Apartment Building Insurance California: Coverage For Investment Properties

Apartment building owners in California face unique insurance challenges that most residential property owners never encounter. We at Cappuccino Insurance Agency see firsthand how many investors overlook critical coverage gaps that lead to expensive claim denials.

This guide walks through the specific protections your multi-unit property needs, the factors that drive your premiums, and the common mistakes that leave investors exposed.

What Coverage Does Your Apartment Building Actually Need

Property Coverage Protects Your Building Structure and Systems

Property coverage protects the physical structure of your apartment building, but most California investors misunderstand what this actually covers. Standard property coverage includes the walls, roof, and permanent fixtures, but you need to verify that electrical systems, plumbing, HVAC units, and elevators are explicitly covered. Many policies have separate limits for these systems, and if your building has older equipment, insurers often require documentation of recent upgrades or replacements.

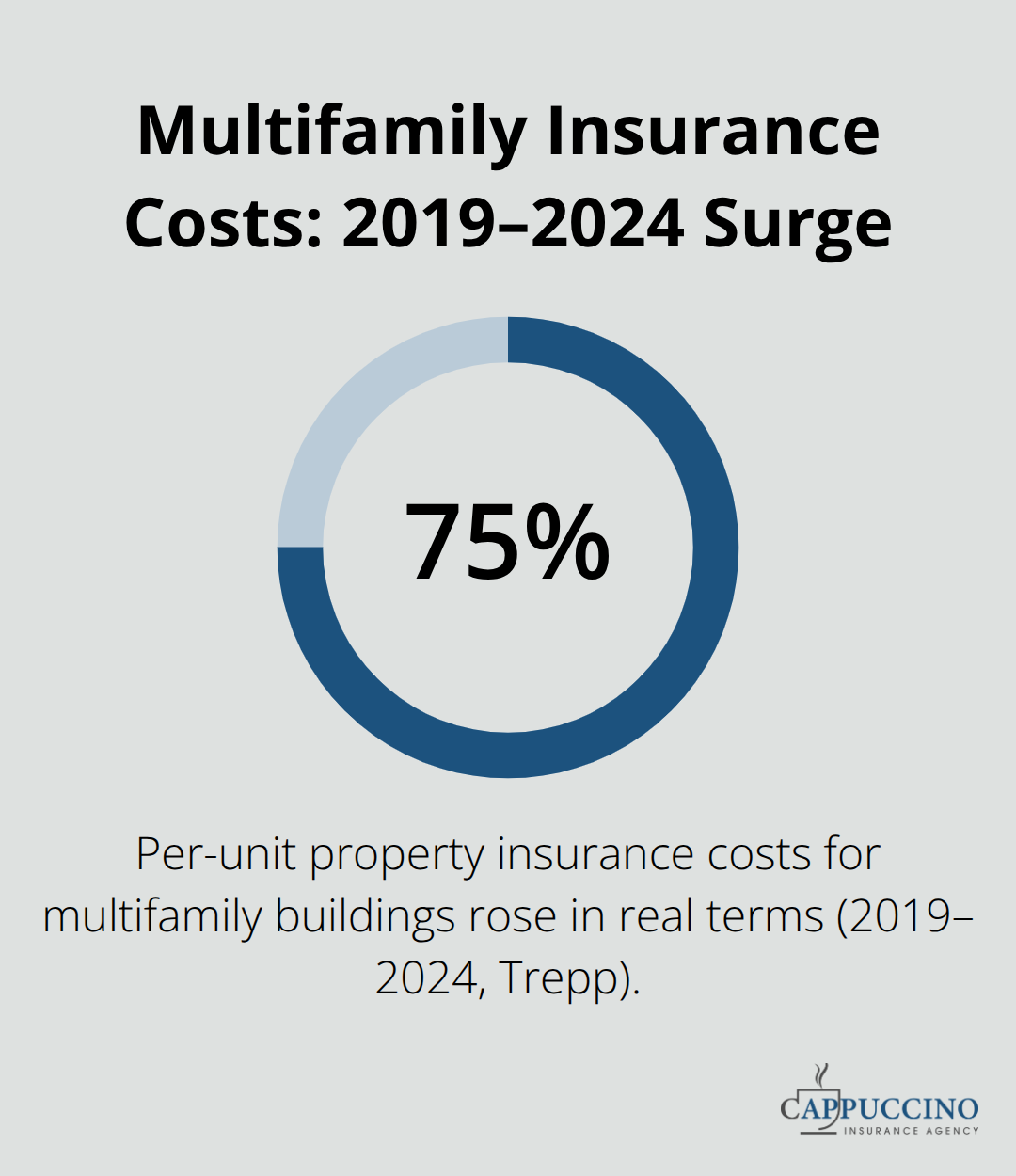

According to Trepp’s analysis of commercial mortgage-backed securities data from 2019 to 2024, per-unit property insurance costs for multifamily buildings jumped from approximately $39 per month to $68 per month in real terms-a 75% increase. This surge reflects not just rate hikes but also increased replacement costs for materials and labor. Your coverage limit must match your building’s actual replacement value, not its market value. An underinsured property creates a coinsurance penalty, meaning the insurer reduces your claim payout proportionally if your coverage falls short of the replacement cost.

Liability Coverage Stops Tenant and Visitor Claims

Liability protection is non-negotiable for multi-unit properties because tenant injuries, visitor accidents, and third-party claims happen regularly in apartment buildings. General liability coverage pays for medical expenses, legal defense costs, and settlements if someone is injured on your property due to negligence. California law requires landlords to maintain habitable premises under Civil Code sections 1940–1954, and insufficient liability coverage exposes you to personal liability beyond policy limits.

