California Commercial Auto Quotes: Fast, Local Options

Running a business fleet in California means navigating strict insurance requirements and rising accident costs. Getting California commercial auto quotes shouldn’t be complicated, yet many business owners waste time comparing options or end up underinsured.

We at Cappuccino Insurance Agency help California businesses find coverage that actually fits their needs. This guide walks you through getting fast quotes, avoiding costly mistakes, and understanding what protection your fleet really requires.

Why Commercial Auto Insurance Isn’t Optional in California

California requires any business operating vehicles for work to carry commercial auto insurance, and this isn’t a suggestion. A personal auto policy simply won’t cover work-related driving, whether that’s deliveries, client visits, or moving equipment. The California Department of Insurance is clear: without proper commercial coverage, your business faces serious consequences. Penalties start at $350 and escalate to $1,800 for repeat violations, plus vehicle impoundment and license suspension up to four years. Beyond legal trouble, one accident without coverage could bankrupt your operation. Medical bills, property damage claims, and lost wages from a single incident can easily exceed $100,000. California law sets minimum liability limits at $30,000 per person and $60,000 per incident for bodily injury, plus $15,000 for property damage, but these minimums barely scratch the surface of real-world claim costs. The average cost of California commercial auto insurance runs about $154 per month according to Insureon’s data, a small price compared to the financial devastation of an uninsured accident.

Fleet Accidents Cost Far More Than You Think

Claim severity in commercial auto has climbed sharply due to advanced vehicle repair costs and rising medical expenses after accidents. A single serious injury claim can easily exceed your minimum liability limits, leaving your business personally liable for the difference. Higher liability limits-such as $500,000 or $1,000,000 combined single limits instead of the bare minimum-protect both current assets and future earnings. Driver shortages and inexperience have pushed claim frequency higher across the industry, meaning more accidents occur than before. Distracted driving remains the leading cause of accidents, and that risk sits directly in your fleet’s hands. Proactive fleet safety programs, regular driver training, and telematics monitoring reduce both accident frequency and severity, which translates into better quotes over time. Carriers now actively reward businesses that demonstrate strong risk management practices with lower premiums and broader coverage options.

