California Homeowners Risk Assessment: Pinpointing Vulnerabilities

California homeowners face real threats from wildfires, earthquakes, and flooding. Many property owners don’t realize how vulnerable their homes actually are until disaster strikes.

At Cappuccino Insurance Agency, we help homeowners identify these risks before they become costly problems. This guide walks you through a practical California homeowners risk assessment so you can protect what matters most.

What Makes California Homes Most Vulnerable

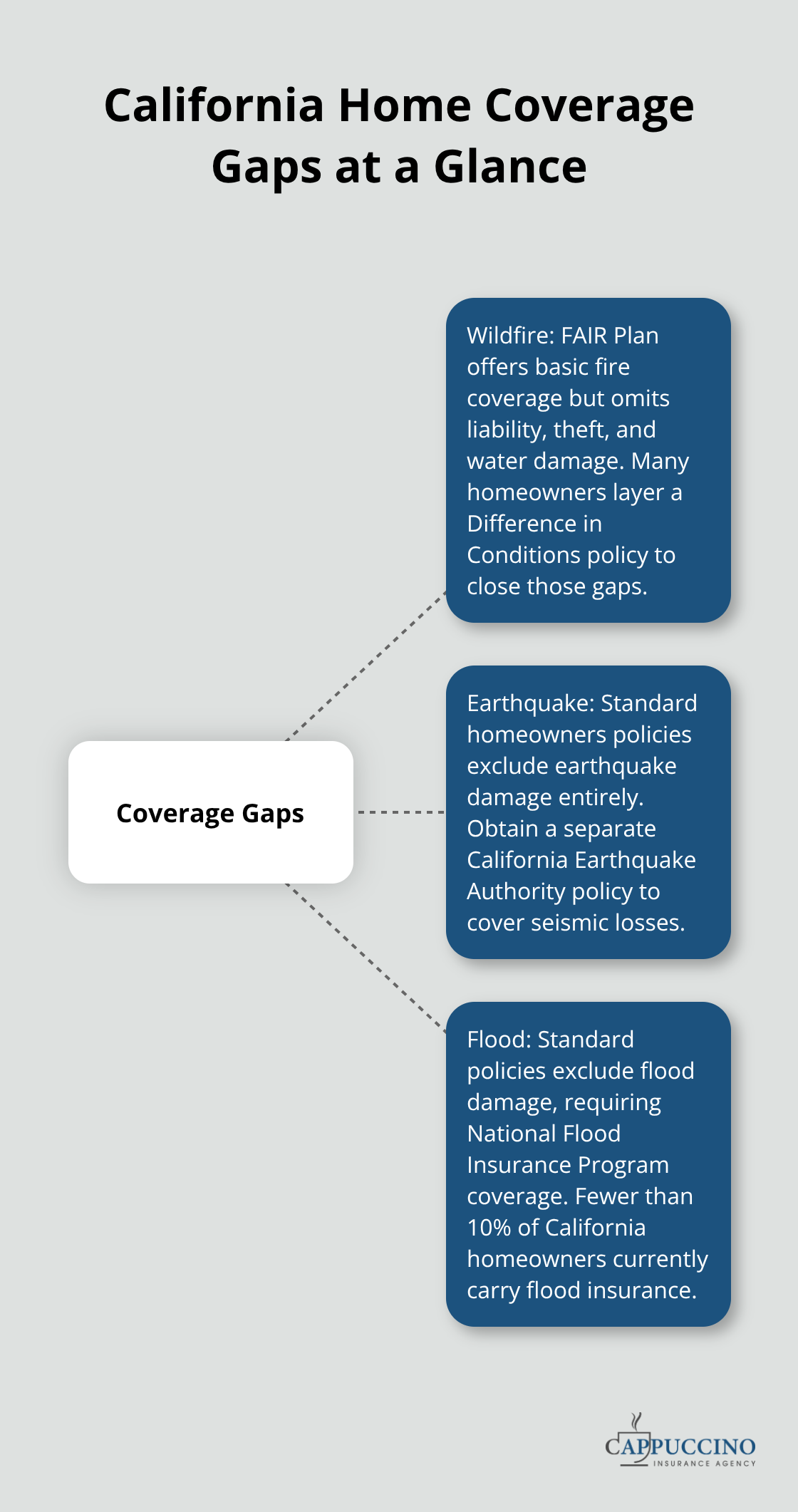

Wildfire risk dominates the California insurance landscape, and location determines everything. About 1.3 million properties sit in high or extreme wildfire zones, which explains why major carriers have pulled out of entire regions. Your home’s wildland-urban interface score-calculated from vegetation density, slope, topography, and emergency access-directly impacts your insurability and premium. Northern California’s Sierra Nevada foothills, wine country, and coastal mountains face the steepest challenges, with many homeowners pushed toward the California FAIR Plan, which now covers over 370,000 policies statewide. The FAIR Plan provides basic fire coverage but leaves you exposed on liability, theft, and water damage, forcing many to layer a Difference in Conditions policy on top just to get reasonable protection. Southern California’s hillside communities face similar pressures, with non-renewals concentrated in wildfire-exposed areas. This isn’t about individual home quality-it’s a systemic market shift driven by catastrophic loss patterns.

Older construction invites ember intrusion

Homes built before 2015 often lack modern wildfire construction standards, especially vulnerable roofs and inadequate ember-resistant vents. Roofing older than 10 years dramatically increases ember intrusion risk, since aging materials allow embers to ignite attic contents. Vinyl gutters need replacement with metal, and attic vents require 1/16-inch mesh or State Fire Marshal-listed ember-resistant alternatives to block ember entry. Wood siding, deck boards, and attached combustible structures create continuous fuel paths that fire can follow into your home.

Earthquake damage remains uninsured

Earthquakes add another layer of risk-older foundations without proper bracing, unreinforced masonry, and soft-story construction (common in multi-story homes) fail first when shaking begins. Standard homeowners policies exclude earthquake damage entirely, so you need separate California Earthquake Authority coverage, which most homeowners skip or underbuy.

Flood insurance gaps leave you exposed

Water damage from flooding and storms isn’t covered by standard policies either, requiring National Flood Insurance Program coverage. Fewer than 10% of California homeowners carry flood insurance despite living in flood-prone zones. These three coverage gaps-wildfire, earthquake, and flood-create a dangerous protection void that forces homeowners to patch together multiple policies or face catastrophic financial loss. Understanding what your current policy actually covers is the first step toward closing these gaps and securing real protection.

