Commercial Auto Insurance Quotes: Compare Top Carriers Quickly

Getting commercial auto insurance quotes from multiple carriers takes time, but it doesn’t have to be complicated. We at Cappuccino Insurance Agency help business owners understand what goes into these quotes and how to compare them side by side.

The right policy protects your vehicles and your bottom line. This guide walks you through the entire process, from what insurers ask for to spotting the best rates and discounts available.

What Information Carriers Need and How They Calculate Your Quote

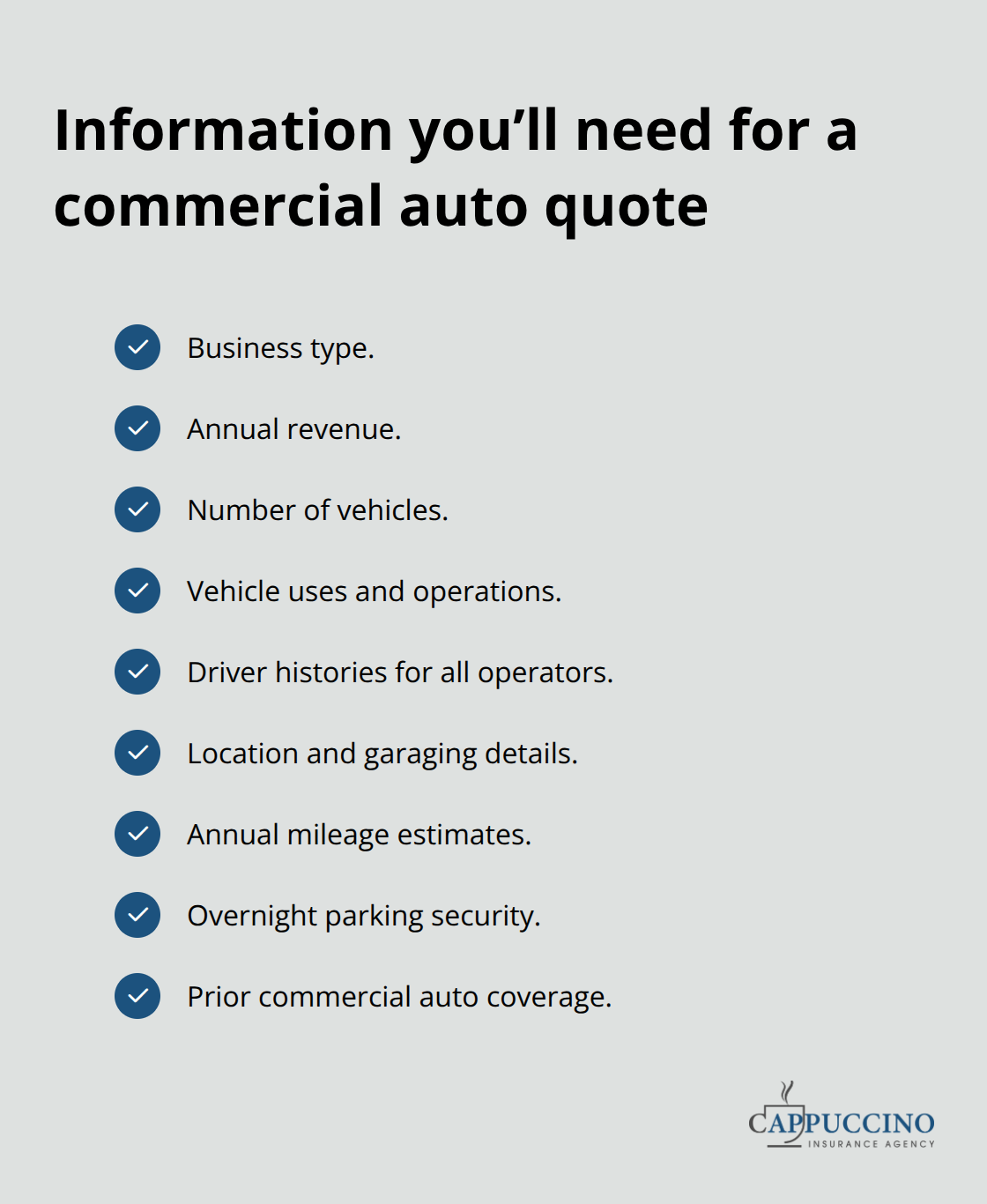

The Data Carriers Request

Carriers need specific data to calculate your commercial auto quote accurately, and the faster you provide it, the sooner you receive rates back. Insurance companies ask for your business type, annual revenue, number of vehicles, and the specific uses of those vehicles because these factors directly impact risk assessment. They request your driving history and the driving records of anyone who operates company vehicles, since drivers with violations or accidents represent higher claims costs.

Your location matters significantly because some states and regions have higher accident rates, theft rates, and regulatory requirements that affect premiums. Most carriers also ask about your annual mileage, whether vehicles stay parked overnight in secure locations, and if you’ve had commercial auto coverage before.

How Quickly You Get Your Quote

Progressive can generate a quote in as little as 8 minutes once you submit this information online. Most carriers deliver quotes within 24 to 48 hours, though some require agent contact rather than instant online quotes. The speed depends on whether you apply through an online portal or work with an agent directly.

