California Auto Insurance Rates: How to Compare and Save

California auto insurance rates are among the highest in the nation, and most drivers overpay without realizing it. We at Cappuccino Insurance Agency help thousands of Californians find better coverage at lower costs every year.

This guide shows you exactly how to compare quotes, understand what you’re paying for, and cut your premiums without sacrificing protection.

Why California’s Insurance Costs Stand Out

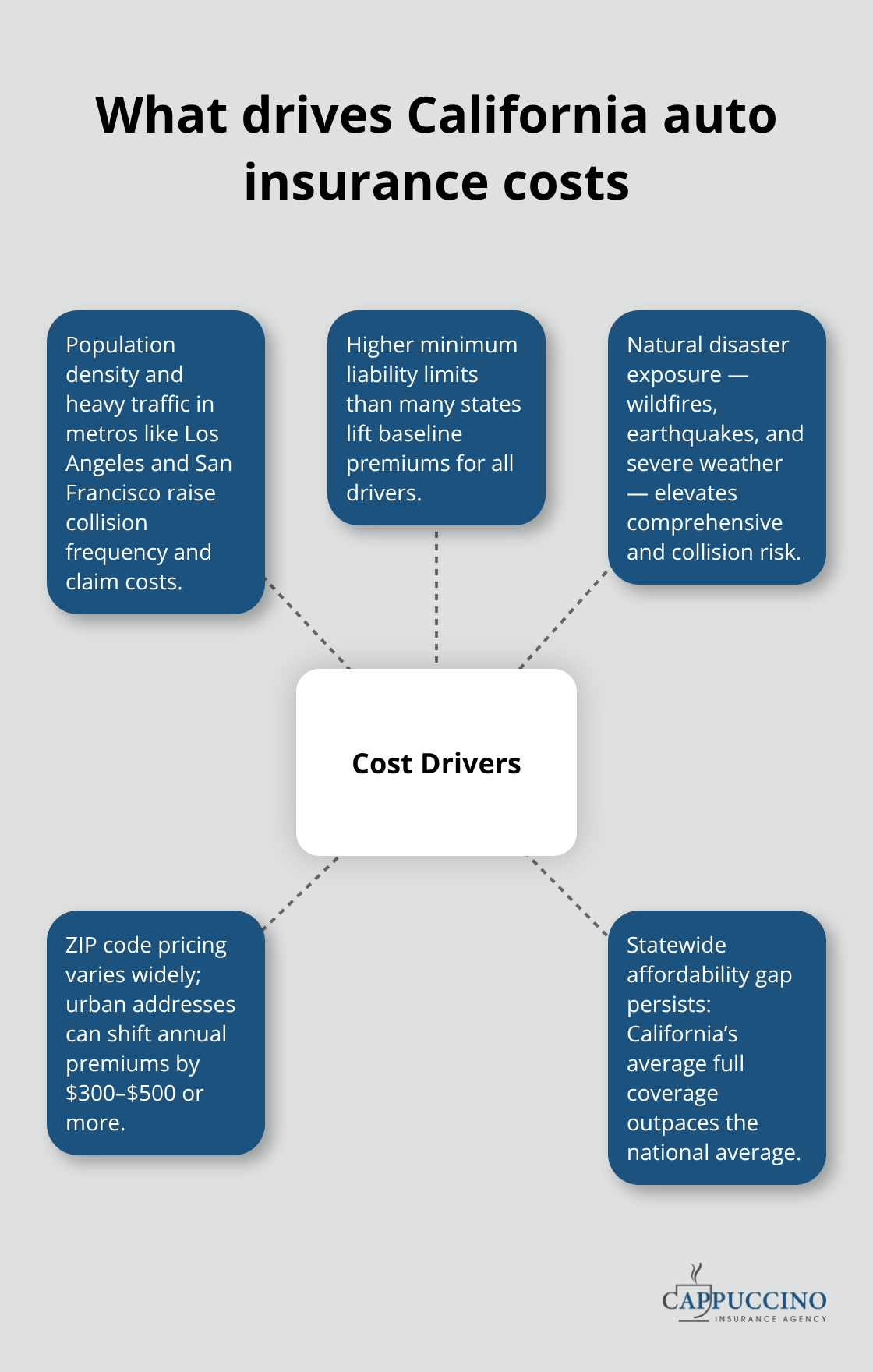

California’s 2025 average full-coverage auto insurance cost reached $2,309 annually, with projections of $2,333 for 2026 according to Insurify data. The national average dropped to $2,144, creating a significant affordability gap for California drivers. The state’s position reflects three concrete factors that directly impact what you pay each month. Population density in major metros like Los Angeles, San Francisco, and San Diego drives collision frequency and claim costs substantially higher than rural areas. California also mandates higher minimum liability coverage limits than many states, which automatically raises baseline premiums.

Additionally, the state’s exposure to wildfires, earthquakes, and severe weather increases the overall risk profile that insurers factor into their rates. These drivers explain why shopping aggressively for quotes delivers outsized savings in California compared to other states.

Traffic and Urban Congestion Push Costs Higher

