California Homeowners Insurance: Personalized Protection For Your Home

California homeowners face a perfect storm of insurance challenges. Rising premiums, limited carrier availability, and wildfire exposure have made finding adequate coverage harder than ever.

At Cappuccino Insurance Agency, we help homeowners navigate these complexities and build protection strategies tailored to California’s unique risks. This guide walks you through your coverage options and shows you how to identify gaps in your current policy.

Why California Homeowners Face a Coverage Crisis

California’s insurance market has fundamentally shifted. The state’s median annual home insurance cost reached approximately $1,200 in 2023, according to analysis from the Terner Center, and premiums continue climbing as carriers reassess wildfire risk. Since 2018, California has experienced seven of the largest wildfires in state history, forcing insurers to either raise rates substantially or exit the market entirely. This isn’t theoretical risk-it’s reshaping who can afford coverage and where insurers will write policies. The California Department of Insurance reports that some carriers have paused or restricted new business in the private market since 2023, leaving homeowners with fewer options even as their replacement costs climb. For mobile-home owners, the situation is particularly severe, with premiums reaching $400–$500 per $100,000 of covered value, compared to roughly $182 per $100,000 for single-family homes. If you own property in a wildfire-prone ZIP code, you’re not just paying more-you may struggle to find an insurer willing to write your policy at all.

The Real Cost of Underinsurance

Many California homeowners mistakenly assume their standard policy covers the full cost to rebuild. It doesn’t. Dwelling coverage should reflect replacement cost, not market value, and the Terner Center data shows that newer homes built after 2009 have lower costs per $100,000 of value (around $150) compared to older homes (around $200). This matters because construction costs in California have accelerated due to stricter fire safety and seismic building codes. If your policy limits fall short of actual replacement costs-a problem affecting thousands of homeowners-you’ll face out-of-pocket expenses after a loss. Extended replacement cost coverage, which can increase rebuilding funds up to 150% of your base limit, addresses this gap precisely. Without it, you risk being short when contractors bill you for code-compliant rebuilds.

Why Location and Risk Profile Drive Your Premium

Your premium reflects your specific property’s wildfire exposure, not statewide averages. A home in a defensible-space area with a Class A fire-rated roof and ember-resistant vents qualifies for mandatory wildfire mitigation discounts under California’s Safer From Wildfires rules. These discounts are not optional incentives-they’re required by law. Taking concrete steps like installing multi-paned windows, creating noncombustible ground zones, or moving combustible structures 30 feet from your home can meaningfully reduce your rate. If you’ve invested in resilience upgrades, your insurer must reflect those improvements in your premium. If they haven’t, you’re overpaying.

