Independent Insurance Agent California: Local Expertise You Can Trust

California’s insurance landscape is complex, with wildfire risks, earthquake exposure, and coastal hazards that require specialized knowledge. An independent insurance agent in California understands these regional challenges and can match you with coverage that actually fits your situation.

At Cappuccino Insurance Agency, we’ve seen how local expertise makes the difference between adequate protection and costly gaps. Working with an independent agent means getting personalized guidance instead of one-size-fits-all policies.

Why Independent Agents Understand California’s Real Insurance Challenges

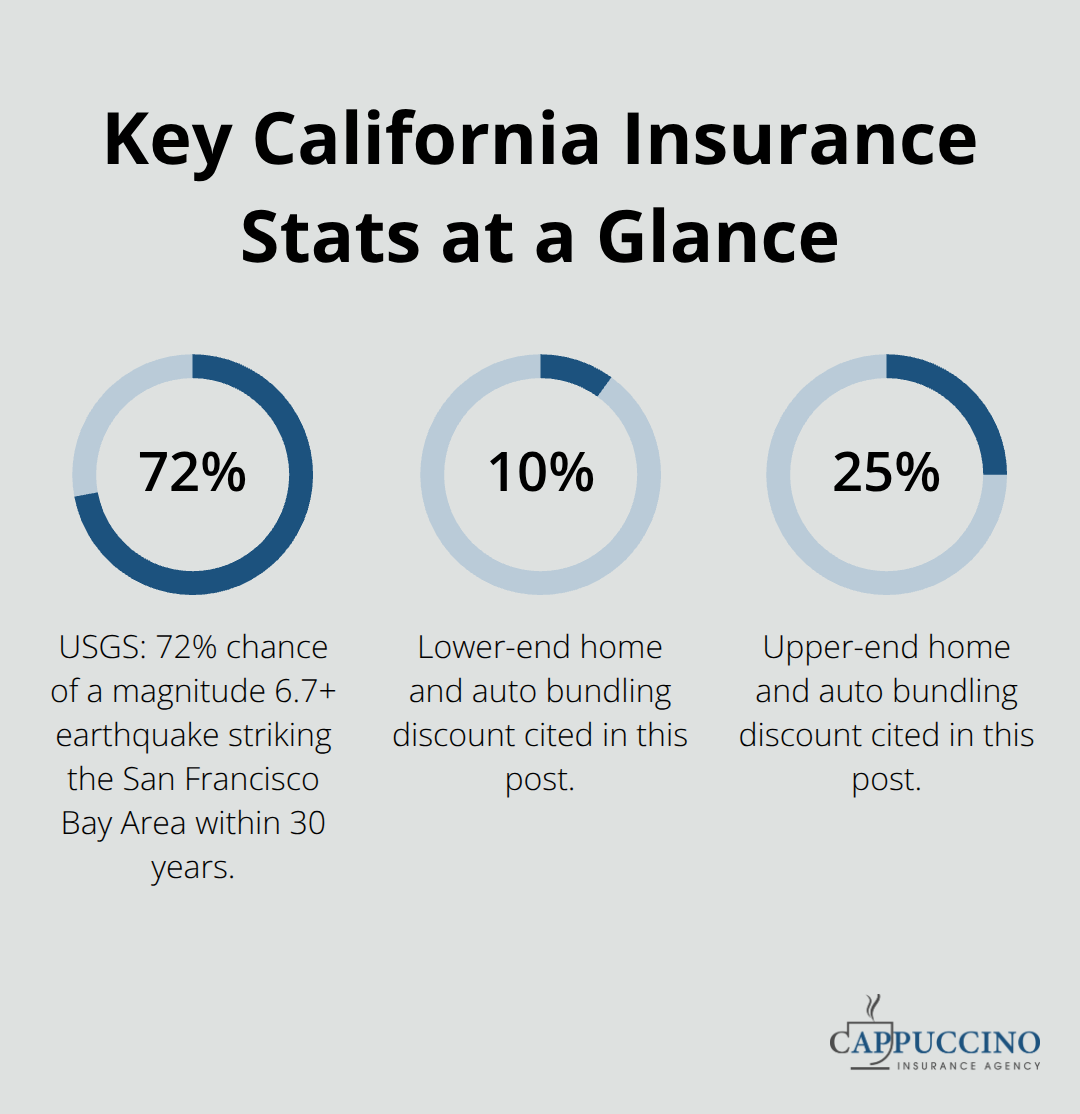

California’s insurance environment demands more than generic coverage templates. Wildfire risk affects over 11 million California residents according to the California Department of Forestry and Fire Protection, with homes in high-risk zones facing coverage denials or premium spikes from