California’s congested roadways directly translate to higher accident rates and more expensive claims. The California Department of Insurance publishes 2026 online sample rate comparisons showing how premiums vary across insurers, and these surveys reveal that location within the state significantly affects your quote. A driver in a dense urban ZIP code pays substantially more than someone in a less congested area, even with identical driving records and vehicles. This is why comparing quotes by your specific ZIP code matters-rates can swing hundreds of dollars between neighborhoods. Major carriers factor in local traffic patterns, theft rates, and accident frequency when pricing, so your address alone can shift your annual premium by $300 to $500 or more.

Mandatory Coverage Levels and Natural Disaster Risk

California requires higher liability minimums than many states, which forms the foundation of your premium. The state’s wildfire seasons, earthquake risk, and coastal storm exposure also influence comprehensive and collision pricing. Insurers build these regional risks into their rate structures, meaning California drivers start from a higher baseline than drivers in states with less exposure. This reality makes deductible selection and coverage evaluation even more important-raising your deductible from $500 to $1,000 can cut your premium significantly without eliminating protection.

Why Comparison Shopping Matters in California

The combination of high baseline rates and location-specific pricing creates enormous variation between insurers. Two carriers can quote the same driver hundreds of dollars apart for identical coverage, which means your next step involves gathering multiple quotes to see where real savings hide. The California Department of Insurance rate surveys show these differences exist across the market, and your specific situation (vehicle type, driving history, ZIP code) determines which insurers offer the best value for you.

