California FAIR Plan Coverage: What Homeowners Need to Know

Finding homeowners insurance in California has become harder than ever. If standard insurers have rejected your application, the California FAIR Plan coverage might be your answer.

We at Cappuccino Insurance Agency help homeowners navigate this complex landscape. This guide walks you through what the FAIR Plan covers, how to apply, and how to fill the gaps it leaves behind.

What the California FAIR Plan Actually Is

The FAIR Plan Is Not Government-Backed

The California FAIR Plan is not a government program, despite what many homeowners assume. A private association overseen by the California Department of Insurance funds it entirely through private insurance companies operating in the state. When standard insurers reject your application due to wildfire risk or other factors, the FAIR Plan serves as your last resort for basic property coverage. As of March 2026, the plan covered 684,388 policies with a total exposure of $750 billion, reflecting significant growth in recent years. This explosive growth reflects a harsh reality: California’s insurance market is contracting, and more homeowners face rejection from standard policies each year.

What Coverage the FAIR Plan Provides

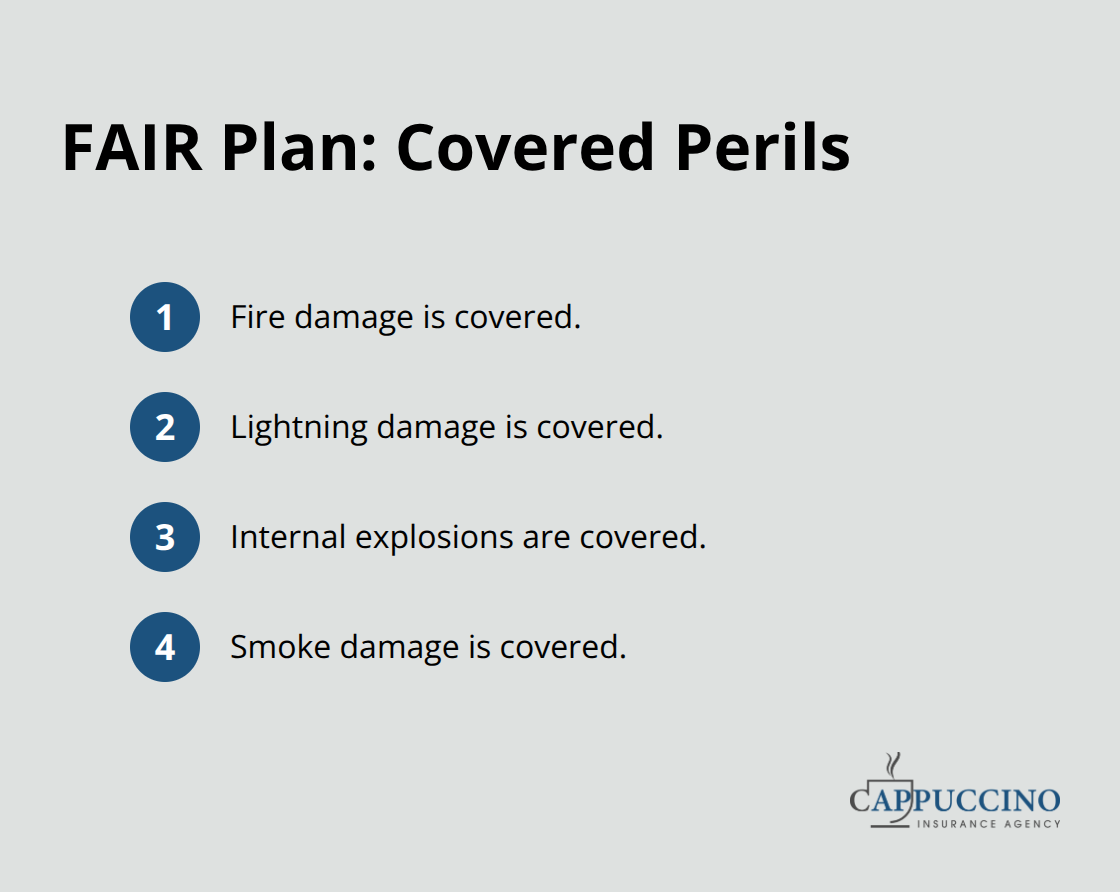

