Property Risk Mitigation Tips for Safer Homes

Your home is one of your biggest investments, yet most homeowners underestimate the risks it faces daily. Weather, fire, theft, and other hazards can strike without warning and leave you with devastating losses.

We at Cappuccino Insurance Agency know that property risk mitigation tips work best when combined with the right insurance coverage. This guide walks you through the risks you face, the steps you can take to reduce them, and how to protect yourself with proper policies.

What Threats Put Your Home at Greatest Risk

Weather events cause the most expensive damage to U.S. homes. The National Oceanic and Atmospheric Administration reported that the United States experienced 28 billion-dollar weather disasters in 2023 alone, with hurricanes, severe storms, and flooding destroying homes and forcing costly repairs. Homeowners in wildfire-prone regions face even sharper risk-California experienced over 5,000 fires in 2023, many destroying entire neighborhoods. If you live in a coastal or fire-prone area, this is not a theoretical concern but a real threat that demands action. You need to assess your specific location’s hazard profile rather than relying on national statistics. Check your local county emergency management office or FEMA’s hazard maps to identify which disasters threaten your address most directly. Once you know your actual risks, you can prioritize your defenses and insurance coverage accordingly.

Roofs and foundations fail without regular maintenance

Roofs fail first during storms because many homeowners delay repairs until visible leaks appear. Inspect your roof annually and after heavy weather, checking for missing or curled shingles, compromised flashing around chimneys and vents, and debris-clogged gutters that trap water. Gutters backed up with leaves and twigs direct water toward your foundation instead of away from it, causing cracks that lead to basement flooding and structural rot. Foundation cracks wider than one-eighth inch warrant professional evaluation because water penetration worsens quickly and costs thousands to remediate. Trim tree branches hanging over your roof so heavy limbs cannot snap during storms and puncture your home. Standing water in landscaping or around your foundation indicates poor drainage-reroute downspouts to discharge at least six feet from your house.