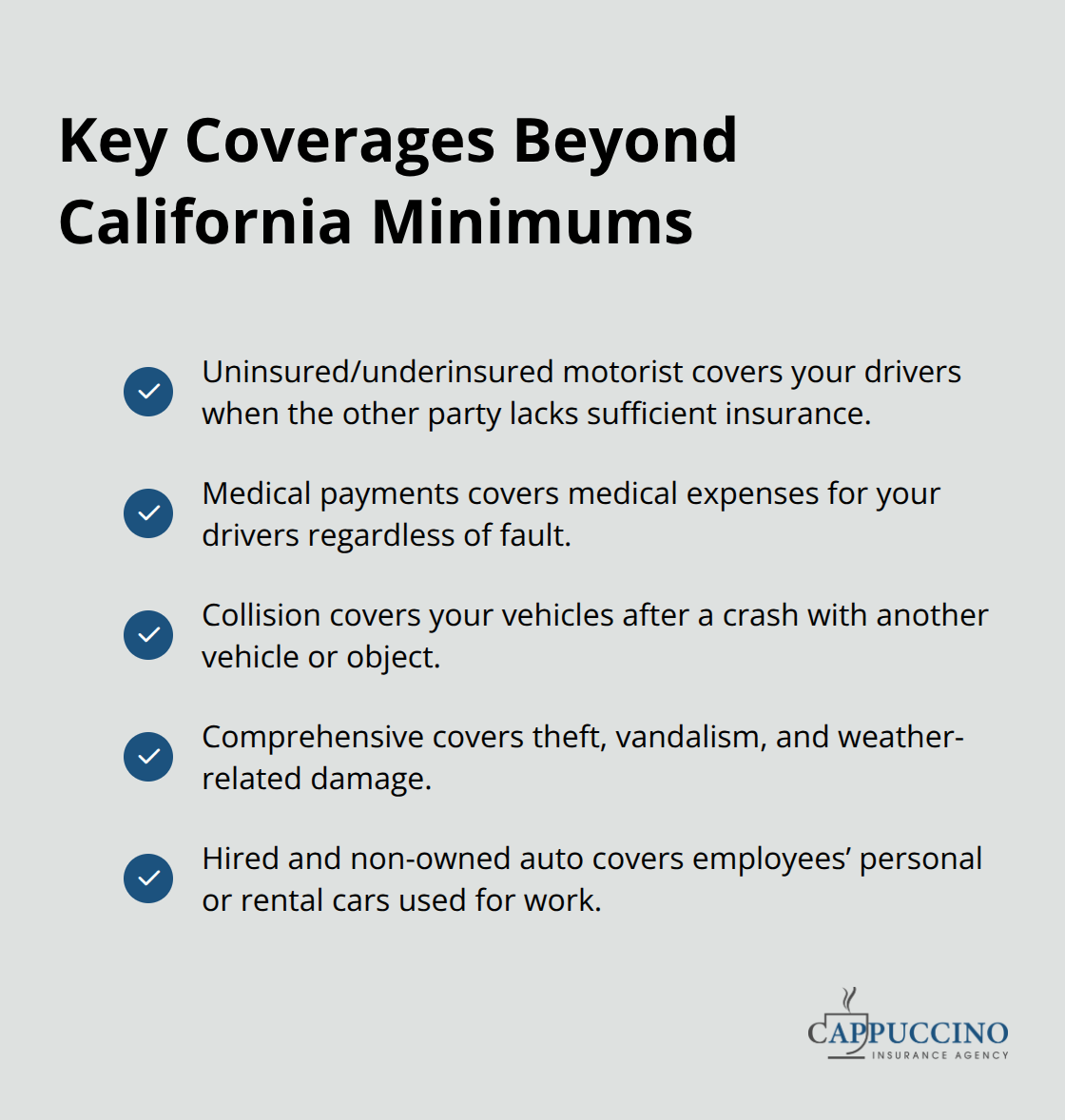

Coverage That Protects Beyond Legal Minimums

Uninsured and underinsured motorist coverage protects your drivers when the other party lacks sufficient insurance, a real concern on California roads. Medical payments coverage handles medical expenses for your drivers regardless of fault, keeping them healthy and your business operational. Collision and comprehensive coverage protect your vehicles from accidents, theft, and weather damage. Hired and non-owned auto coverage is essential if your team uses personal vehicles or rental cars for work-a gap that catches many businesses off guard. The right combination of coverages depends entirely on how your business operates and what vehicles your team drives.

Understanding these options before you request quotes helps you compare apples to apples across carriers and avoid paying for protection you don’t need while missing coverage you do.

Getting Fast Quotes From California Carriers That Actually Compete

Work With Licensed Agents Who Access Multiple Carriers

The fastest way to get California commercial auto quotes is to work with an independent agent who accesses multiple carriers simultaneously rather than calling insurers one by one. California Department of Insurance guidance emphasizes that licensed broker-agents specializing in commercial coverages pull quotes from multiple carriers at once, saving you weeks of phone calls. You can verify an agent’s license status with the California Department of Insurance before proceeding.

Professional associations like the Insurance Brokers and Agents of the West connect you with qualified local brokers who know California’s specific requirements. When you meet with an agent, come prepared to discuss your vehicle count, vehicle types, how you use them, and your driving history. The agent will review your current policy if you have one and identify coverage gaps that new quotes should address.