A basic FAIR Plan policy covers only four perils-fire, lightning, internal explosions, and smoke-against your dwelling and personal property on an actual cash value basis. Actual cash value means you receive what your items were worth at the time of loss, not what it costs to replace them today.

The plan caps residential dwelling coverage at $3 million per location. The average FAIR Plan premium runs about $3,200 per year, according to recent market data, which is significantly higher than a typical California standard policy at roughly $1,429 for $300,000 in dwelling coverage. You pay more for less protection, which is why treating the FAIR Plan as a temporary solution-not a permanent answer-matters.

The Critical Coverage Gaps

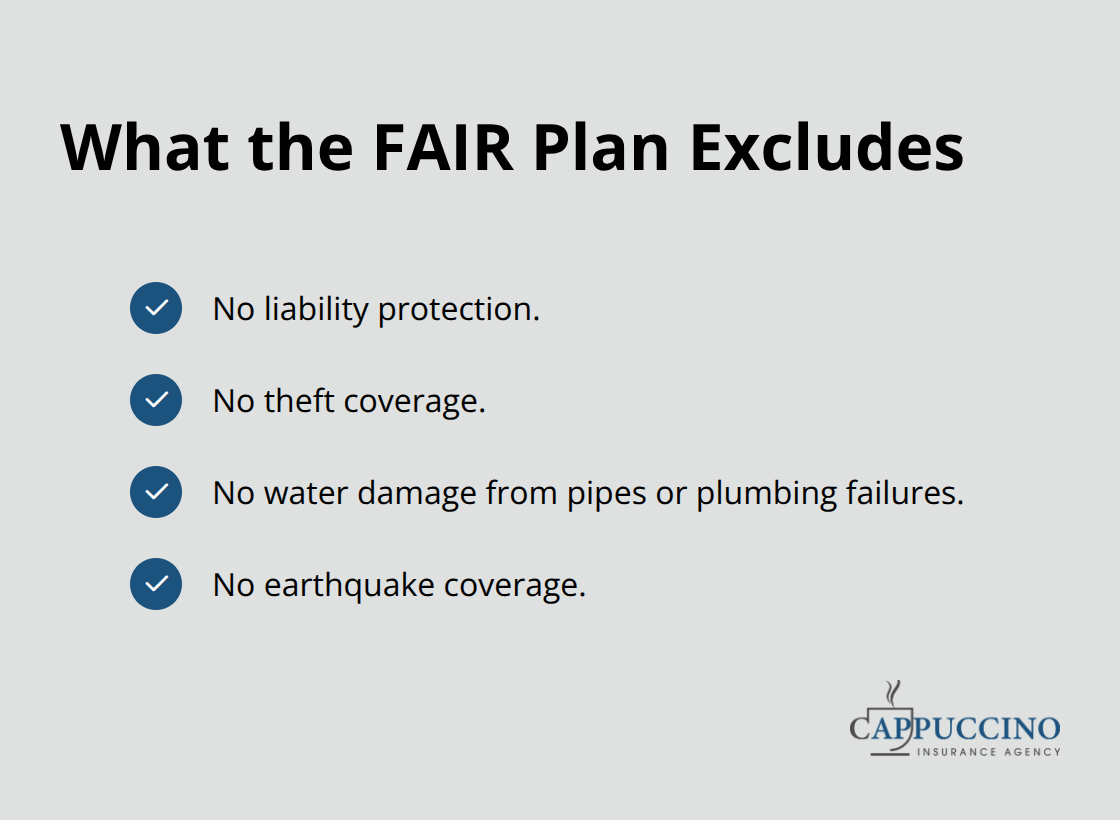

The FAIR Plan excludes liability protection, theft coverage, water damage, and earthquake protection. These gaps are massive. If someone is injured on your property, your FAIR Plan policy won’t defend you. If a pipe bursts and floods your basement, you pay out of pocket. If an earthquake hits, the FAIR Plan won’t cover a single dollar of damage. This differs fundamentally from a standard homeowners policy, which typically bundles liability, theft, water damage, and additional living expenses into one comprehensive package.