Assess Your Home’s Actual Risk Before Disaster Hits

Document Your Roof and Exterior Condition

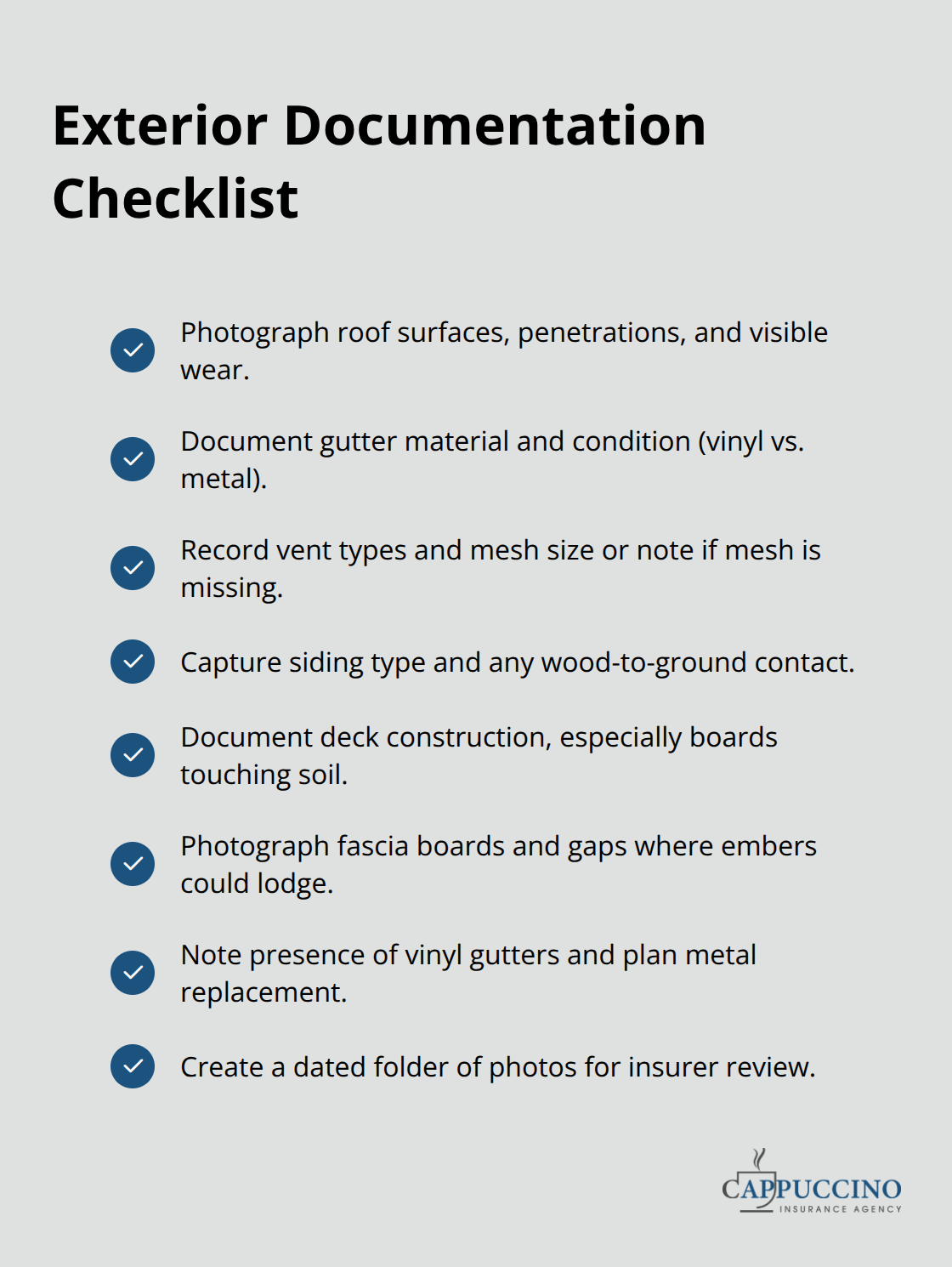

Start with your roof and exterior because these elements face the most immediate wildfire threat. Walk around your property with a camera and photograph every surface-roof condition, gutter material, vent type, siding, deck construction, and attached structures. Capture close-up images of roof penetrations, fascia boards, and gaps around attachments where embers lodge. If your roof is older than 10 years, photograph the shingles to show aging, curling, or missing pieces. Check whether your gutters are vinyl (they need metal replacement) or already metal. Examine your attic and foundation vents and measure the mesh size if visible, or note if vents lack mesh entirely.

Vinyl or screen mesh won’t stop embers; you need 1/16-inch metal mesh or State Fire Marshal-listed ember-resistant vents. Document wood siding, wood fencing within five feet of the house, wood mulch or bark in landscaping, and any deck boards touching the ground. These details establish a baseline for what needs upgrading and provide insurers with concrete evidence of your property’s current condition.

Take the Cal Fire Self-Assessment

Complete the Cal Fire Home Hardening Self-Assessment, which takes under 10 minutes and delivers a tailored report showing exactly which vulnerabilities your home has. This assessment identifies specific weaknesses tied to your property’s construction and location, giving you a prioritized list of upgrades that matter most for your situation.

Evaluate Your Foundation and Structural Systems

Look for cracks in concrete, signs of settling, or visible water damage in basements or crawl spaces. Older homes built before 1980 often lack proper foundation bolting or bracing, especially if you live in an earthquake zone. A full structural assessment requires a licensed engineer or contractor, not a DIY inspection. This professional evaluation reveals whether your foundation meets current seismic standards and identifies any structural vulnerabilities that affect your insurability and long-term safety.