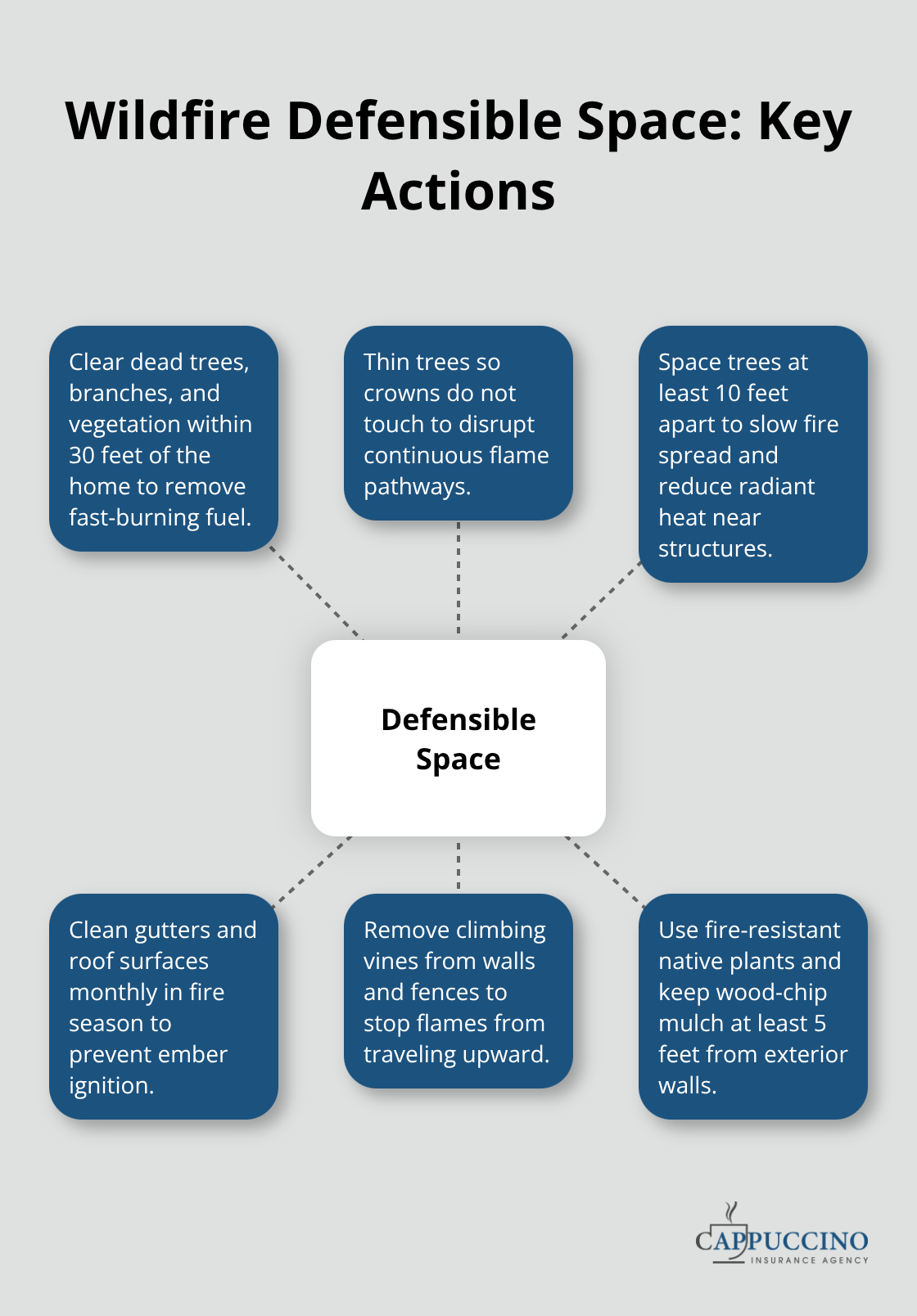

Vegetation fuels wildfire spread near your home

Defensible space stops fire from reaching your structure if you live within a mile of wildland areas. The principle is straightforward: remove dead trees, dead branches, and dead vegetation within 30 feet of your home, thin trees so crowns do not touch, and clear leaves and needles from gutters and roof surfaces monthly during fire season. Dense vegetation acts as fuel; spacing trees 10 feet apart slows fire spread significantly. Remove climbing vines from walls and fences because they carry flames upward toward your roof. Use fire-resistant plants like native shrubs with low sap and moisture content rather than ornamental junipers that ignite easily. Mulch made from wood chips retains moisture and resists ignition better than bark mulch; keep mulch at least five feet from your home’s exterior walls.