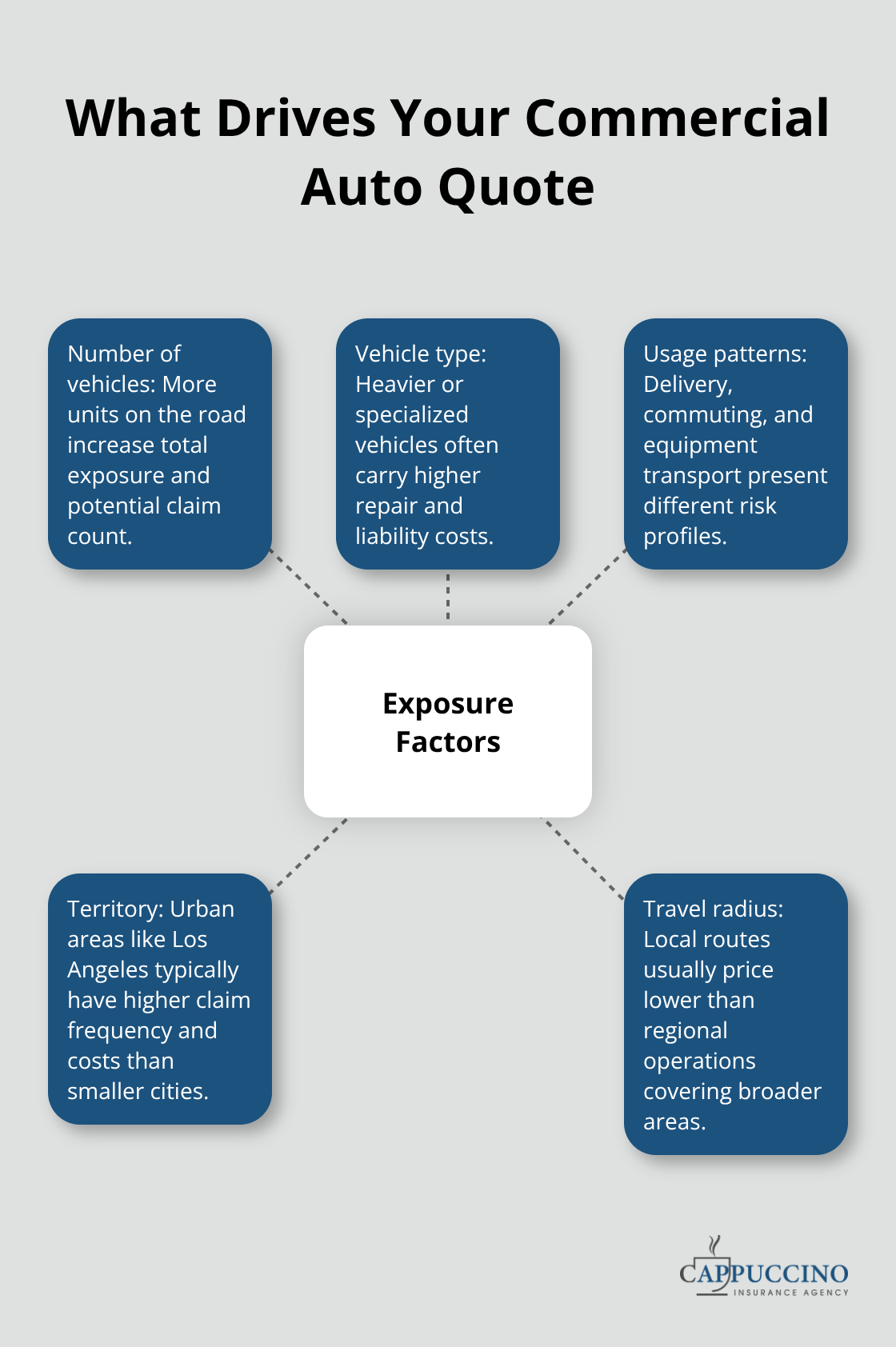

Understand How Exposure Factors Shape Your Quote

Auto quotes price using exposure factors that include number of vehicles, vehicle type, usage patterns, and territory. A food truck operating in Los Angeles will quote differently than the same truck in Bakersfield due to claim frequency and costs in each area. Agents who understand your specific territory and industry often negotiate better terms than generic online platforms can offer.

Territory matters significantly because insurers track claim history and accident rates by location. Los Angeles typically carries higher premiums than smaller cities like Bakersfield for identical vehicles and coverage. Your travel radius also affects pricing-local city routes present lower risk than regional routes covering broader areas.

Match Coverage Exactly When Comparing Quotes

Comparing quotes accurately requires matching coverage exactly across proposals, not just looking at the lowest premium number. Ensure each quote uses the same liability limits (California minimum is 30/60/15, but most businesses need higher limits like $500,000 or $1,000,000 combined single limits), the same deductible levels, and the same coverage symbols for each vehicle. A $1,000,000 limit quote will always cost more than a $500,000 limit, so premium differences only matter when protection matches.

Digital-first carriers like ERGO NEXT and biBERK issue certificates of insurance in minutes online, which matters enormously if you need same-day COI proof for job sites.