Audit Your Current Insurance Coverage

Pull out your current homeowners policy and read the declarations page carefully. Note your dwelling coverage limit, deductible, and what’s actually excluded. Standard policies exclude earthquake damage and flood damage completely. If you carry FAIR Plan coverage, you have only basic fire protection with no liability, theft, or water damage. If you’ve layered a Difference in Conditions policy on top, you’re managing two separate policies with two different insurers, which creates gaps if claims overlap. This audit reveals whether your dwelling limit matches your home’s rebuild cost (many homeowners are underinsured), whether you need earthquake coverage through the California Earthquake Authority, and whether flood insurance through the National Flood Insurance Program applies to your property.

Close Your Coverage Gaps

These three steps-photographing vulnerabilities, documenting structural concerns, and reviewing actual policy language-give you the information needed to prioritize mitigation spending and close coverage gaps before the next fire season. With this assessment complete, you’re ready to move forward with specific mitigation actions that reduce your home’s exposure and strengthen your insurance position.

How to Reduce Your Home’s Wildfire Risk Right Now

Eliminate Fuel Pathways in Zone 0

Zone 0-the five feet immediately surrounding your home-is where embers collect and ignition begins. Replace wood mulch, decorative bark, and wood fencing in this zone with gravel, pavers, or metal fencing sections immediately. According to Cal Fire guidance, this single action breaks the fuel path that fire uses to reach your structure. Metal gutter guards prevent pine needles and leaves from accumulating, and you should clean gutters before red-flag events rather than waiting for spring. Vinyl gutters must be replaced with metal, and any deck boards touching soil need to become noncombustible or removed entirely.

