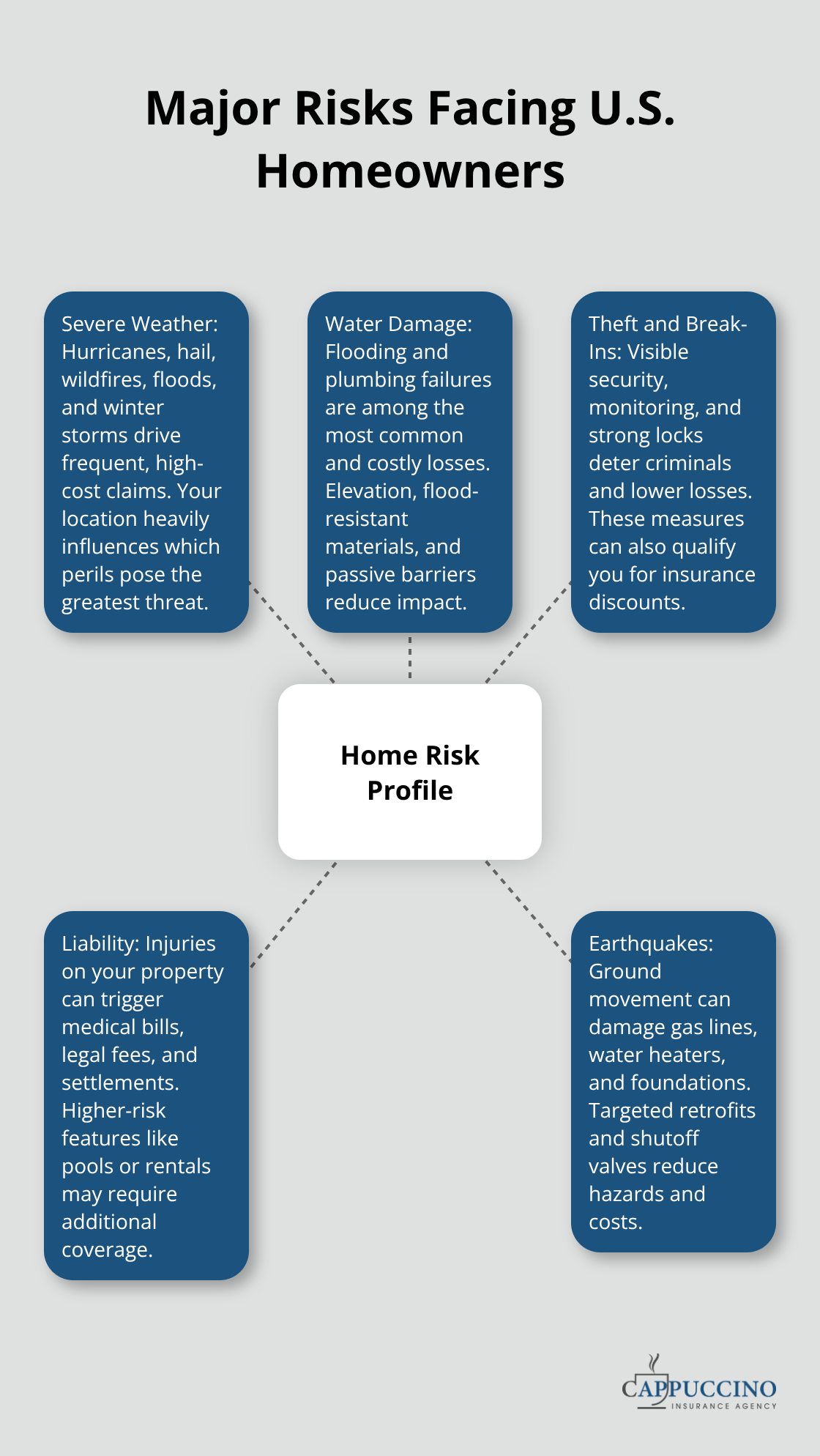

What Threatens Your Home Most

Weather Disasters Strike Hard and Often

Weather disasters cost American homeowners billions annually, and the trend accelerates. In 2024, nearly 30 billion-dollar severe weather events struck the U.S., spanning hurricanes, floods, wildfires, hail, and winter storms. Your location determines which threats matter most-Florida homeowners face hurricane risk with premiums averaging four times the national average, while California properties contend with wildfire exposure. Roof damage from wind or hail represents one of the fastest claims filed against homeowners policies, yet many homeowners skip annual roof inspections by licensed roofers that could catch deterioration before storms hit.