The Calculation Process

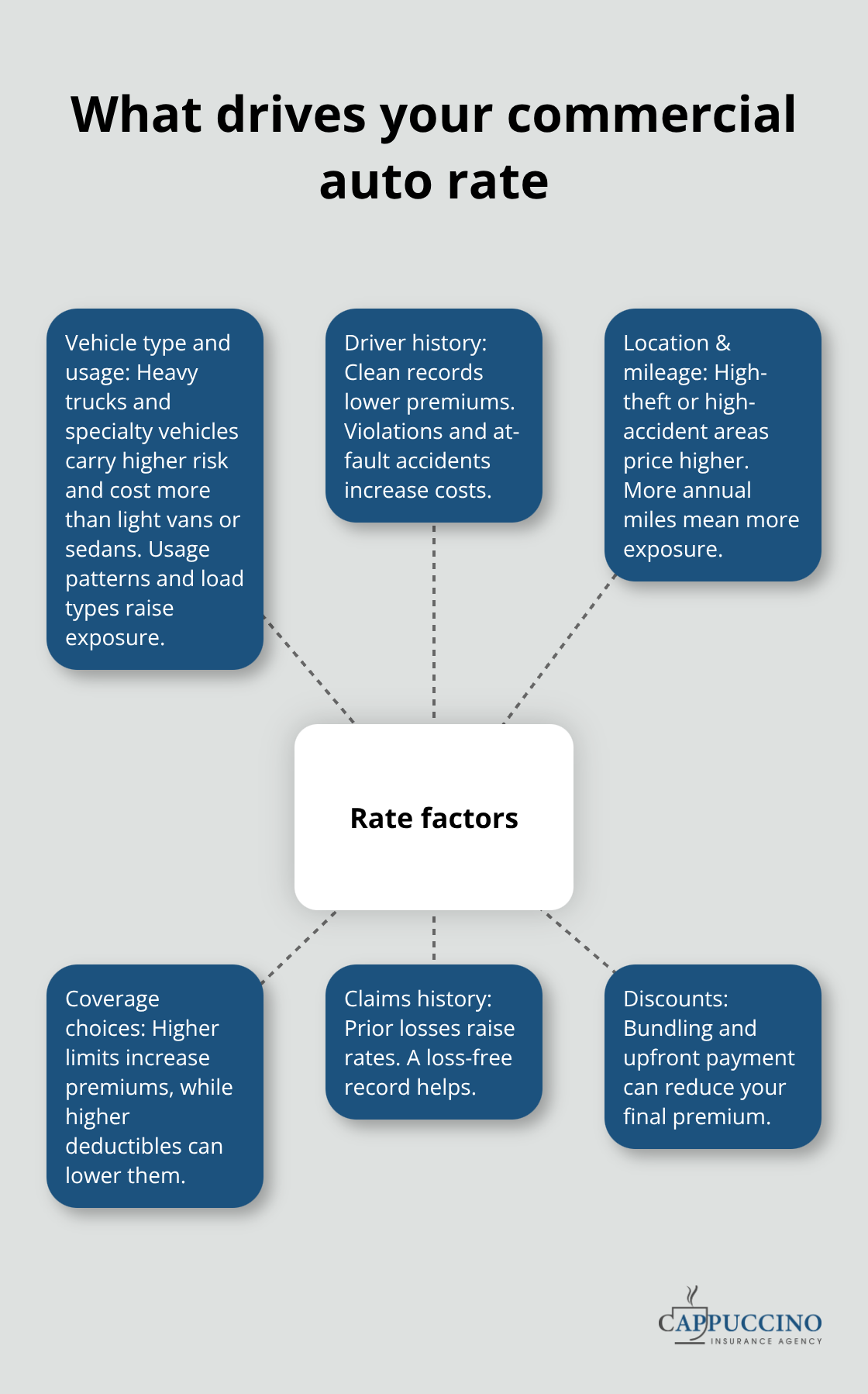

Insurers take your business profile and run it through their underwriting models, which weigh factors like your industry type, vehicle values, coverage limits you select, and claims history. A construction company with heavy trucks receives different rates than a service business with light vans because construction vehicles face different usage patterns and accident exposures. Your deductible choice directly reduces your premium-increasing from a $500 to $1,000 deductible typically lowers costs measurably.

Discounts That Lower Your Premium

Discounts factor in immediately during the calculation process. Bundling with property insurance can save about 12% on average, while paying your entire premium upfront can save 13% or more. Discover proven strategies to maximize your savings on your commercial auto policy.

Why Comparing Multiple Carriers Matters

Shopping multiple carriers reveals real pricing differences and helps you identify which carrier offers the best value for your specific business profile. Rates vary significantly across insurers-comparing the same coverage limits across three to five carriers shows you exactly what each one charges for identical protection. This comparison process sets you up to evaluate coverage limits and deductibles more effectively in the next section.

Key Factors That Affect Your Commercial Auto Insurance Rates

Vehicle Type and Usage Patterns

Your vehicle type determines your baseline risk profile, and insurers price accordingly based on real accident and claims data. A dump truck costs significantly more to insure than a sedan because dump trucks face higher accident rates, carry heavier loads, and require