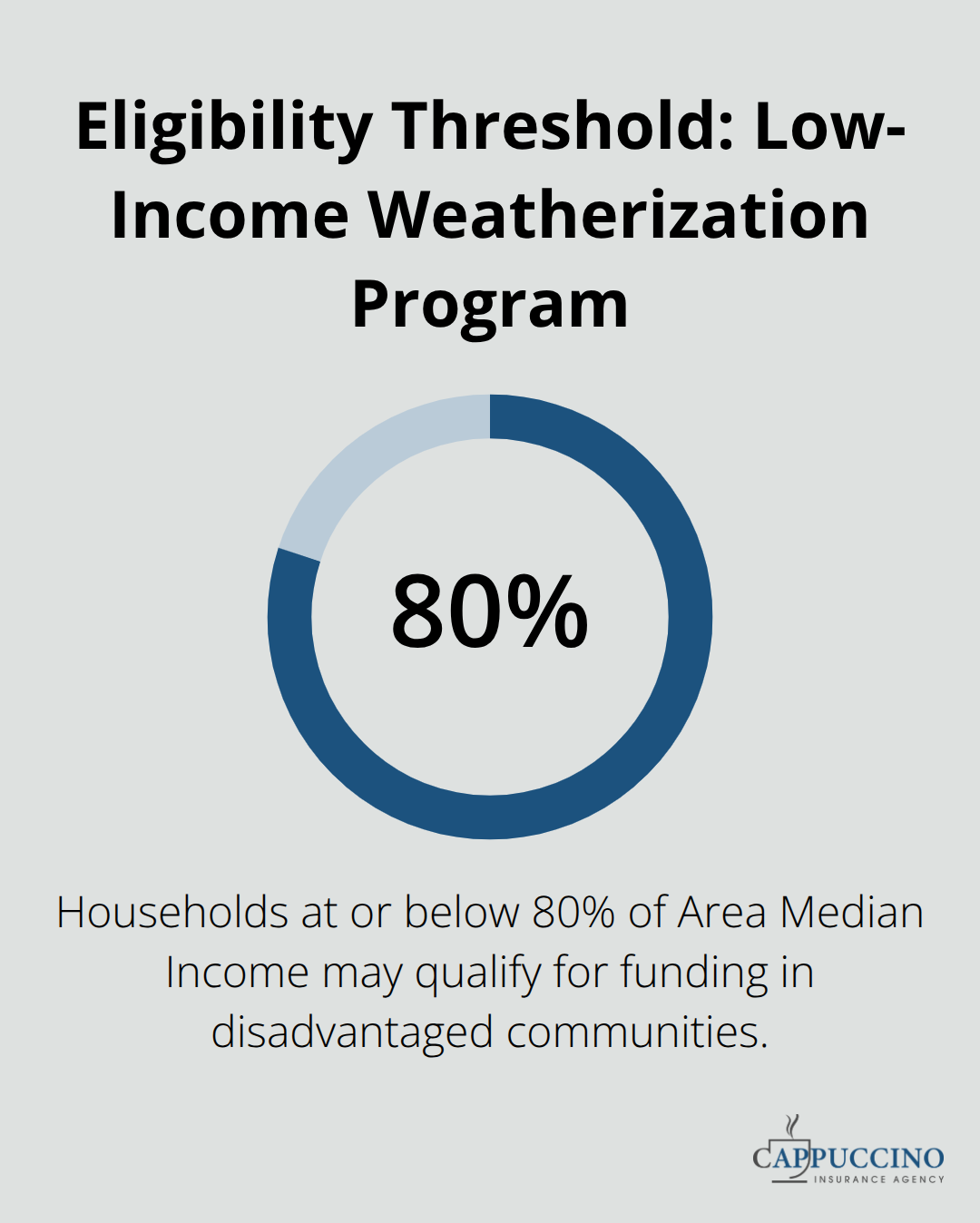

If your home has a detached structure within 10 feet-a shed, gazebo, or carport-establish the same noncombustible barrier around it. These upgrades cost far less than retrofitting your roof or siding, yet they eliminate the most common ember entry pathways. The California Low-Income Weatherization Program provides funding for eligible households earning 80% or less of the Area Median Income in disadvantaged communities, though wildfire hardening falls outside traditional weatherization scope. Prioritize Zone 0 work first because it delivers the fastest risk reduction and lowest cost per improvement.

Upgrade Roofs and Vents to Block Embers

Roof and vent upgrades are non-negotiable if your home is older than 2015. Class A-rated roof coverings-asphalt shingles, tile, cement shingles, or metal-are required by California building code and should be your standard. If your roof exceeds 10 years old, replacement cannot wait; aging materials fail to block embers. Attic and underfloor vents must have 1/16-inch to 1/8-inch metal mesh or State Fire Marshal-listed ember-resistant alternatives; standard screen mesh fails immediately. Install metal drip edges above gutters to prevent embers from entering behind the gutter system.

Harden Siding, Windows, and Doors

For exterior siding, replace combustible materials with noncombustible or ignition-resistant options; if full replacement isn’t feasible, cover the bottom 2 feet with noncombustible siding and add metal flashing with gaps no larger than 1/8 inch. Double-pane tempered glass windows with metal framing perform better than single-pane, and metal mesh window screens add radiant-heat protection. These structural upgrades typically cost 5,000 to 15,000 dollars depending on your home’s size and current condition, but they transform your home from a wildfire liability into a defensible structure.

Work With Professionals and Document Improvements