Many owners carry only $300,000 to $500,000 in general liability limits, which is dangerously low for a multi-unit building. A single serious injury claim can exceed these limits within months of legal defense alone. Excess liability or umbrella coverage provides additional protection after your primary policy limits are exhausted. Try minimum umbrella limits of $1 million to $2 million for apartment buildings with five or more units. If your building has employees, workers’ compensation is mandatory in California and covers job-related injuries regardless of fault. Employment practices liability insurance protects you against discrimination, harassment, and wrongful termination claims, which are increasingly common in California’s strict regulatory environment.

Rental Income Coverage Protects Cash Flow During Repairs

Loss of rents coverage is the coverage most investors regret not having after a fire, major water damage, or other event forces tenants to vacate. This coverage reimburses the rental income you would have collected while the building is uninhabitable and undergoing repairs. Without it, you still owe your mortgage, property taxes, and maintenance costs while receiving zero tenant income.

A typical claim for a 20-unit building losing rent for three months due to fire damage results in a claim of $60,000 to $90,000, depending on your market rent. California property owners often assume their lender’s hazard insurance covers rental income loss, but it doesn’t-this protection must be added separately to your policy. The coverage usually includes a waiting period of 30 days before payments begin, so you absorb the initial month of lost rent. Earthquake and flood damage are the most common triggers for extended vacancy in California, so if your building is in a seismic zone or flood-prone area, rental income coverage becomes critical. Try coverage limits equal to at least six months of gross rental income, though three months is the practical minimum for most investors.

The specific coverage limits you select depend on your building’s location, age, and tenant profile-factors that also shape your premium costs and underwriting requirements.