Who Qualifies for FAIR Plan Coverage

Eligibility requires that you’ve genuinely pursued private coverage first. You cannot simply walk into the FAIR Plan; you must demonstrate that standard insurers have denied you. Owner-occupied homes, condos, rental properties, and even seasonal homes qualify, but vacant properties (more than 50% unoccupied), homes with unrepaired damage, and properties linked to illegal activity do not.

How to Start the Application Process

A licensed insurance broker registered with the FAIR Plan provides the practical path forward. Brokers perform a diligent market search on your behalf at no additional cost to you and handle the application process. This initial step-working with a broker to verify your eligibility and gather required documentation-sets the foundation for moving forward with your FAIR Plan application.

Coverage Limits and Exclusions Under the California FAIR Plan

What the FAIR Plan Actually Covers

The FAIR Plan’s four-peril structure covers fire, lightning, internal explosions, and smoke damage against your dwelling and personal property on an actual cash value basis. If your five-year-old roof burns in a wildfire, you don’t receive $15,000 to replace it with new materials-you receive what that roof was worth after five years of depreciation, typically $8,000 to $10,000. The gap between actual cash value and replacement cost forces homeowners into a painful choice: accept underinsurance or purchase costly endorsements. Dwelling replacement cost coverage exists as an optional add-on, but it increases your premium substantially.

Coverage Limits That Fall Short

The FAIR Plan caps residential coverage at $3 million per location as of 2026, a significant increase from the previous $1.5 million limit, yet this ceiling still falls short for many high-value properties in coastal California communities. The average FAIR Plan premium of $3,200 annually already feels punitive compared to standard homeowners policies at roughly $1,429 for equivalent dwelling limits. Adding replacement cost endorsements pushes that figure higher, making the FAIR Plan increasingly expensive relative to what it actually covers.

Major Exclusions You Cannot Ignore

Liability protection, theft, water damage from pipes or plumbing failures, and earthquake coverage all fall outside the standard FAIR Plan policy. This matters because California homeowners face water damage claims at rates comparable to or exceeding fire claims in many years. If a burst pipe floods your home, the FAIR Plan pays nothing. If someone slips on your driveway and sues you for $250,000 in medical expenses, the FAIR Plan offers zero defense.

Wildfire Risk and Coverage Contradictions

Wildfire risk influences your coverage options in a counterintuitive way. Properties in high-risk wildfire zones face steeper FAIR Plan premiums, yet the Plan’s four-peril structure actually excludes coverage for some wildfire-related damage. Smoke damage is covered, but only if fire reaches your property; pre-fire smoke damage from distant fires falls into a gray area that has sparked litigation. A July 2024 class-action lawsuit in Alameda County alleged the FAIR Plan refused to investigate and pay smoke damage claims from wildfires that never directly threatened the insured properties. The outcome remains unresolved, but the dispute highlights how wildfire risk concentrates exposure in areas where the FAIR Plan’s protection proves most limited.

Why Supplemental Coverage Becomes Essential

Homeowners in high-risk zones should not assume the FAIR Plan fully protects them against wildfire consequences. The gaps in coverage-particularly the absence of liability protection and water damage coverage-create significant financial exposure that extends far beyond fire risk alone. These exclusions set the stage for understanding how additional insurance layers can address what the FAIR Plan leaves unprotected.