Lighting and landscaping deter burglars

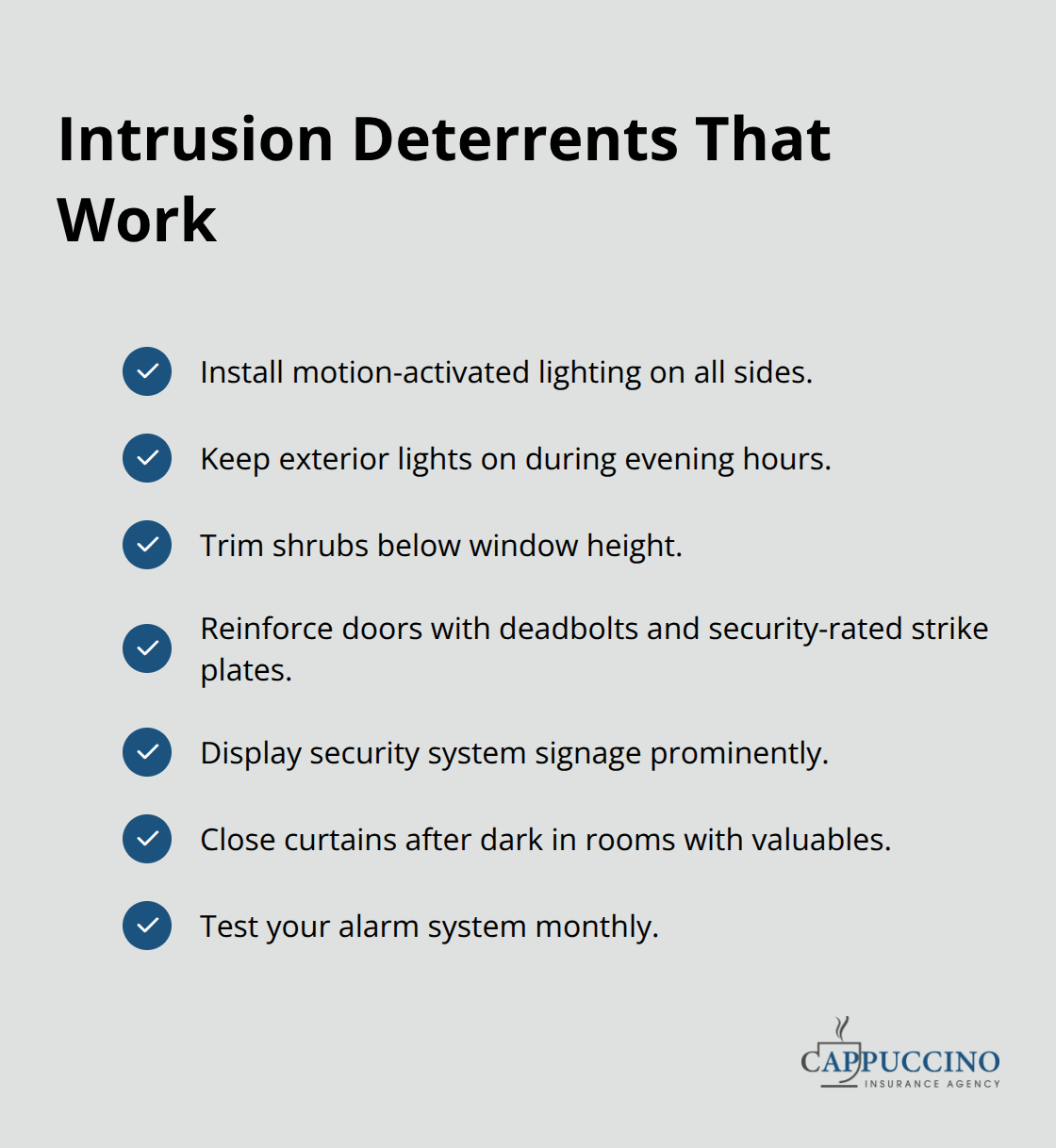

Burglars spend seconds evaluating whether entry is quick and unobserved. Dark entry points and overgrown landscaping blocking windows make your home attractive to criminals. Install motion-activated lighting on all sides of your home and keep exterior lights on during evening hours so no entrance sits in shadow. Trim shrubs below window height so intruders cannot hide while attempting entry. Doors with visible deadbolts and reinforced frames deter break-ins far more effectively than cheap locks.

Visible security system signage reduces burglary attempts (creating the perception of monitoring, even if a system is basic). Gaps in window coverings at night reveal whether you are home and what valuables sit inside-close curtains after dark in rooms with electronics or jewelry.

Your insurance coverage must match your location’s hazards

Standard homeowners policies exclude flood and earthquake damage, yet these events strike thousands of homes annually. If you live in a flood zone or earthquake-prone area, you need separate policies to avoid catastrophic financial loss. Wildfire risk presents another challenge-standard policies may exclude or limit coverage in high-risk zones. We at Cappuccino Insurance Agency specialize in hard-to-place wildfire properties across California, offering solutions like the California FAIR Plan and Difference-in-Conditions wraps that fill coverage gaps. A free coverage assessment identifies which hazards threaten your specific address and which policies you actually need rather than what insurers push as standard.

How to Protect Your Home Before Disaster Strikes

Secure Entry Points Against Intruders

Burglary happens year-round and costs the average victim $2,661 in stolen goods according to FBI crime statistics, yet motion-activated lighting cuts attempted break-ins sharply. Install lights on all sides of your home, particularly above doors and garage entrances where burglars test entry points. Reinforce exterior doors with deadbolts and strike plates rated for security use-quality hardware forces intruders to invest time and noise that attracts attention, while cheap locks fail in seconds. Visible security system signage matters more than most homeowners realize; the appearance of monitoring deters criminals faster than an alarm that only sounds after entry. Test your system monthly to confirm sensors function and backup batteries hold charge, because a silent system provides zero protection when you need it most.

Maintain Roofs and Foundations Before Water Damage Strikes

Roof and foundation maintenance prevents water damage that costs far more than routine inspections and repairs. Inspect your roof twice yearly and after storms, looking for missing shingles, cracked flashing, and debris-clogged gutters that trap water against your home. Gutters backed with leaves direct water toward your foundation instead of away from it, causing cracks that lead to flooding and structural rot costing thousands to fix. Foundation cracks wider than one-eighth inch warrant immediate professional evaluation because water penetration accelerates quickly. Trim tree branches hanging over your roof so heavy limbs cannot snap during storms and puncture your home or damage shingles. Reroute downspouts to discharge at least six feet from your house and grade landscaping so water flows away from your foundation, not toward it.