What Drives Your Apartment Building Insurance Premiums in California

Building Age and System Condition Set Your Baseline Cost

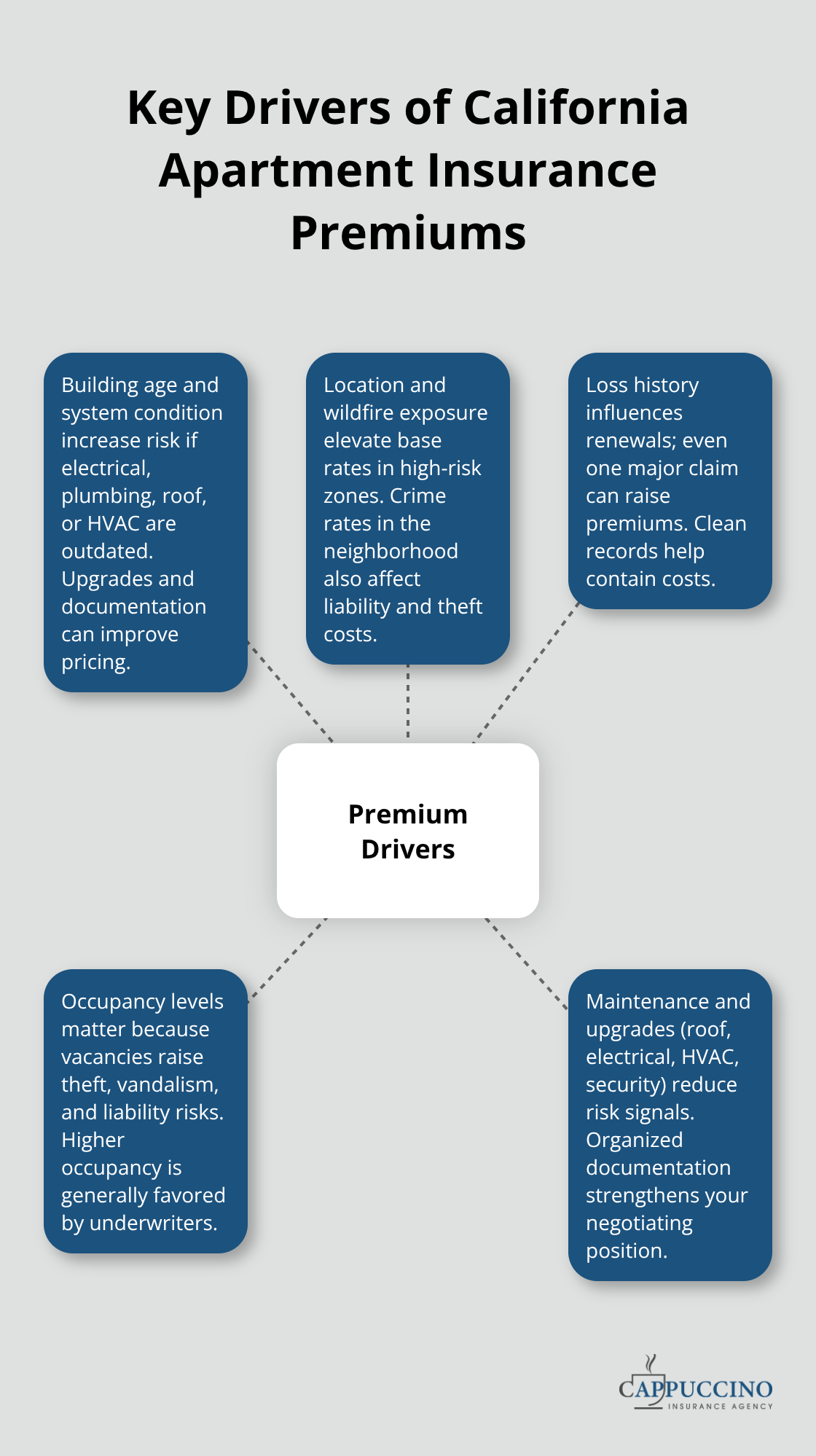

Your building’s age is the single biggest factor determining your insurance cost, and California insurers have become ruthless about older properties. Buildings constructed before 1980 typically pay 40% to 60% higher premiums than newer construction because aging electrical systems, plumbing, and roofs create claim risk. Insurers now demand detailed documentation of any upgrades to your electrical panel, plumbing lines, HVAC system, and roof before they’ll even quote your property.

If your building still has original Zinsco, Stab-Lok, or Federal Pacific electrical panels, many carriers will simply decline coverage or require replacement as a condition of the policy. The replacement cost for these panels runs $3,000 to $8,000 depending on the building size, but it’s non-negotiable with most insurers. Roof age matters equally-anything over 20 years old triggers immediate premium increases or coverage restrictions. The real cost hit comes when you combine building age with location risk.

Location Risk and Wildfire Exposure Drive Regional Premiums

Properties in California’s high-wildfire zones pay substantially more because insurers have absorbed massive losses from recent fire seasons. A building in Santa Rosa or Paradise faces premiums 30% to 50% higher than an identical building 50 miles away in lower-risk areas. Wildfire exposure stands as the dominant reason properties face rejection in California’s standard insurance market, making location one of your least controllable cost factors. Crime rates in your neighborhood also affect your liability and theft coverage costs. Properties in high-crime zip codes see higher premiums because claim frequency data shows more tenant injuries, break-ins, and property damage in those areas.

Insurers pull detailed loss history for your specific property, so even one major claim in the past five years will increase your renewal premium by 15% to 25%. Your occupancy rate directly impacts your premium because vacant units represent higher risk for theft, vandalism, and liability exposure. Insurers view a building with 70% occupancy very differently than one at 95% occupancy.