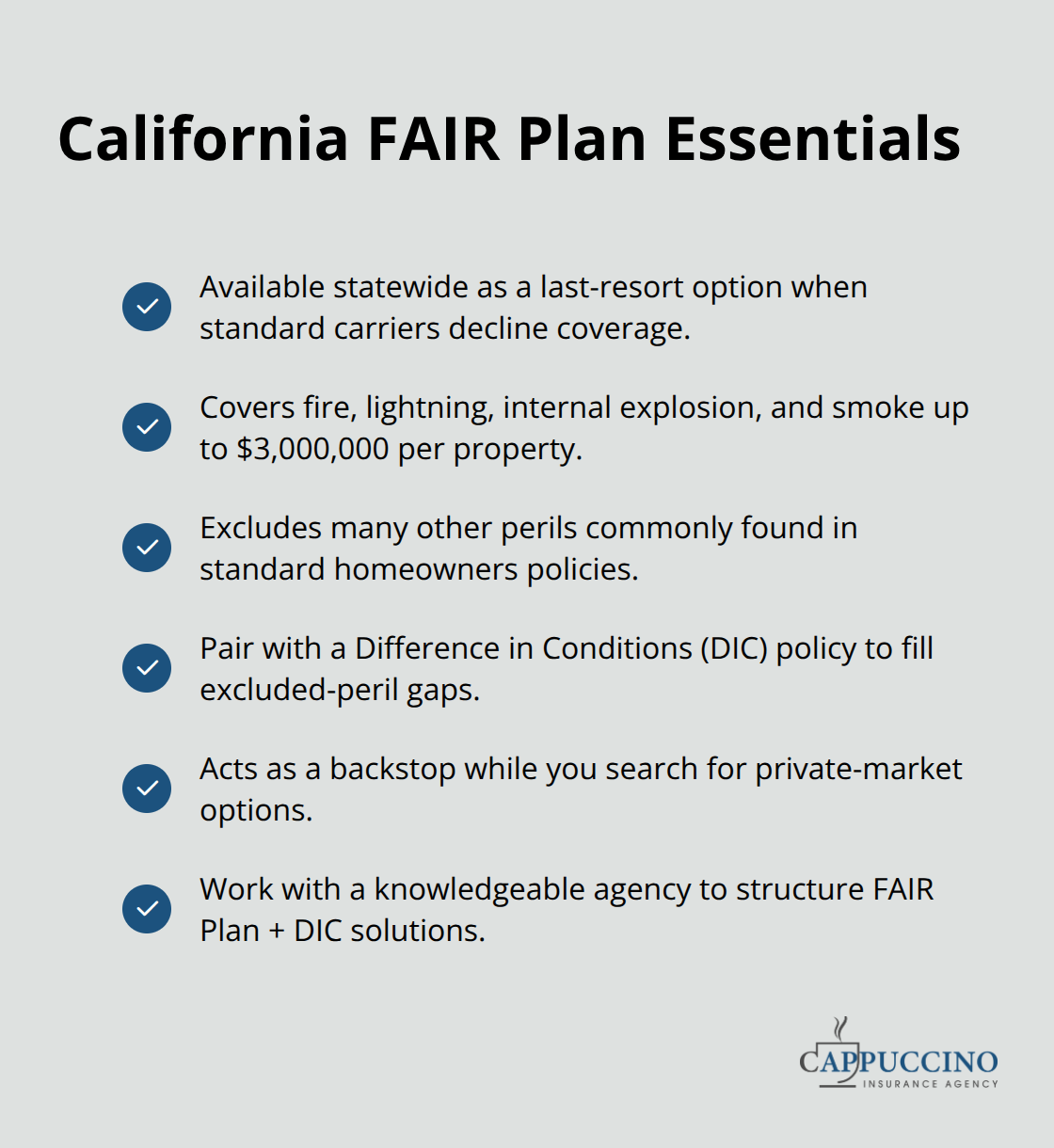

Navigating Hard-to-Place Properties

Some California homeowners face outright rejection from standard carriers. High wildfire risk, older construction, or previous claims can trigger nonrenewals or coverage denials. When this happens, the California FAIR Plan serves as a backstop-it’s available to every homeowner as a last-resort option. The FAIR Plan covers losses from fire, lightning, internal explosion, and smoke up to a combined maximum of $3,000,000 per property. However, FAIR Plan coverage excludes other perils, so most homeowners add a Difference in Conditions policy to fill those gaps. At Cappuccino Insurance Agency, we help clients secure specialty solutions for hard-to-place properties, including FAIR Plan policies paired with DIC wraps to restore broader protection.

This approach ensures you’re not left uninsured while you search for standard market options.

What Your Standard Policy Actually Covers (And What It Doesn’t)