Eliminate Fire Fuel Through Vegetation Management

Wildfire preparedness demands aggressive vegetation management within 30 feet of your home if you live near wildland areas. Dead trees, dead branches, and dead vegetation act as fuel that fire spreads through rapidly; removing them stops fire progression at your property line rather than allowing it to climb toward your roof. Thin trees so crowns do not touch each other-fire spreads through touching vegetation like water flowing downhill. Space trees at least 10 feet apart to force fire to jump gaps rather than travel continuously. Clear leaves and needles from gutters and roof surfaces monthly during fire season because accumulated debris ignites easily and carries flames to your structure. Remove climbing vines from walls and fences because they carry fire upward toward your roof where it penetrates vents and ignition-prone materials. Use fire-resistant native plants with low sap and moisture content rather than ornamental junipers and similar plants that ignite at low temperatures. Wood-chip mulch resists ignition better than bark mulch because it retains moisture; keep mulch at least five feet from your home’s exterior walls.

These specific actions reduce your property loss risk substantially. The next step involves selecting insurance coverage that matches your location’s actual hazards rather than accepting generic policies that leave critical gaps unprotected.

What Insurance Coverage Your Home Actually Needs

Replacement Cost Limits Must Match Your Home’s Real Value

Standard homeowners insurance covers dwelling damage, personal property, liability, and additional living expenses, but coverage limits and exclusions matter far more than the policy name. Most policies cap dwelling coverage at replacement cost, meaning insurers pay what it costs to rebuild your home today, not what you paid for it years ago. If your home would cost $450,000 to rebuild but your policy limits sit at $350,000, you absorb the $100,000 gap out of pocket. A replacement cost estimate from a contractor reveals what your home actually costs to rebuild before you select coverage limits, preventing underinsurance that leaves you financially devastated after total loss.