Tenant Screening and Maintenance History Lower Your Rates

Tenant screening practices matter more than you’d think because insurers know that properties with rigorous screening have fewer claims. If you can document that you conduct background checks, verify income at three times the rent, and check references, you have leverage to negotiate lower rates at renewal. Trepp’s 2019–2024 analysis showed that per-unit insurance costs rose 75% in real terms, but this increase wasn’t uniform across all properties.

Buildings with documented maintenance histories, recent roof replacements, and updated electrical systems saw smaller increases than poorly maintained properties. This means your renewal premium next year depends partly on decisions you make today about building upkeep. Start collecting documentation now: photos of recent roof work, electrical panel replacements, HVAC maintenance records, and security improvements like cameras or controlled entry systems.

Competing Quotes Reveal Significant Premium Variations

When you contact carriers for quotes, your documentation becomes your negotiating advantage. Many property owners assume they’re stuck with whatever premium their current insurer quotes, but competing quotes from multiple carriers typically reveal significant premium variations for identical properties. The carrier that rates your building lowest depends on their specific appetite for your risk profile-some specialize in older buildings while others focus on newer construction.

An independent insurance agency partners with multiple carriers across California, which means you can see how different carriers price the same building risk. This competitive approach exposes the real market value of your coverage instead of accepting a single insurer’s assessment. The differences between carriers often exceed the cost of obtaining multiple quotes, making this step essential before your renewal date arrives.

What’s Actually Missing From Your Current Policy

Most apartment building owners discover coverage gaps only after filing a claim, and by then it’s too late. Standard apartment building policies systematically undercover three critical exposures that leave investors exposed to significant out-of-pocket losses.

Underinsured Property Values Create Coinsurance Penalties

The first gap appears when your property coverage limit falls below your building’s true replacement cost. Many owners base their coverage on the property’s market value or what they paid for it years ago, but replacement cost is fundamentally different. If you own a 40-unit building constructed in 1975 with original systems, the cost to rebuild it today with modern electrical, plumbing, and HVAC far exceeds what you paid for the property.

Construction and labor costs have risen dramatically alongside insurance premiums, meaning your coverage limit probably covers only a portion of actual replacement cost today. When you file a claim, insurers apply a coinsurance penalty that reduces your payout proportionally if coverage falls short. A $500,000 fire claim on a building with $3 million in actual replacement cost but only $2 million in coverage results in the insurer paying just $333,000, leaving you responsible for $167,000 out of pocket.

An updated replacement cost appraisal every two to three years prevents this penalty. Don’t accept your insurer’s suggested limits without verification-request an independent appraisal that accounts for current material and labor costs in your market.

Earthquake and Water Damage Require Separate Coverage

The second major gap involves earthquake and water damage, which California insurers either exclude entirely or limit severely in standard policies. Earthquake coverage requires a separate endorsement or policy through the California Earthquake Authority, yet most apartment owners skip this because they assume their general property coverage handles seismic damage. It doesn’t.

Water damage from burst pipes, roof leaks, or foundation cracks falls under your standard property policy, but flood damage from heavy rain or overflowing rivers does not. If your building sits in a 100-year flood zone or even a moderate-risk flood area, standard coverage leaves you exposed to total loss. Many California properties experienced significant water damage during the 2023 atmospheric river events, and owners discovered their policies covered nothing because the damage qualified as flood, not water damage.

Properties in seismic zones or flood-prone areas need both earthquake and flood coverage added to their policies. Contact your agent to determine your building’s specific exposure and obtain separate quotes for these coverages before your next renewal.

Liability Limits Fall Short for Multi-Unit Operations

The third critical gap involves liability limits that fail to match your actual exposure as a multi-unit property operator. A $300,000 general liability limit might work for a small commercial space, but a 30-unit apartment building with common areas, parking lots, pools, or fitness facilities generates substantially higher injury risk. A single serious injury claim involving a tenant, guest, or delivery person can exhaust basic liability limits within the first year of legal defense costs alone.

California’s wage and hour laws, fair housing regulations, and tenant protection ordinances create additional liability exposure that standard policies address only partially. Employment practices liability coverage protects against discrimination and wrongful termination claims and should accompany any policy for buildings with maintenance or security staff, yet many owners carry none. Try minimum liability limits of $1 million for buildings with five or more units, with umbrella coverage of $2 million or higher for added protection.