Water damage from flooding or plumbing failures ranks as the second-most common homeowners claim. If your property sits in a flood zone, elevation alone isn’t always necessary; elevating electrical appliances, using flood-resistant materials like tile instead of carpet, and installing passive floodproofing measures around doors and windows provide meaningful protection at lower cost. The National Institute of Building Sciences reports that every dollar invested in mitigation saves six dollars in future disaster costs, making these steps financially smart, not just protective.

Theft and Break-Ins Threaten Your Valuables

Theft and break-ins remain persistent threats regardless of location, costing homeowners thousands in stolen goods and repair expenses. Security systems with professional monitoring, surveillance cameras, and smart locks demonstrably reduce theft risk and often qualify you for insurance discounts. Outdoor lighting, secure landscaping with clear sightlines, and reinforced door locks deter burglars more effectively than assumptions about neighborhood safety.

Liability Claims Can Exceed Your Coverage

Liability claims from injuries on your property-a guest slipping on ice, a contractor injured while working, a neighbor’s child hurt on your deck-can result in medical bills, legal fees, and settlements that exceed standard homeowners coverage limits. Most standard homeowners policies cover basic liability, but high-risk factors like a pool, trampoline, or rental use of your property require additional umbrella or specialty coverage to protect your assets.

Assess Your Risks Before Disaster Strikes

The key is conducting a thorough property risk assessment now, before a disaster or accident forces reactive, expensive decisions later. Understanding which threats apply to your specific property and location allows you to prioritize mitigation steps that matter most. Once you identify your risks, practical steps to reduce them become clear-and that’s where essential mitigation strategies come into play.