standard carriers. Earthquake exposure compounds this reality-the U.S. Geological Survey estimates a 72% probability of a magnitude 6.7 or larger earthquake hitting the San Francisco Bay Area within the next 30 years. An independent agent doesn’t just acknowledge these risks; they navigate them daily. Independent agents work with clients across California’s diverse landscapes, from coastal properties facing flood and wind exposure to Tri-Valley homes vulnerable to the Hayward Fault. This isn’t theoretical knowledge-it’s the difference between receiving approval for coverage and facing rejection from carriers unfamiliar with regional underwriting nuances.

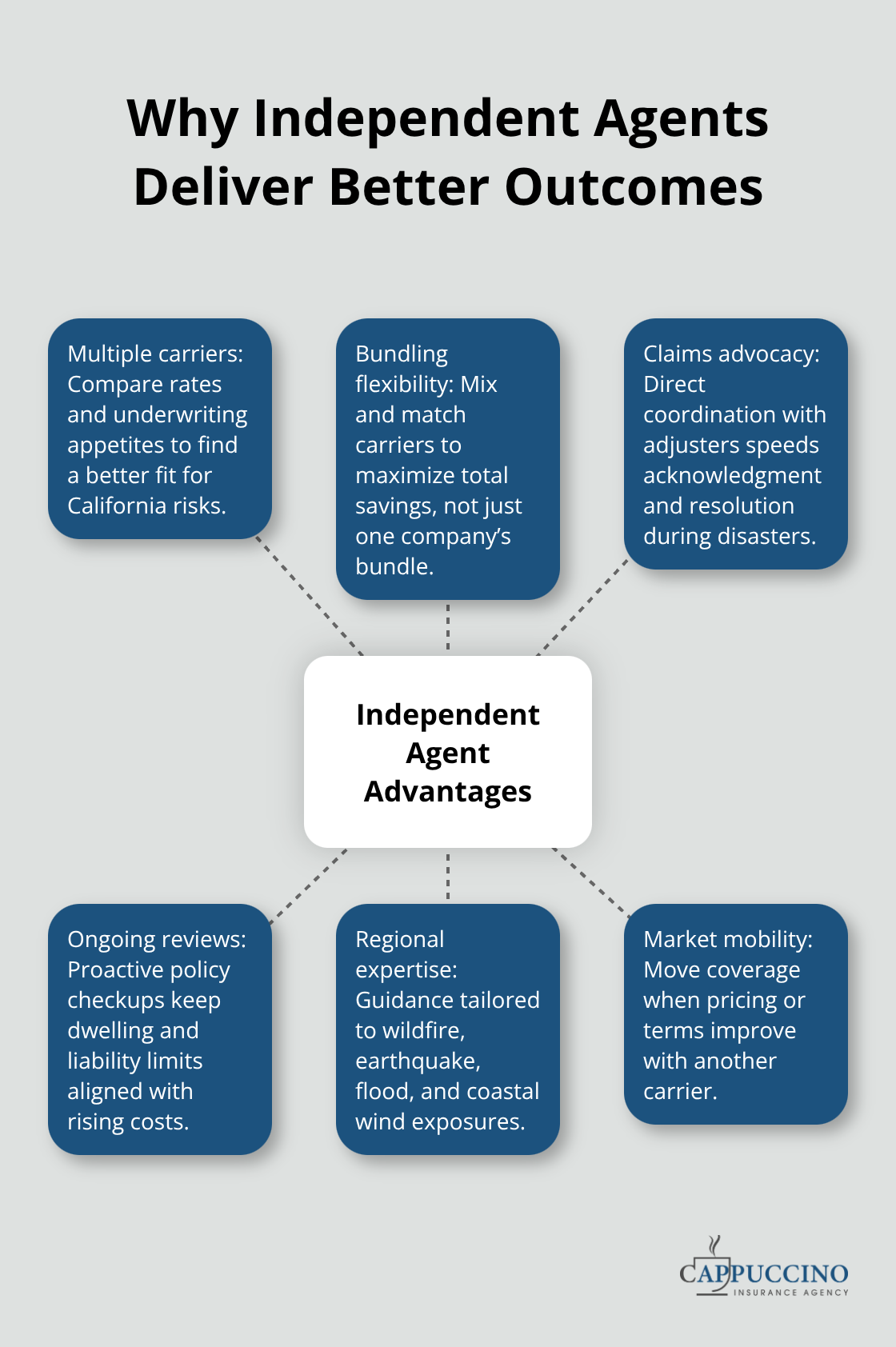

When you work with a captive agent tied to a single insurer, that carrier’s appetite for California risk determines what you can buy. An independent agent accesses 20+ carriers with varying risk tolerances, meaning a property declined elsewhere often finds competitive coverage through the right market fit.