Schedule professional assessments rather than attempting complex retrofits yourself; always consult a licensed contractor and your local building official to ensure compliance and address ventilation implications that DIY work often overlooks. Verified mitigation can unlock eligibility and potential premium discounts as carriers adopt credit-based programs. Document these improvements with photos and contractor reports so you have concrete evidence when discussing coverage options with your insurer.

Final Thoughts

California homeowners face three interconnected threats: wildfire exposure tied to location and construction age, earthquake damage excluded from standard policies, and flood risk left uninsured by most carriers. A California homeowners risk assessment reveals these vulnerabilities before they become financial disasters. Your roof condition, vent type, exterior materials, foundation integrity, and current coverage gaps determine whether your home can survive the next fire season or whether you face catastrophic loss.

Homes change over time, and so does their risk profile. A roof replacement, major remodel, or significant landscaping work shifts your property’s vulnerability. Repeat assessments every three to five years, or immediately after major upgrades, to track progress and catch new exposures. This ongoing evaluation keeps your mitigation efforts aligned with your actual risk and helps you qualify for premium discounts as carriers adopt credit-based programs for verified improvements.

We at Cappuccino Insurance Agency partner with multiple carriers to help California homeowners secure the coverage they need for wildfire-exposed properties, including FAIR Plan and Difference-in-Conditions solutions. Our free coverage assessment identifies gaps in your current protection, and our annual policy reviews ensure you’re not overpaying for redundant coverage or missing essential protections.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.