How to Strengthen Your Home Against Real Threats

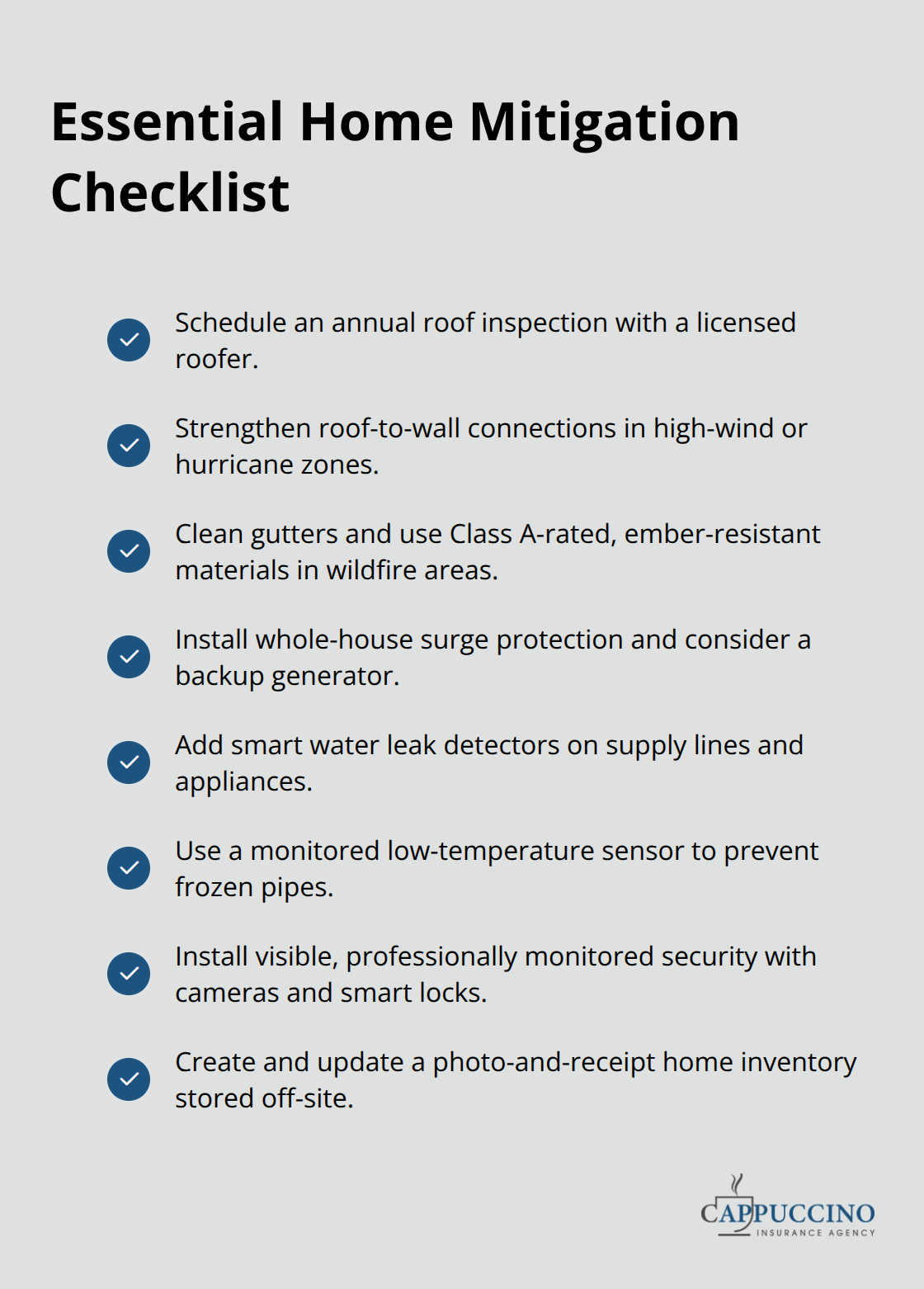

Knowing your risks means nothing without action. Mitigation requires three concrete steps: keeping your home’s critical systems in working order, installing devices that detect and deter problems before they escalate, and maintaining an accurate record of what you own. These aren’t optional upgrades-they’re standard practices that lower your insurance costs and prevent catastrophic losses.

Protect Your Roof and Weather-Vulnerable Systems

Your roof triggers the fastest and most expensive claims, so start your mitigation there. A licensed roofer should inspect your roof annually, checking for missing shingles, deteriorated flashing, and structural weakness before storms arrive. If you live in a hurricane or high-wind zone, verify that your roof-to-wall connections use robust attachment patterns-8d nails at 6-inch spacing with engineering input provides the performance that matters when wind pressure tests your home.

For wildfire risk, start your assessment at the roof and work downward: install Class A-rated siding, use ember-resistant vents, rake gutters clean, and keep decks free of debris and flammable materials. In flood zones, a Secondary Water Resistance barrier on your roof can improve performance and may reduce your insurance premiums.

Upgrade Your Electrical and Plumbing Systems

Your electrical system and plumbing deserve equal attention to your roof. Have an electrician inspect for arcing behind walls and install whole-house surge protection plus a backup generator if you live where power outages follow storms. For plumbing, water leak detection systems catch failures before they destroy walls and flooring-these smart devices provide real-time alerts and significantly reduce water damage losses, which rank as the second-most common homeowners claim.

Your heating system needs a monitored low-temperature sensor that alerts you if your furnace fails during winter; this single device prevents frozen pipes that cost thousands to repair.

Install Visible Security and Monitoring Devices

Security devices work best when they’re visible and professionally monitored. Install surveillance cameras at entry points, use smart locks on exterior doors, and add motion-sensor lighting around your property perimeter-burglars avoid homes where they’ll be seen and recorded. A professionally monitored security system with 24/7 response qualifies you for insurance discounts that often pay back the installation cost within two years.

Prepare for Earthquake and Water Threats

For earthquake risk, install a seismic gas shutoff valve, strap your hot water heater to wall studs, and retrofit foundation bolts if your home was built before modern building codes. These steps stabilize your home’s most vulnerable components when ground movement strikes.