Long-Term Relationships Build Accountability

Independent agents build their reputation on long-term client retention, not transaction volume. This creates accountability that direct online insurers simply don’t have. When you call your independent agent at renewal time, that agent remembers your home’s wildfire mitigation efforts, your claim history, and the specific coverage gaps you discussed last year. Direct insurers process thousands of renewals through automated systems; your file becomes a data record, not a relationship. Clients who work with independent agents receive proactive outreach when their circumstances change-a new home addition, a young driver on the policy, or increased earthquake risk from local development. These conversations happen before renewal notices arrive, giving you time to adjust coverage properly. Additionally, independent agents advocate directly with carriers on your behalf during claims. If a dispute arises over coverage interpretation or claim handling, your agent has a relationship with the carrier’s claims team and can escalate issues effectively. Direct insurers offer customer service phone lines; independent agents offer someone who knows your file inside and out and has carrier connections to resolve problems faster.

Claims Support That Accelerates Resolution

The real test of an insurance relationship isn’t the policy sale-it’s what happens after a loss. California’s wildfire season produced significant losses, and homeowners with independent agents reported faster claim acknowledgment and resolution than those working with direct insurers, according to feedback from regional agent networks. An independent agent familiar with your property can guide you through the claims process immediately, helping you document losses and navigate coverage questions while you manage the emergency. This matters enormously. Carriers receive thousands of claims simultaneously during disasters; an agent who knows your policy details and communicates directly with the claims adjuster accelerates the process. Clients receive claim checks weeks faster because their independent agent provides clear documentation and clarifies coverage interpretation without the homeowner needing to repeat themselves to multiple service representatives. Direct insurers route all claims through centralized call centers with no agent advocacy; you navigate the process and prove your case alone.

Finding an Agent Who Knows Your Region

Not all independent agents possess equal expertise in California’s regional risks. An agent operating in the Tri-Valley understands Hayward Fault exposure differently than one serving coastal San Diego. An agent familiar with wildfire zones knows which carriers accept properties in high-risk areas and which ones don’t. When you select an independent agent, ask about their specific experience with your region’s dominant risks-whether that’s earthquake, wildfire, flood, or coastal wind. An agent who has handled claims in your area brings practical knowledge that translates directly into better coverage recommendations. This regional specificity separates agents who simply sell policies from agents who truly understand your insurance needs.

How Independent Agents Access Better Rates and Broader Coverage

Multiple Carriers Create Real Pricing Advantages

Direct insurers limit you to their single rate card and underwriting guidelines. Independent agents work with multiple carriers, meaning properties rejected by one insurer often qualify for competitive coverage through another. This isn’t a minor advantage-it’s the difference between finding affordable coverage and facing denial. A homeowner in a high-fire-risk zone might be declined by Progressive but approved by Travelers at a reasonable rate. A driver with a minor accident history might face steep premiums from GEICO but find better pricing through Cincinnati Insurance. When you shop with a direct insurer, you see one quote.

When you work with an independent agent, you compare actual rates across carriers with different risk appetites and pricing models. Independent agents can shop the market and move your coverage to another carrier if better pricing or coverage emerges, creating genuine advantages that accumulate significantly over time.

Bundling Delivers Savings Only Agents Can Unlock

Bundling home and auto coverage amplifies pricing benefits-discounts range from 10 to 25 percent depending on the carriers involved. Only an independent agent can identify which combination of carriers delivers the best total savings rather than forcing you into a single company’s bundle. A captive agent ties you to one insurer’s bundled rates. An independent agent compares bundled options across multiple carriers, sometimes finding that splitting coverage between two insurers (one for home, another for auto) produces better overall savings than bundling with either carrier alone. This flexibility exists only when an agent accesses multiple markets.