Leverage Bundle Discounts and Local Expertise

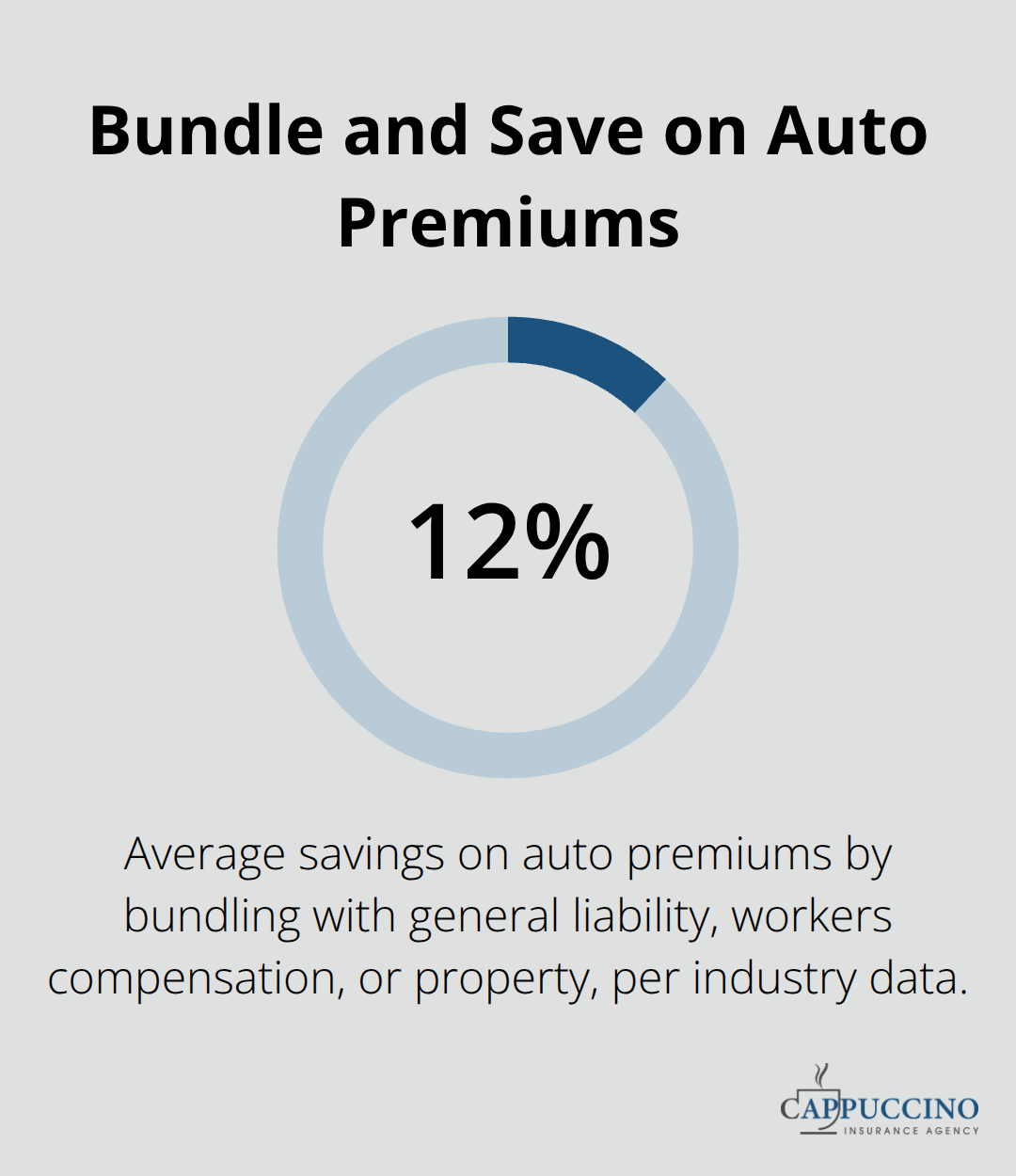

Bundling commercial auto with general liability, workers compensation, or property insurance typically yields around 12% average savings on auto premiums according to industry data. This combination simplifies billing, reduces administrative overhead, and often qualifies you for additional discounts that single-policy carriers cannot match.