Final Thoughts

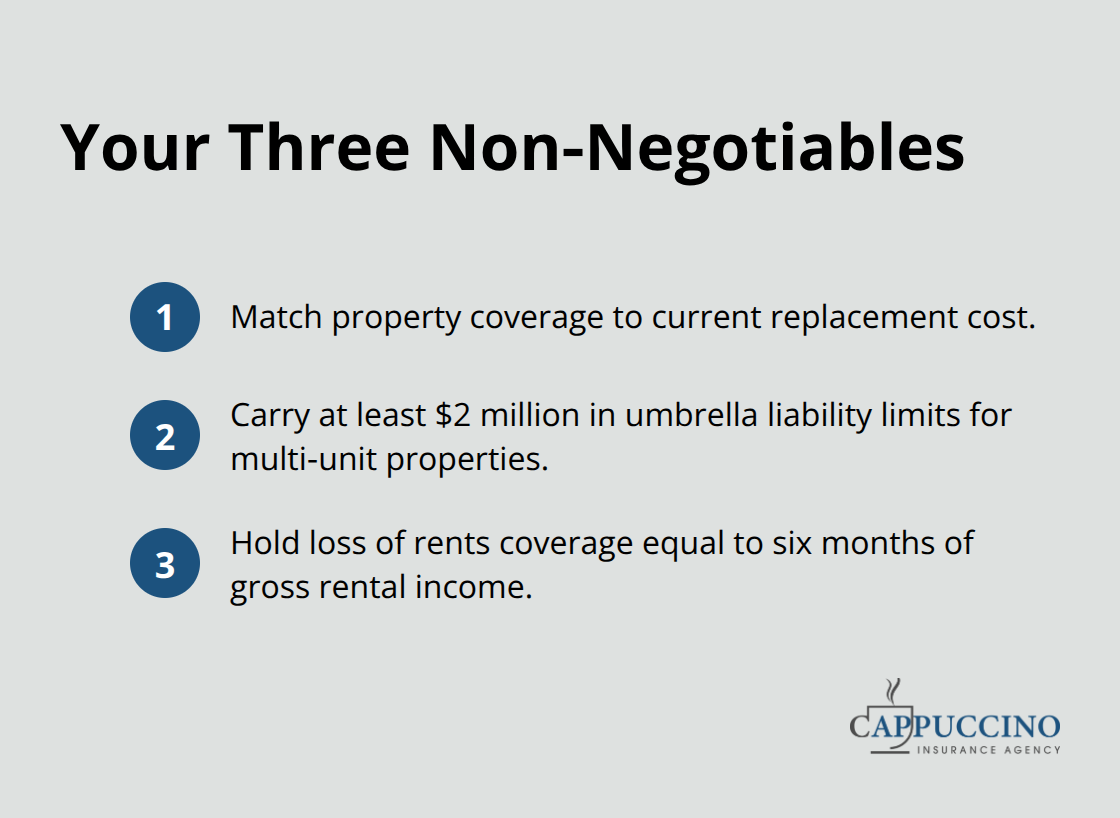

Your apartment building insurance in California requires three non-negotiable components: property coverage that matches your actual replacement cost, liability protection with umbrella limits of at least $2 million for multi-unit properties, and loss of rents coverage equal to six months of gross rental income. The 75% increase in per-unit insurance costs since 2019 makes this review urgent because your current coverage limits were likely set years ago when replacement costs were substantially lower. Without these three layers, you absorb risk that insurance exists to transfer.

Start your policy review by collecting your building’s documentation: the year constructed, square footage, recent upgrades to electrical systems, roof age, and your five-year loss history. Request this information from your current agent in writing, then contact multiple carriers to see how they rate your specific property. The variation between carriers often exceeds $5,000 annually for identical buildings, meaning competitive quotes directly impact your bottom line.

Cappuccino Insurance Agency partners with multiple carriers across California, giving you access to specialized underwriters who understand your building’s specific risk profile. A professional review typically takes two hours and costs nothing, yet it frequently reveals $3,000 to $8,000 in annual savings or identifies critical gaps that would cost far more to address after a claim. Contact your agent now to schedule a comprehensive apartment building insurance California policy review before rates increase again.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.