specialized coverage. According to Progressive Commercial, commercial auto insurance costs vary by vehicle type, ranging from $272 monthly for contractor autos to $954 for for-hire transport trucks. Heavy trucks, box trucks, and specialty vehicles like tow trucks command higher premiums than light vans because they operate under different exposure conditions. Insurers calculate rates separately for each vehicle type, then bundle them into your overall policy cost.

Driver History and Experience

Driver history matters more than most business owners realize, and a single violation can increase your rates substantially. Insurers examine not just accidents and at-fault claims, but also traffic violations like speeding tickets, reckless driving charges, and DUI convictions from the past three to five years. If your company employs multiple drivers, each one’s record affects your policy price, which is why some carriers ask for the driving history of everyone who operates company vehicles. A clean driving record lowers your premium, while violations and accidents push costs higher.

Business Location and Annual Mileage

Your location influences rates because state regulations, theft rates, and accident frequency vary dramatically-a business in a high-theft urban area pays more than an identical business in a rural location. Annual mileage also factors heavily since more miles driven means more exposure to accidents. Vehicles that travel 50,000 miles yearly versus 10,000 miles yearly receive different rates accordingly. Gather accurate mileage estimates and secure driver records before requesting quotes so carriers can calculate your actual risk profile rather than making conservative assumptions that inflate your premium.