Document Everything You Own

Your final critical step is maintaining a current home inventory with photos and receipts stored off-site in cloud storage or a safe deposit box. This inventory simplifies insurance claims after a loss and proves what you owned, what condition items were in, and what they cost to replace. Document high-value items like jewelry, art, and electronics separately, because standard homeowners policies cap coverage on these categories.

Once you’ve completed these mitigation steps, your home stands far stronger against the threats that matter most in your area. The next piece of this protection puzzle is selecting the right insurance coverage-because even the best-maintained home needs financial backup when disaster strikes.

Insurance Coverage That Protects Against Major Risks

Standard Homeowners Policies Leave Critical Gaps

Standard homeowners insurance protects against specific perils, but most policies exclude water damage from flooding and earthquakes entirely, leaving homeowners dangerously underprotected in high-risk zones. Your base policy covers wind, hail, theft, and liability from injuries on your property, but replacement cost inflation has outpaced coverage limits significantly. A building insured for three million dollars may now require more than four million for actual reconstruction due to material costs, labor expenses, and supply chain disruptions. This undervaluation trap catches homeowners off guard when they file claims and discover their coverage falls short.

Conduct a professional property valuation review now to determine true replacement costs, not outdated estimates from years past. Work with your insurance advisor to adjust your coverage limits upward and document the valuation methodology used, so you have proof that your coverage reflects current market rates.