How to Compare Quotes and Find Real Savings

Request Quotes from Multiple Carriers

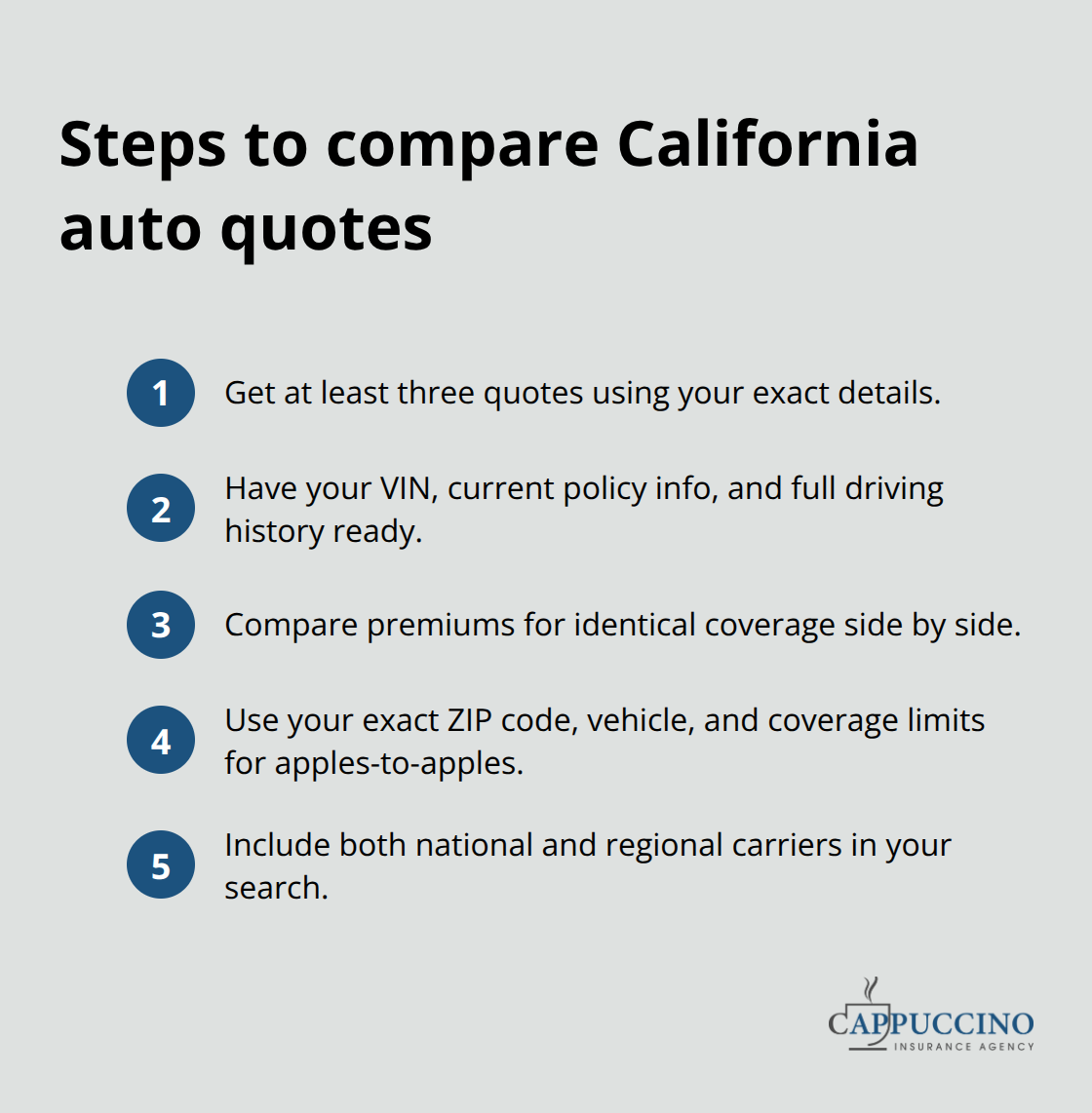

Start by requesting quotes from at least three different insurers using your specific information-this step alone typically reveals $300 to $500 in annual variation for identical coverage. When you contact carriers or use online tools, have your vehicle identification number, current policy details if you have one, and complete driving history ready so quotes reflect your actual risk profile. Premiums for the same driver vary widely across carriers, which means skipping this comparison step costs most California drivers hundreds annually.

The California Department of Insurance publishes 2026 online sample rate comparisons that show how different insurers price coverage, serving as a helpful reference point before you request formal quotes. Request quotes from major carriers like GEICO, Progressive, and State Farm, but also ask regional insurers about their California rates since local expertise sometimes delivers better pricing. Once you gather three to five quotes, compare them side by side using your actual ZIP code, vehicle type, and coverage limits to see which carriers offer the best value for your situation.

Examine Coverage Details and Deductible Options

Don’t automatically select the lowest quote-examine what coverage each one includes and verify that liability limits meet California’s mandatory minimums. Understanding your quote breakdown matters because insurers calculate premiums differently based on how they weight factors like location, driving record, vehicle type, and claims history. Raising your deductible from $500 to $1,000 typically lowers your monthly premium without eliminating protection, though verify you can afford that deductible if a claim occurs.