How to Apply for California FAIR Plan Coverage

Find a Licensed Broker to Start Your Application

Your path to FAIR Plan coverage runs through a licensed broker registered with the California FAIR Plan, not through direct contact with the Plan itself. Brokers conduct the market search that proves your eligibility-they shop the standard insurance market on your behalf and document every denial you’ve received or would receive from private carriers. This step matters because the FAIR Plan requires evidence that you’ve genuinely pursued private coverage first. The California Department of Insurance maintains a Broker Finder tool to locate registered brokers in your area, and using a broker costs you nothing extra since their services are provided at no additional charge.

Prepare Your Property Information

When you contact a broker, bring information about your property: its age, condition, distance to the nearest fire station, your claims history, and the specific reason standard insurers rejected you. This documentation accelerates the eligibility verification process. The broker will typically request a home inspection to assess property conditions and wildfire hardening measures, which can influence your premium. If you’ve already received written denials from private insurers, bring those letters-they strengthen your application and reduce the time brokers spend on market searches. The entire broker-led verification process usually takes two to four weeks, though complex cases involving properties with damage or maintenance issues may extend this timeline.

Submit Your Application and Receive Approval

Once your broker confirms eligibility and completes the market search, the formal application submission begins. Your broker submits the FAIR Plan application with documentation proving you meet residency and property-use requirements-that your home is owner-occupied, a rental property, a condo, or a seasonal residence, and that it hasn’t been vacant for more than 50 percent of the preceding 12 months. The FAIR Plan typically issues a decision within 30 to 60 days of receiving a complete application, according to the California Department of Insurance. After approval, your policy activates within days, providing immediate coverage once you pay the initial premium.

Choose Your Payment Options and Coverage Endorsements

Payment flexibility has improved: as of 2026, the FAIR Plan allows monthly payments without fees, though credit card payments incur a processing fee that covers transaction costs only. Some homeowners ask whether they should request the optional dwelling replacement cost endorsement during application-the answer depends on your property value and financial capacity to absorb depreciation losses. A $500,000 home on actual cash value leaves significant exposure; adding replacement cost coverage increases your premium by roughly 15 to 25 percent but eliminates depreciation penalties. The broker can provide exact premium comparisons for your specific property before you commit.