Personal Property Coverage Leaves High-Value Items Exposed

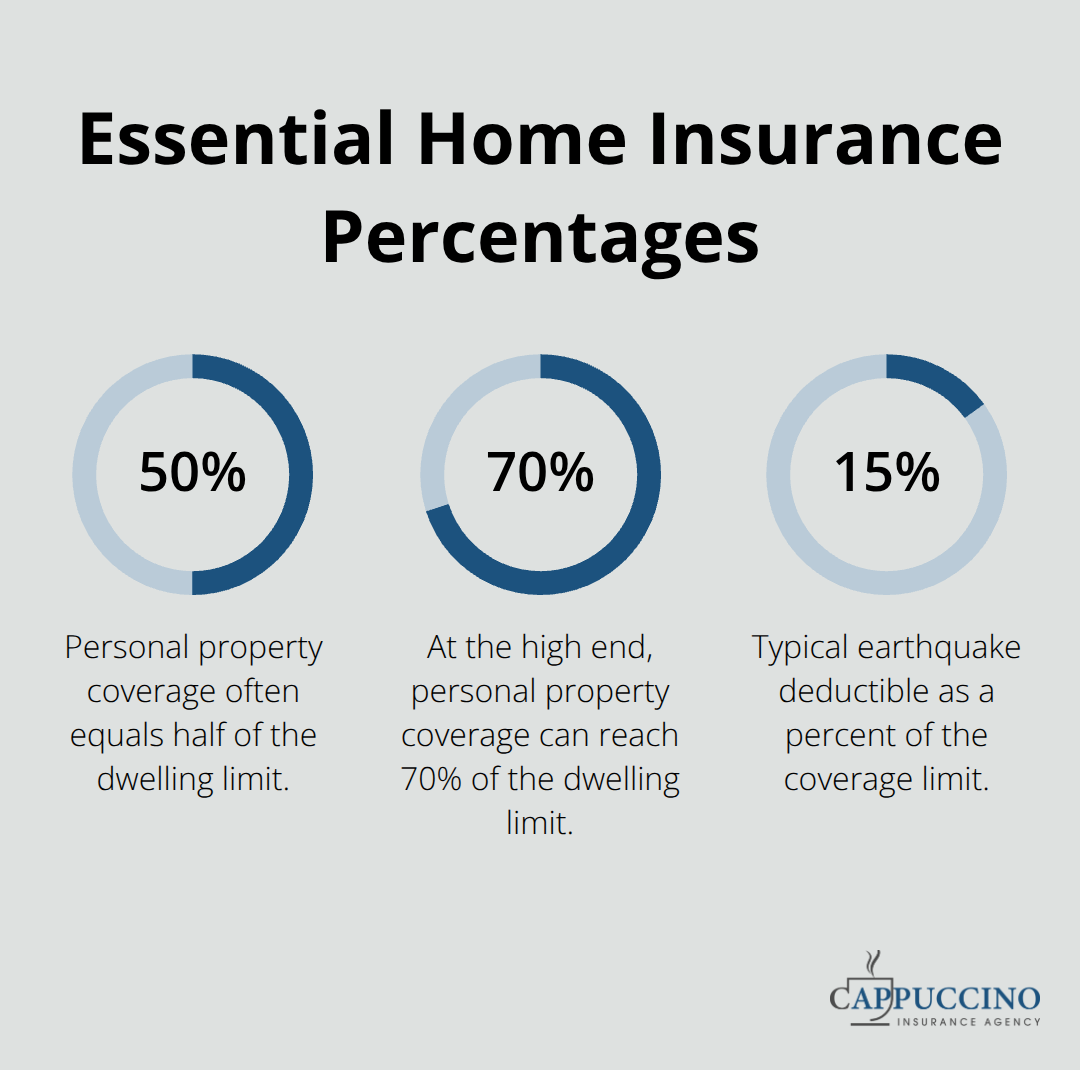

Personal property coverage typically maxes out at 50-70% of your dwelling limit, which sounds reasonable until you inventory your actual possessions and realize clothes, electronics, furniture, and kitchen items add up far faster than expected. High-value items like jewelry, art, and collectibles hit sub-limits of $1,000-$2,500 per item, forcing you to purchase scheduled personal property riders if you own anything valuable. This gap between standard coverage and what you actually own creates a false sense of protection that evaporates when loss occurs.

Liability Coverage Needs Umbrella Protection for Serious Injuries

Liability coverage protects you if someone is injured on your property and sues, yet most policies start at $100,000-$300,000 limits that evaporate instantly in serious injury cases where medical costs and lost wages exceed $500,000. Umbrella policies costing $150-$300 annually for $1 million in additional liability coverage are inexpensive relative to the financial destruction a major lawsuit creates. This additional layer of protection costs far less than the risk it eliminates.

Flood and Earthquake Coverage Require Separate Policies

Standard policies exclude flood and earthquake damage entirely, a reality that catches homeowners off-guard when disaster strikes. Flood insurance requires a 30-day waiting period before coverage activates, meaning you cannot buy it after storm warnings appear. If you live in a designated flood zone, your mortgage lender mandates flood insurance anyway, so obtaining it voluntarily before lender requirements apply gives you time to shop rates across multiple carriers.

Earthquake coverage runs $300-$600 annually depending on your home’s construction and location, with deductibles typically set at 15-20% of the coverage limit rather than fixed dollar amounts, meaning a $300,000 home with 15% deductible requires you to absorb $45,000 in losses before insurance pays anything.

Wildfire Risk Demands Specialized Coverage Solutions

Wildfire risk presents the most complex coverage challenge in California because standard carriers are withdrawing from high-risk zones and raising rates dramatically for properties within one mile of wildland. The California FAIR Plan provides a last-resort option for wildfire-prone properties that cannot obtain coverage elsewhere, but FAIR Plan policies cost 40-60% more than standard market rates and offer narrower coverage. Difference-in-Conditions wraps fill the gaps that FAIR Plan policies leave exposed, protecting your home against losses standard policies exclude. Annual policy reviews catch coverage gaps before disaster exposes them, yet most homeowners never review their policies unless they purchase a new home or switch insurers. Cappuccino Insurance Agency partners with 20+ carriers to deliver specialty solutions for hard-to-place wildfire-risk properties across California, including the California FAIR Plan and Difference-in-Conditions wraps, plus free coverage assessments that identify which hazards threaten your specific address and which policies actually protect you.

Conclusion

Property risk mitigation tips only work when paired with accurate insurance coverage that matches your home’s actual hazards. The steps you take to secure entry points, maintain your roof, and eliminate fire fuel reduce loss probability significantly, but they cannot prevent every disaster. Insurance fills the gap between what you can prevent and what strikes despite your best efforts.

Professional assessments reveal coverage gaps that standard policies hide. Most homeowners discover these gaps only after loss occurs, when it’s too late to add protection. A contractor’s replacement cost estimate shows whether your dwelling limits match what rebuilding actually costs, while a hazard assessment identifies which disasters threaten your specific address rather than relying on national statistics that may not apply to your location.

We at Cappuccino Insurance Agency provide free coverage assessments that identify which hazards threaten your address and which policies actually protect you. Our team partners with multiple carriers to deliver specialty solutions for hard-to-place wildfire-risk properties across California, including the California FAIR Plan and Difference-in-Conditions wraps that fill coverage gaps standard policies leave exposed. Schedule a free assessment to confirm your coverage matches your home’s real risks.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.