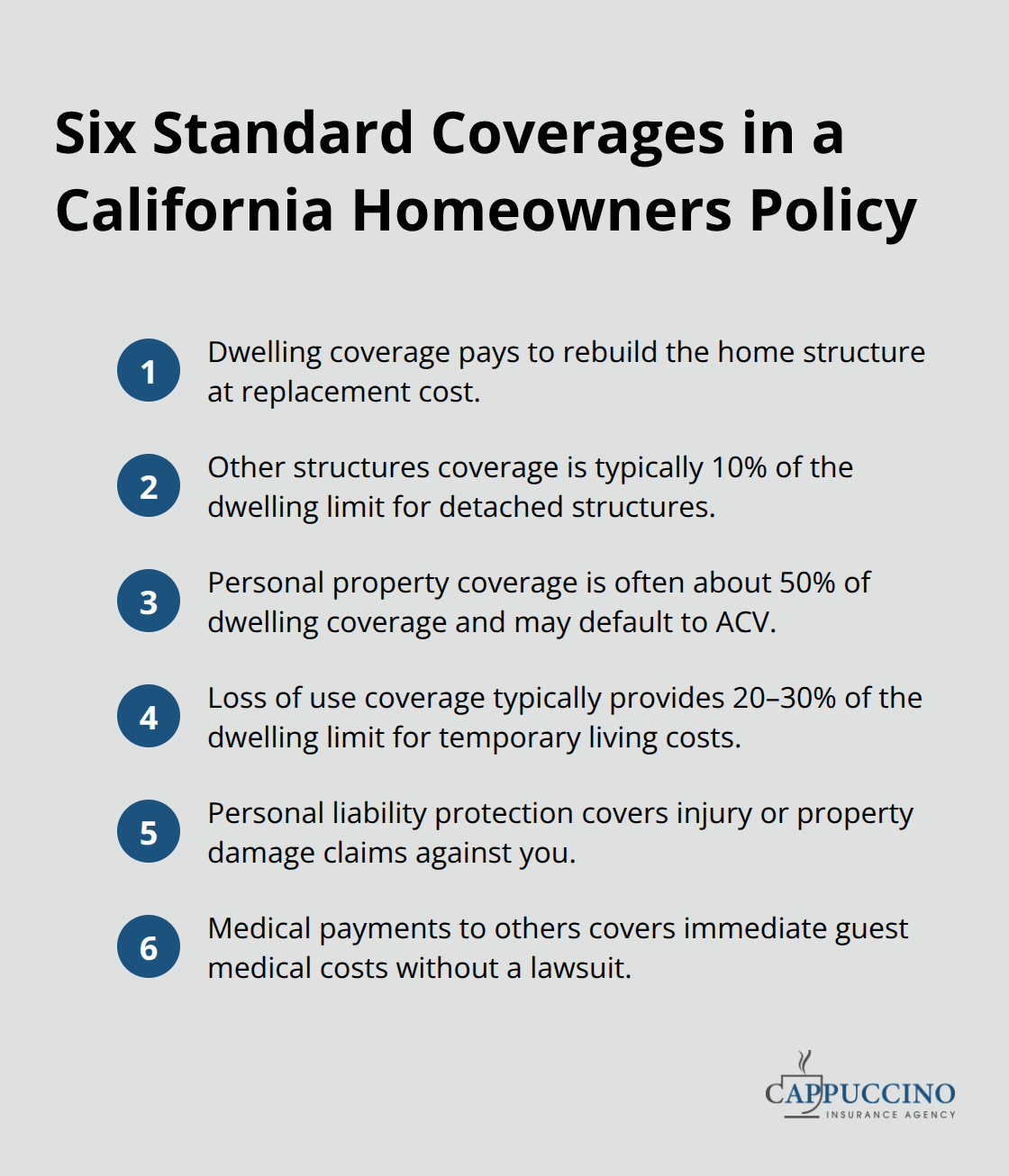

A California homeowners policy includes six standard coverages, and understanding what each one delivers is the first step toward identifying gaps in your protection. Dwelling coverage pays to rebuild your home structure itself, excluding the land, and should always reflect replacement cost rather than market value. Other structures coverage typically runs at 10% of your dwelling limit and covers detached garages, sheds, or guest houses, though you’ll need to adjust this upward if you have an accessory dwelling unit or rental structure. Personal property coverage, often set around 50% of dwelling coverage, protects your belongings inside the home, but here’s where most California homeowners slip up: this coverage applies actual cash value rather than replacement cost value, meaning your three-year-old television depreciates before you file a claim. Loss of use coverage, typically 20–30% of your dwelling limit, reimburses temporary living expenses if your home becomes uninhabitable after a covered loss. Personal liability protection ranges from $100,000 to $500,000 per occurrence and covers damages if someone is injured on your property and sues. Medical payments to others, usually $1,000–$5,000 per person, covers immediate medical costs for guests injured on your property without requiring a lawsuit. These six components form your baseline, but California’s construction costs and wildfire reality demand more.

Flood and Earthquake Coverage Require Separate Policies

Standard policies exclude flood damage entirely, which means living near any floodplain or low-lying area requires a separate flood insurance policy through the National Flood Insurance Program. Earthquake damage is also excluded, and you must purchase earthquake coverage separately, typically through the California Earthquake Authority with deductibles ranging from 5–25% of your dwelling limit. These two exclusions represent massive exposure for California homeowners, yet many assume their standard policy covers both. It doesn’t. If a winter storm triggers flooding or a seismic event damages your foundation, your standard homeowners policy leaves you unprotected.

Extended Replacement Cost Addresses Rising Construction Expenses

Extended replacement cost coverage is an optional endorsement that expands your base dwelling coverage and helps pay for extra rebuilding costs outside your standard limit. Without it, you’re betting that your current limit matches what contractors will actually charge in 2026 or 2027. Construction costs in California have climbed faster than national averages, and code-compliant rebuilds cost substantially more than pre-loss estimates. This endorsement protects you from that gap.

Specialized Endorsements Fill Critical Gaps

Service line and buried utility protection covers water lines, sewer lines, and electrical lines running from your home to the street, protecting you from costs that can reach $10,000 or more. For high-value items like jewelry, fine art, or collectibles, a scheduled personal property endorsement provides specific coverage limits without depreciation. If you have solar panels or battery backup systems, you need an equipment endorsement to ensure those investments are covered. Ordinance or law coverage pays the difference between rebuilding to your home’s original construction standards and rebuilding to current California codes, which can add 10–25% to total reconstruction costs depending on your location and home age. This coverage matters significantly because California’s fire safety and energy efficiency standards have tightened substantially.