For older vehicles, consider whether comprehensive and collision coverage still makes financial sense compared to the premium cost. California drivers should focus on driving history, location, vehicle type, and eligible discounts rather than credit scores since California prohibits using credit-based scores in auto pricing decisions.

Leverage Online Comparison Tools and Telematics Programs

Online comparison tools accelerate this process significantly. Insurify connects you with 120+ insurers and provides real-time quotes, while Compare.com partners with similar numbers of carriers and reports that customers save up to $867 annually when shopping through their platform. These tools let you enter information once and view multiple quotes instantly rather than calling each carrier individually, saving hours of effort.

Usage-based insurance programs like MercuryGO monitor your actual driving behavior and can reduce premiums by up to 30% if you qualify, so ask carriers whether they offer telematics discounts when requesting quotes. The best time to shop is annually or when major life changes occur-moving within California, adding a new driver, or purchasing a different vehicle all affect your rate significantly. These changes create opportunities to reassess your coverage and find carriers that better match your current situation.

Cut Your Premium Without Cutting Protection

Bundle Auto and Home Policies for Immediate Savings

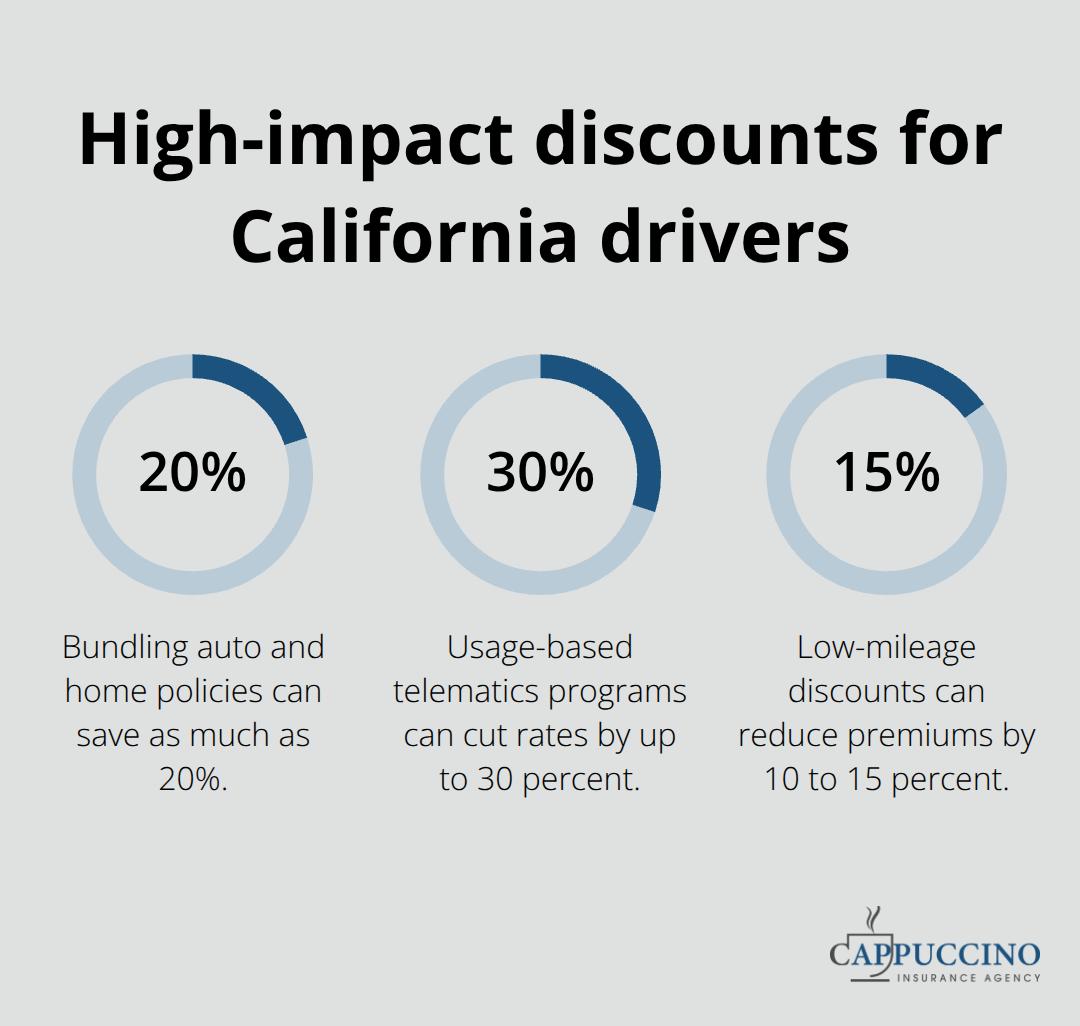

Combining your auto and home policies stands as the single most effective way to lower your California premium immediately. State Farm, Allstate, and Nationwide all offer substantial multi-policy discounts from bundling auto and home insurance that can save you as much as 20% when you combine coverage. Contact your current insurer or shop new carriers specifically asking about bundle discounts-this single step often outperforms every other savings strategy combined. If you own multiple vehicles, stacking them on the same policy multiplies your savings further through multi-car discounts that many insurers apply automatically.

Maintain a Clean Driving Record

Your driving record directly determines whether you qualify for good driver discounts that persist year after year, making this the longest-lasting savings lever available. A clean record without accidents or violations can sustain discounts indefinitely, while even one incident can eliminate eligibility for three to five years depending on the carrier. Safe driving directly lowers premiums; fewer claims over time help you keep costs down and can qualify you for additional discounts that compound your savings.

Adjust Your Deductible and Coverage Levels