Complex Situations Require Carrier Flexibility

Complex California situations demand carrier flexibility that captive agents cannot provide. Wildfire exposure, earthquake risk, coastal properties, and rental units require underwriting expertise across multiple markets. A rental property in the Tri-Valley faces different risk assessment than a primary residence, and carriers price accordingly-but only agents accessing multiple markets can find the right fit at the right price. Cappuccino Insurance Agency regularly assesses coverage annually, not just at renewal, identifying gaps created by property changes, new construction, or shifting risk profiles. Direct insurers send renewal notices once yearly with automated adjustments. An independent agent proactively reviews whether your dwelling limits keep pace with East Bay construction costs, whether your liability coverage reflects current California risk exposure, and whether new coverage options have emerged that better serve your situation.

Ongoing Reviews Prevent Coverage Gaps

This ongoing relationship prevents the common problem of discovering coverage shortfalls during claims. A homeowner discovering that their dwelling limit hasn’t increased with rebuilding costs, or that their liability limit is inadequate, learns this lesson expensively. Independent agents catch these gaps before loss occurs, adjusting coverage to match your actual protection needs rather than letting policies stagnate. When circumstances shift-a home addition, a young driver joining the household, or increased earthquake risk from local development-an independent agent identifies the coverage adjustments needed immediately. Direct insurers process renewals through automated systems; independent agents engage in conversations that reveal changing protection needs.

The Carrier Selection Process Matters

Selecting an independent agent means gaining access to carriers willing to underwrite California’s unique risks. Some carriers specialize in wildfire-prone properties; others excel with earthquake exposure or coastal wind risk. An agent familiar with each carrier’s underwriting preferences matches your property to the right market, securing approval and competitive rates simultaneously. This market knowledge separates agents who simply process applications from agents who strategically place coverage. The next step in protecting your California home involves understanding what specific coverage types address your region’s dominant risks and how an independent agent tailors those protections to your situation.

Selecting an Agent Who Understands California’s Insurance Landscape

Choosing the right independent agent requires evaluating three concrete factors that directly impact your coverage quality and pricing.