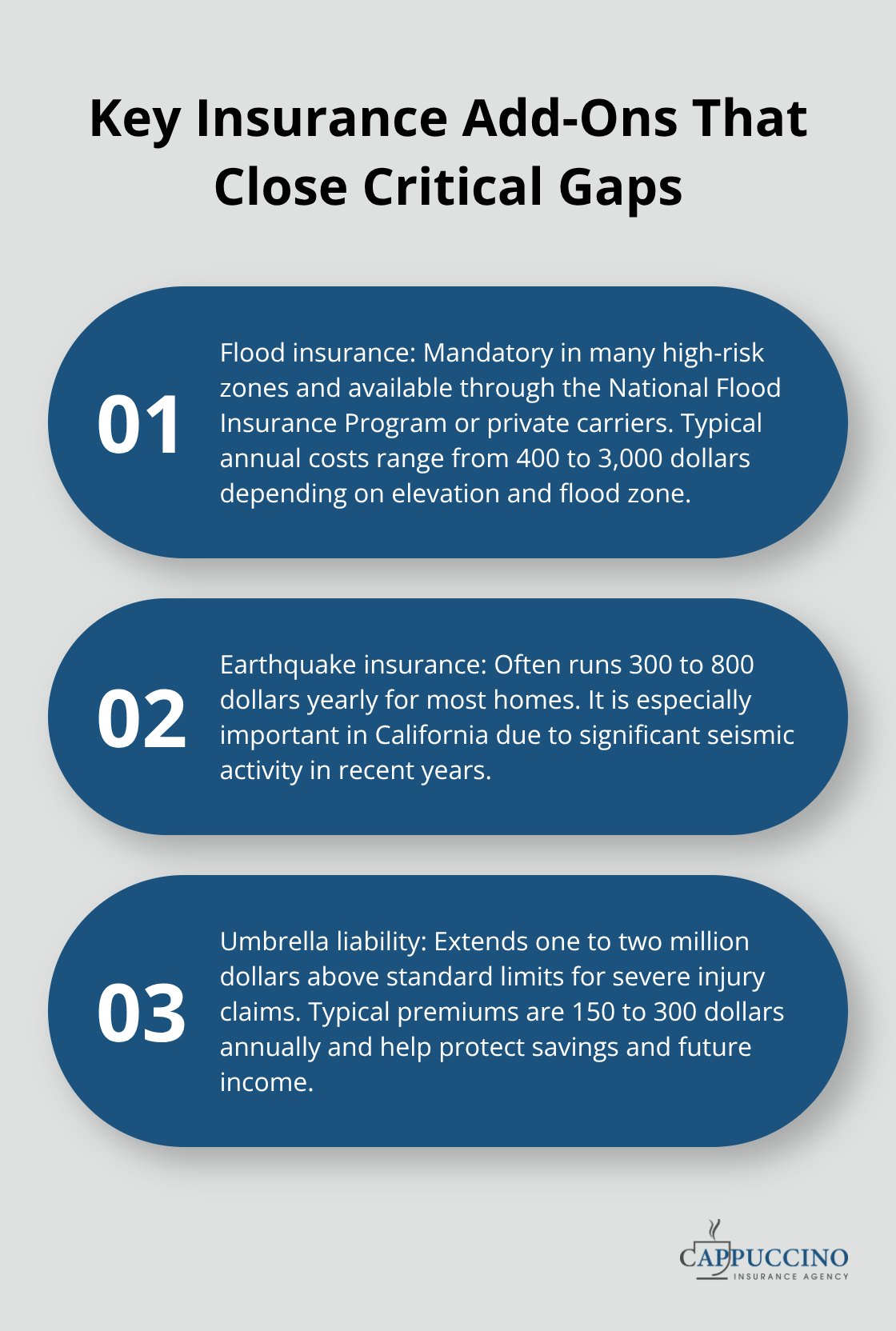

Flood and Earthquake Coverage Fills Essential Voids

Additional coverage options separate homeowners who stay protected from those who face financial ruin after disaster strikes. Flood insurance through the National Flood Insurance Program or private carriers is mandatory in high-risk zones and costs between 400 and 3,000 dollars annually depending on your property’s elevation and flood zone designation. Earthquake coverage runs 300 to 800 dollars yearly for most homes but becomes non-negotiable if you live in California, which experienced significant seismic activity in recent years.

Umbrella Policies Protect Your Assets

Umbrella policies extending one to two million dollars above your standard liability limits cost 150 to 300 dollars annually and protect your assets when someone is seriously injured on your property. These policies activate when liability claims exceed your homeowners policy limits, shielding your savings and future income from catastrophic judgments.

Specialty Coverage for High-Risk Properties

Specialty coverages for wildfire risk, including California FAIR Plan policies and Difference-in-Conditions wraps, address gaps that standard carriers increasingly refuse to fill in high-exposure areas. We at Cappuccino Insurance Agency partner with over 20 carriers across California to help homeowners secure specialty solutions for properties traditional insurers reject, including wildfire-prone regions where standard coverage has become scarce.

Annual Policy Reviews Close Coverage Gaps

Annual policy reviews matter more than most homeowners realize because your risk profile changes when you renovate, add a pool, rent out your home, or experience significant weather events in your area. Schedule a coverage assessment each year to close gaps, adjust limits for inflation, and capture discounts you may have missed, so your financial protection actually matches your real exposure.

Final Thoughts

Risk mitigation for homeowners works best when you combine practical property improvements with solid insurance coverage. The steps you’ve learned-inspecting your roof annually, installing security systems, upgrading electrical and plumbing protections, and maintaining a home inventory-directly reduce your exposure to the threats that matter most in your area. These actions lower your insurance costs, prevent catastrophic losses, and give you genuine peace of mind that your home can withstand the disasters and accidents that strike thousands of homeowners every year. Insurance alone cannot protect you, because a policy pays claims after damage occurs, but mitigation prevents damage from happening in the first place.

When you combine both strategies, you create a complete defense: mitigation reduces the frequency and severity of losses, while insurance covers what mitigation cannot prevent. This partnership is why homeowners who invest in both see lower premiums, faster claim settlements, and faster recovery after disasters. Your home’s true replacement cost likely exceeds your current coverage limits due to inflation and supply chain disruptions, so a professional valuation review identifies gaps that leave you exposed.

Schedule a coverage assessment today to ensure your insurance limits match your home’s actual replacement cost and your specific risk profile. Cappuccino Insurance Agency helps homeowners across California secure coverage solutions tailored to your property’s unique threats, including specialty options for wildfire-prone areas. Contact us to strengthen your home’s protection with the right combination of mitigation and insurance.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.