Raising your deductible from $500 to $1,000 typically cuts your monthly premium by 15 to 30 percent without eliminating protection if you maintain an emergency fund to cover that amount. For vehicles worth less than $10,000, comprehensive and collision coverage may cost more annually than the car’s replacement value-calculate whether dropping these coverages makes sense for older vehicles since you only need liability coverage to meet California legal requirements. This evaluation prevents you from overpaying for protection you don’t need while maintaining the coverage that matters most.

Leverage Safety Features and Usage-Based Programs

Cars equipped with automatic emergency braking, lane departure warnings, and anti-lock brakes qualify for lower premiums due to reduced accident severity. Usage-based programs like MercuryGO monitor your actual driving behavior and can cut rates by up to 30 percent by tracking speed, braking patterns, and mileage. Ask carriers whether they offer telematics discounts when requesting quotes, since these programs reward safe driving with meaningful rate reductions.

Qualify for Low-Mileage Discounts

Low-mileage discounts apply if you drive fewer than 10,000 to 12,000 miles annually, so document your mileage when requesting quotes since this factor alone can reduce your premium by 10 to 15 percent. This discount reflects reduced collision risk and makes sense for California drivers who work from home, use public transit, or live in walkable neighborhoods where driving stays minimal.

Final Thoughts

Comparing California auto insurance rates requires you to request quotes from multiple carriers, examine coverage details carefully, and shop actively rather than renew automatically each year. The strategies in this guide-bundling policies, maintaining a clean driving record, adjusting deductibles, and qualifying for usage-based discounts-work together to compound your savings substantially. Most California drivers leave hundreds of dollars on the table annually simply because they never contact competing carriers or ask about available discounts.

Your next step is straightforward: request quotes from at least three insurers this week using your specific ZIP code, vehicle information, and driving history. Compare the quotes side by side, paying attention to coverage details and deductible options rather than focusing solely on the lowest price. Once you identify the best option, contact that carrier to confirm any discounts you qualify for and ask about bundling opportunities if you carry home or renters insurance.

Long-term savings come from reviewing your policy annually and shopping for new quotes every one to two years, since California auto insurance rates shift constantly and new discounts emerge regularly. Major life changes like moving within California, adding a new driver, or purchasing a different vehicle create immediate opportunities to reassess your coverage and find carriers that better match your situation. Contact us at Cappuccino Insurance Agency to get started with a comprehensive rate comparison today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.