When you’re ready to compare quotes from multiple carriers, you’ll want to evaluate how these rate factors translate into actual premium differences across insurers. The next section shows you how to analyze coverage limits, deductibles, and discounts to identify which carrier delivers the best value for your business.

How to Compare Commercial Auto Insurance Quotes Effectively

Match Coverage Limits Across All Quotes

Once you have quotes in hand, the real work starts. Most business owners make the mistake of comparing only the monthly premium, but that approach leaves money on the table and often results in inadequate coverage. The premium is just one piece of the puzzle. You need to verify that each quote includes the same coverage limits across all carriers, since commercial policies tend to have higher limits than personal auto policies-it’s riskier to compare without matching them.

Start by selecting your desired liability limits (typically $100,000 per accident for small businesses, though higher limits are common), your collision and comprehensive coverage deductible amounts, and any add-ons you need like rental reimbursement or roadside assistance. Write these specifications down, then request quotes with identical coverage from at least three carriers. Once quotes arrive with matching coverage, the comparison becomes straightforward: line them up side by side and note the premium differences.

Analyze Premium Differences Across Carriers

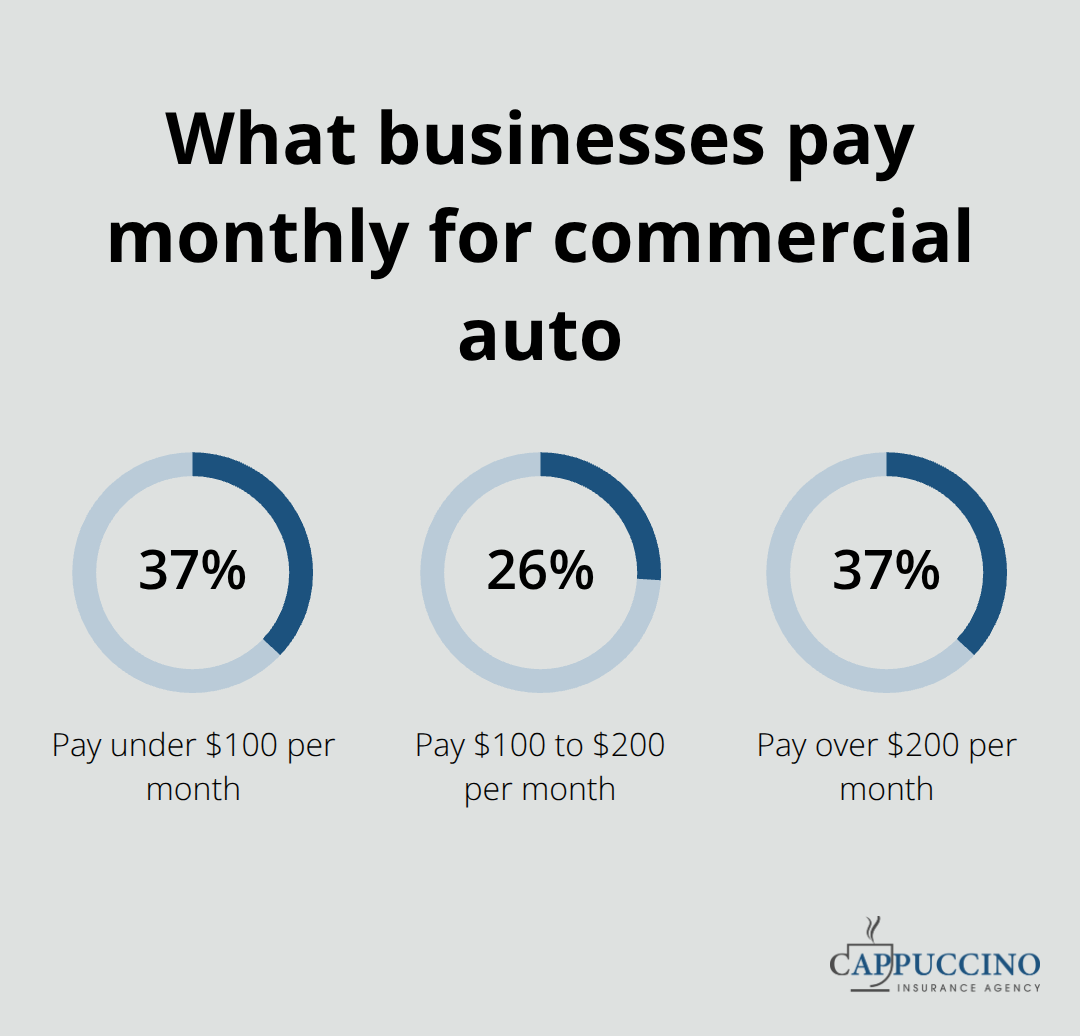

According to industry data, 37% of businesses pay under $100 monthly for commercial auto insurance, 26% pay between $100 and $200, and 37% pay over $200, but these ranges shift dramatically based on vehicle type and industry. A construction company might pay around $173 monthly on average, while an IT business could see $198, so your specific industry matters far more than general benchmarks.

A difference of $50 to $100 monthly between carriers is normal and worth investigating, but a difference of $200 or more signals either superior value or inadequate coverage that you need to examine more closely. Progressive Commercial data shows that median monthly costs reach about $219 for business auto like cleaning services and restaurants, and $212 for contractors, so compare your quotes against these industry benchmarks to spot outliers.

Identify Discounts and Bundle Opportunities

Discounts often determine which carrier delivers real value, and this is where most business owners leave savings unclaimed. Bundling your commercial auto policy with property insurance saves approximately 12% on average according to Progressive data, while paying your entire annual premium upfront can save 13% or more. Some carriers like The Hartford offer online quotes and claims filing plus coverage for lost business income after crashes, which appeals to service-based businesses, while others like Auto-Owners provide telematics discounts that reward safe driving habits and can lower costs further.