Verify Licensing and Carrier Access

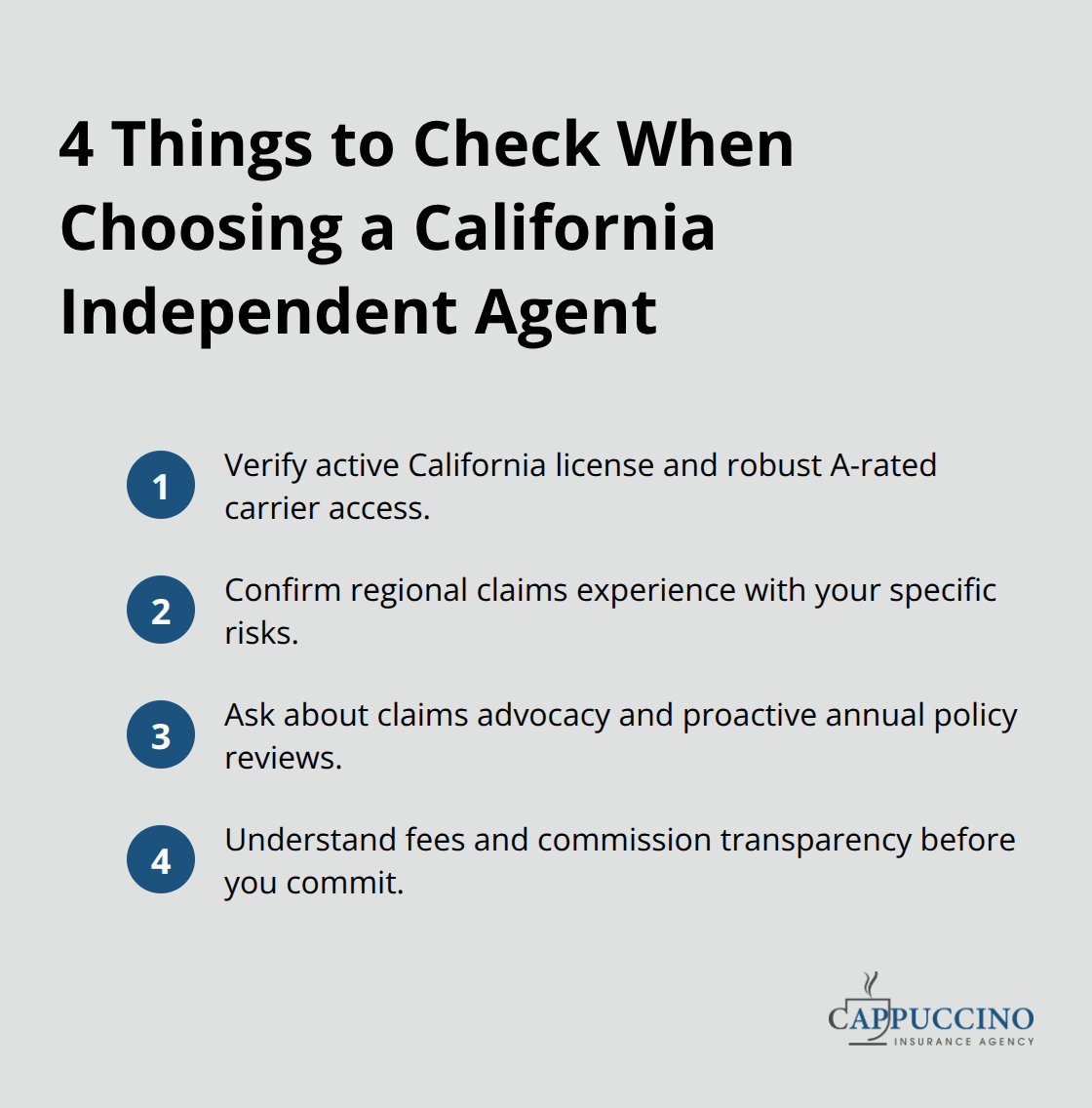

Start by confirming that your agent holds an active California insurance license through the California Department of Insurance website. This verification confirms the agent operates under state supervision and meets continuing education requirements. Beyond licensure, ask which carriers the agent represents. An agent accessing 15+ A-rated carriers like Travelers, Liberty Mutual, Cincinnati Insurance, and Western Reserve Group can navigate California’s complex risk environment far more effectively than an agent working with five carriers. Request specifics: which carriers do you work with, and which ones specialize in wildfire or earthquake coverage? An agent who hesitates or provides vague answers hasn’t invested the effort to understand their own market access.

Evaluate Regional Expertise Through Claims Experience

Ask prospective agents about specific claims they’ve handled in your area. If you’re in the Tri-Valley, ask how many earthquake claims they’ve processed near the Hayward Fault. If you’re in a high-fire zone, ask which carriers they’ve successfully placed with in recent wildfire seasons.

An agent operating in your region for five or more years brings practical knowledge about which underwriters accept properties others reject and which coverage combinations work best for local risks. Request references from clients with similar properties-a wildfire-exposed home, a rental unit, or a property with earthquake concerns. This direct feedback reveals whether the agent truly understands your specific risk profile.

Assess Claims Support and Policy Review Practices

Compare service availability by understanding how the agent handles claims support and annual reviews. Does the agent conduct proactive policy reviews, or do you only hear from them at renewal? Can you reach someone directly during business hours, or do you navigate a call center? Ask prospective agents about their claims advocacy process-specifically, whether they communicate directly with carriers’ claims teams on your behalf. An agent who remains involved after you file a claim accelerates resolution and prevents claim denials caused by coverage misinterpretation. This ongoing relationship distinguishes agents who simply process transactions from those who actively protect your interests.

Understand Fee Structures and Commission Transparency

Confirm how the agent structures fees and commissions upfront. Most independent agents earn commissions from carriers rather than charging service fees, but verify this directly. If an agent charges service fees, understand what those fees cover and whether they reduce commissions. Transparent pricing prevents surprises and builds confidence that your agent prioritizes your interests over higher commissions. This clarity matters significantly when you’re comparing agents and want to understand the true cost of their services.

Final Thoughts

California’s insurance needs demand more than standard policies and generic advice. The regional risks you face-wildfire exposure, earthquake probability, and coastal hazards-require an independent insurance agent in California who understands your specific situation and accesses carriers willing to underwrite it. An agent who conducts annual reviews catches coverage shortfalls before loss occurs, while carrier relationships accelerate claims resolution when you need it most.

Local relationships create accountability that direct insurers cannot match. When you work with an independent agent familiar with your area, that agent remembers your property details, your risk profile, and your coverage goals. This continuity translates directly into better protection and lower premiums over time, and the financial advantage compounds significantly across years of coverage.

Independent agents access multiple carriers with different risk appetites and pricing models, meaning properties rejected elsewhere often find competitive coverage through the right market fit. Bundling discounts range from 10 to 25 percent, but only an independent agent identifies which carrier combination delivers your best total savings. Contact Cappuccino Insurance Agency to schedule your coverage assessment today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.