Plan Your Next Steps After Policy Activation

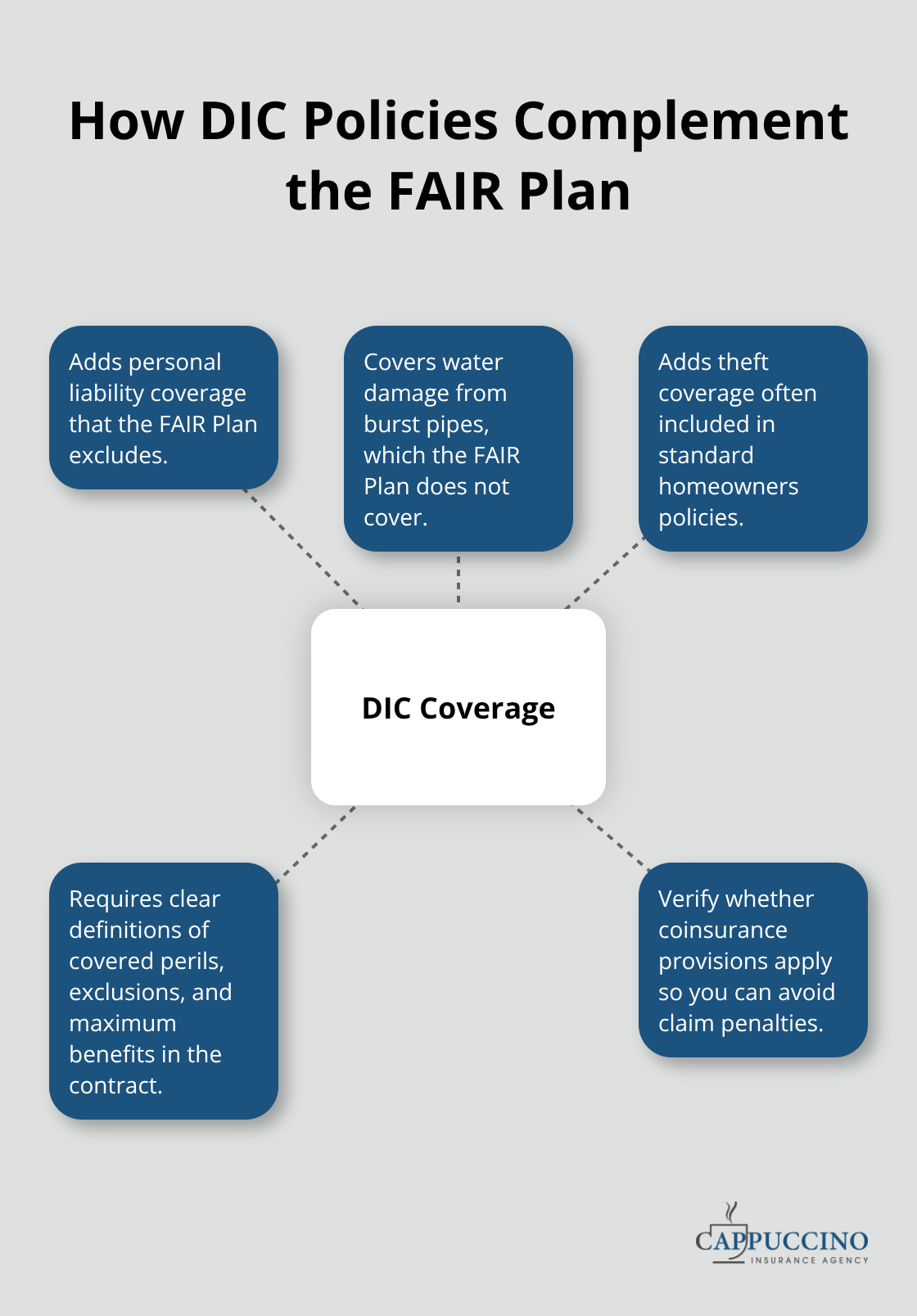

Once your policy activates, contact your broker within 30 days to discuss supplemental coverage options, particularly Difference-in-Conditions policies that address the FAIR Plan’s liability and water damage gaps.

Wrapping Up

The FAIR Plan provides essential coverage when standard insurers won’t, but it deliberately leaves gaps in liability, theft, water damage, and earthquake protection. A basic policy covers only fire, lightning, internal explosions, and smoke on an actual cash value basis-meaning you absorb depreciation losses that a standard homeowners policy would cover. Difference-in-Conditions policies bridge these gaps by layering additional protection on top of your California FAIR Plan coverage, adding perils like theft, water damage from burst pipes, and personal liability that the FAIR Plan excludes entirely.

When you pair a DIC policy with your FAIR Plan coverage, the FAIR Plan handles fire-related perils while the DIC policy covers the everyday risks that standard homeowners policies address. The California Department of Insurance maintains a list of insurers selling DIC policies, but shopping independently or through a broker yields better results than relying on a single salesperson. Your DIC contract should clearly define covered perils, exclusions, maximum benefits, and premium amounts, and you should verify that coinsurance provisions don’t apply to your coverage or that you meet any stated requirements to avoid claim penalties.

After your policy activates, reassess your total protection within 30 days and calculate your potential losses from liability claims, water damage, and theft against what your coverage actually protects. The gap between your exposure and your coverage determines whether a DIC policy makes financial sense for your situation. We at Cappuccino Insurance Agency help homeowners in high-risk areas build complete insurance strategies that combine FAIR Plan coverage with supplemental protection tailored to your property and budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.