If you operate vehicles during only part of the year, seasonal insurance adjustments can cut costs significantly during slow periods-you reduce coverage or switch to comprehensive-only to avoid paying for full protection when vehicles sit idle. Ask each carrier specifically which discounts apply to your business type and location, since eligibility varies widely and not all discounts are available everywhere. Upfront payment discounts alone could save you hundreds annually, and when combined with bundling, the total savings can exceed $1,500 per year on a multi-vehicle policy.

Verify Carrier Reliability and Claims Service

After you’ve identified your lowest-cost option with matching coverage and maximum discounts applied, verify that carrier’s complaint record through the National Association of Insurance Commissioners data. Carriers with 5.0 ratings and very low complaints include Acuity, Auto-Owners, Axis, Federated, The Hartford, Nationwide, and Sentry, so a slightly higher premium from one of these carriers often means better claims service when you actually need it. A carrier’s financial strength and complaint history matter as much as the price you pay today.

Final Thoughts

Comparing commercial auto insurance quotes from multiple carriers reveals real savings opportunities that most business owners miss. The process itself is straightforward: you gather quotes with identical coverage limits, analyze the premium differences across carriers, and identify which discounts apply to your specific business. A difference of $50 to $100 monthly between carriers is normal, but comparing three to five quotes shows you exactly where value lies.

Bundling with property insurance saves approximately 12% on average, while paying your annual premium upfront can save 13% or more, so these discounts often determine your final decision more than the base premium itself. Before you select a carrier, verify their complaint record through NAIC data and confirm they maintain strong financial ratings. Carriers like The Hartford, Nationwide, and Auto-Owners consistently deliver low complaint levels and reliable claims service, which matters when you actually need to file a claim.

Start gathering commercial auto insurance quotes today by contacting carriers that serve your industry and location. Have your business type, vehicle information, driving records, and annual mileage ready so carriers calculate accurate rates quickly. We at Cappuccino Insurance Agency partner with top carriers and can help you compare commercial auto insurance quotes side by side while identifying bundle opportunities and specialty coverage you might need.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.