Local independent agencies like Cappuccino Insurance Agency partner with 20+ carriers to help you find the exact combination of coverage and price that fits your operation. Working with a local partner means someone understands California’s unique regulatory landscape and can navigate territory-specific pricing without the delays of national call centers. The next step involves understanding which coverage options actually protect your specific business model and which ones you can safely skip.

Common Mistakes When Shopping for Commercial Auto Insurance

Most California business owners make three critical errors when shopping for commercial auto insurance, and each one drains money from your operation. The first mistake is purchasing minimum liability limits and treating that as sufficient protection. California’s legal minimum of 30/60/15 covers almost nothing in a serious accident, yet many owners stop there because it’s the cheapest option. One claim that exceeds your limit leaves your business personally liable for the difference, which can total hundreds of thousands of dollars. A $1,000,000 combined single limit costs more upfront but protects your actual assets when real accidents happen.

Underinsuring Your Fleet Leaves You Exposed

The gap between minimum coverage and adequate protection is where most businesses fail. You might think the extra premium for higher limits isn’t worth it, but that assumption costs you money in the long run. Request quotes with higher liability limits like $500,000 or $1,000,000 combined single limits and compare them against minimum coverage to see the actual dollar difference. That difference is often smaller than you expect, especially when you add bundled coverages into the equation. A serious injury claim can easily exceed your minimum liability limits, leaving your business personally liable for the remainder. Advanced vehicle repair costs and rising medical expenses after accidents have pushed claim severity sharply higher across the industry. One accident without adequate coverage could bankrupt your operation faster than any other business risk.

Ignoring Bundle Discounts Across Your Policies

The second mistake is treating each insurance policy as a separate purchase instead of combining them strategically. Most business owners carry general liability, workers compensation, and property insurance separately, paying full price for each one. Bundling commercial auto with these policies yields around 12% average savings on auto premiums according to industry data, plus it simplifies billing and reduces administrative headaches. That 12% savings compounds year after year, and the administrative simplification frees your time for actual business operations. Digital carriers like ERGO NEXT and biBERK make it easy to request quotes online with customized limits, but local agents who understand your specific industry and territory often negotiate better terms than automated systems can offer.

Failing to Review Your Policy Annually

The third mistake is treating your policy as a set-it-and-forget-it purchase instead of reviewing it annually. Your business changes, your vehicle mix evolves, your claims history shifts, and your coverage needs expand or contract accordingly. A policy that made sense three years ago may be costing you thousands in unnecessary premiums or leaving dangerous gaps today. Schedule a policy review every 12 months with your agent to catch coverage gaps, eliminate redundant protection, and capitalize on discounts you may have missed. Many California businesses discover during their first annual review that they were either drastically overinsured on certain coverages or dangerously underinsured on others.

Choosing the Right Carrier and Coverage Match

The carriers you work with matter less than ensuring your coverage actually matches your risk, your limits protect your assets, and your premiums reflect every discount you qualify for. Local independent agencies partner with multiple carriers to help you find the exact combination of coverage and price that fits your operation. Working with a local partner means someone understands California’s unique regulatory landscape and can navigate territory-specific pricing without the delays of national call centers. Your business insurance should evolve with your operation, not stagnate in place while your actual risks change.

Final Thoughts

Getting California commercial auto quotes fast requires you to work with someone who accesses multiple carriers, match your coverage to your actual risk, and review your protection annually. The cheapest quote fails you if it leaves your business exposed to liability that exceeds your limits, so request quotes with liability limits that actually protect your assets rather than just California’s legal minimum. Territory, vehicle type, driving history, and claims experience all shape your premium, which means generic online quotes often miss the specific factors that affect your California business.

Gather information about your vehicle count, vehicle types, how your team uses them, and your driving history, then contact an independent agent who accesses multiple carriers simultaneously. Ask about bundle discounts across your policies and whether your current coverage has gaps you haven’t noticed. Digital carriers can issue certificates of insurance in minutes if you need same-day proof, while local agents often negotiate better terms for your specific territory and industry.

Contact Cappuccino Insurance Agency to start your California commercial auto quotes process today. We partner with multiple carriers to help you find coverage that fits your operation and budget, and we provide free coverage assessments to catch gaps and eliminate unnecessary premiums.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.