Identifying What Your Policy Actually Covers

The gap between what your standard policy covers and what your home actually needs grows wider each year as California’s building codes evolve. Most homeowners discover these gaps only after a loss occurs, when contractors present bills that exceed policy limits or when claims get denied for excluded perils. The solution is straightforward: request a detailed coverage review from your agent that lists all six standard coverages, their limits, and any exclusions specific to your property. Ask which endorsements apply to your situation and which ones you’re missing. This conversation reveals whether your dwelling limit reflects actual replacement cost, whether your personal property coverage uses actual cash value or replacement cost value, and whether you have adequate liability limits for your neighborhood and property type. Understanding these details now prevents expensive surprises later.

How to Find an Insurer That Matches Your California Property

Finding the right carrier in California’s fractured insurance market requires abandoning the assumption that all homeowners policies are interchangeable. The differences between carriers, their underwriting criteria, and their willingness to write coverage in wildfire zones are vast. Local agents tailor custom plans to regional risks and location-specific conditions across California, accounting for geographic variables like Joshua Tree’s heat exposure versus Northern California’s cold winters. However, comparing carriers demands specificity. The Consumer Federation of America reports an average annual premium around $1,724 for approximately $350,000 of dwelling coverage, yet this masks enormous regional variation. A home in a Firewise USA certified community may qualify for substantially lower premiums than an identical home three miles away in an unmitigated area.

Document Your Property’s Risk Profile Before Shopping

Your first step is not contacting five carriers for quotes-it’s documenting your property’s actual risk profile and mitigation investments. Have you installed a Class A fire-rated roof? Do you have noncombustible ground zones within 30 feet of your structure? Have you created ember-resistant vents and multi-paned windows? These concrete measures qualify for mandatory wildfire mitigation discounts under Safer From Wildfires rules, and many homeowners fail to communicate them to insurers, resulting in inflated premiums. Before shopping, photograph your defensible space, document any fire-resistant upgrades, and gather your property’s construction date and square footage. Carriers use this information to assign accurate risk ratings, but they cannot do so if you don’t provide it.

Compare Quotes Across Multiple Carriers

Once you document your property’s resilience investments, comparing carriers becomes actionable rather than abstract. Request quotes from at least three carriers that actively write in your ZIP code, and critically, ask each one whether they’ve applied all eligible wildfire mitigation discounts to your quote. Many homeowners receive quotes that omit these discounts entirely, meaning they’re seeing artificially high premiums. The California Department of Insurance publishes a Residential Insurance Company Contact List with toll-free numbers for over 50 licensed homeowners insurers, and you can use the Home Insurance Finder tool to locate agents representing different carriers in your area.

When you obtain quotes, compare not just the annual premium but the specific coverage limits, deductibles, and exclusions for each policy. A $1,500 annual premium means nothing if the policy includes a $5,000 deductible for wind damage or lacks extended replacement cost coverage. This detailed comparison reveals which carriers actually match your property’s needs and which ones simply offer the lowest sticker price.

Solutions for Hard-to-Place Properties

For hard-to-place properties where standard carriers decline coverage, the California FAIR Plan serves as your backstop, covering fire, lightning, internal explosion, and smoke losses up to $3,000,000 per property. However, FAIR Plan policies exclude other perils, so pairing one with a Difference in Conditions policy through a retail agent or broker restores broader protection. Cappuccino Insurance Agency partners with 20+ carriers to deliver specialty solutions for properties that struggle to secure standard market coverage, including FAIR Plan policies with DIC wraps that provide comprehensive protection when private insurers restrict underwriting.

Get Help When Facing Nonrenewal or Rejection

If you’re in a nonrenewal situation or face repeated rejections, contact your state’s Department of Insurance toll-free at 1-800-927-4357 for multilingual assistance locating available carriers and understanding your options. The department maintains resources and tools to help you navigate coverage gaps and identify insurers still writing in your area.

Final Thoughts

California homeowners insurance demands annual attention because your policy from three years ago likely underprotects you today. Construction costs climb, wildfire risk evolves, and coverage gaps compound over time-a $50,000 shortfall in dwelling limits becomes a $100,000 problem when rebuilding expenses spike. Start by requesting a detailed coverage review that confirms your dwelling limit reflects actual replacement cost, verifies all eligible wildfire mitigation discounts apply to your premium, and identifies missing extended replacement cost coverage or inadequate liability limits.

If you’ve made fire-resistant upgrades since your last renewal, document them and ensure your insurer knows about them. For homeowners facing nonrenewal or rejection from standard carriers, the California FAIR Plan and specialty solutions exist specifically for your situation. These gaps aren’t minor oversights-they’re the difference between rebuilding your home and facing financial hardship after a loss.

We at Cappuccino Insurance Agency provide free coverage assessments and annual policy reviews to help you identify gaps and secure the best protection at the right price. We partner with 20+ carriers to deliver solutions for hard-to-place properties, including FAIR Plan policies with Difference-in-Conditions wraps. Schedule your annual review today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.