Homeowner Coverage California: Ensuring Adequate Protection And Value

California homeowners often buy insurance without understanding what they actually need. The gap between what you have and what protects you can be expensive.

We at Cappuccino Insurance Agency help homeowners navigate homeowner coverage in California to avoid costly mistakes. This guide shows you what coverage matters, where gaps hide, and how to get real value from your policy.

What California Actually Requires You to Carry

California doesn’t mandate homeowner insurance by state law, but your mortgage lender absolutely will. If you borrowed money to buy your home, your lender requires dwelling coverage (the structure itself) and typically asks for liability protection as well. The California Department of Insurance sets no minimum coverage amounts for owner-occupied homes, which means you and your lender negotiate what’s adequate.

Lender Requirements Fall Short of Reality

Most lenders demand dwelling coverage equal to at least the loan amount, though this often falls short of what you actually need to rebuild. Construction costs in California run significantly higher than the national average, and rebuilding your home after a total loss costs far more than your purchase price. The Terner Center found that California’s median home insurance cost was about $1,200 per year in 2023, but this varies dramatically by property type and location. Mobile homes carry the highest per-dollar cost at roughly $483 per $100,000 of covered value, while single-family homes average around $182 per $100,000. Dwelling-fire policies, common in high-risk areas, jumped from about $150 to $230 per $100,000 between 2018 and 2021, reflecting the state’s wildfire exposure. Your mortgage lender’s minimum requirement protects their investment, not yours.

Standard Policies Leave Critical Gaps

Standard homeowner policies include dwelling coverage, other structures (typically 10% of your dwelling limit), personal property (usually 50% to 70% of dwelling coverage), liability, and additional living expenses. The California Department of Insurance emphasizes that personal property has sub-limits for jewelry, fine arts, and collectibles, meaning scheduled items often need separate endorsements to avoid severe underinsurance. A $500,000 dwelling limit might sound adequate, but if your home requires $750,000 to rebuild due to current labor and material costs, you’re underinsured by a quarter million dollars.

Excluded Perils You Must Address Separately

Earthquake damage isn’t covered by standard policies in California, and neither is flood damage unless you purchase separate coverage through the California Earthquake Authority or the National Flood Insurance Program. NFIP flood coverage maxes out at $250,000 for the structure and $100,000 for contents on single-family homes, which many California properties exceed. From 2018 to 2021, fire-related losses accounted for roughly 42% of all premiums paid in California, according to the California Department of Insurance, yet many homeowners carry inadequate fire coverage limits.

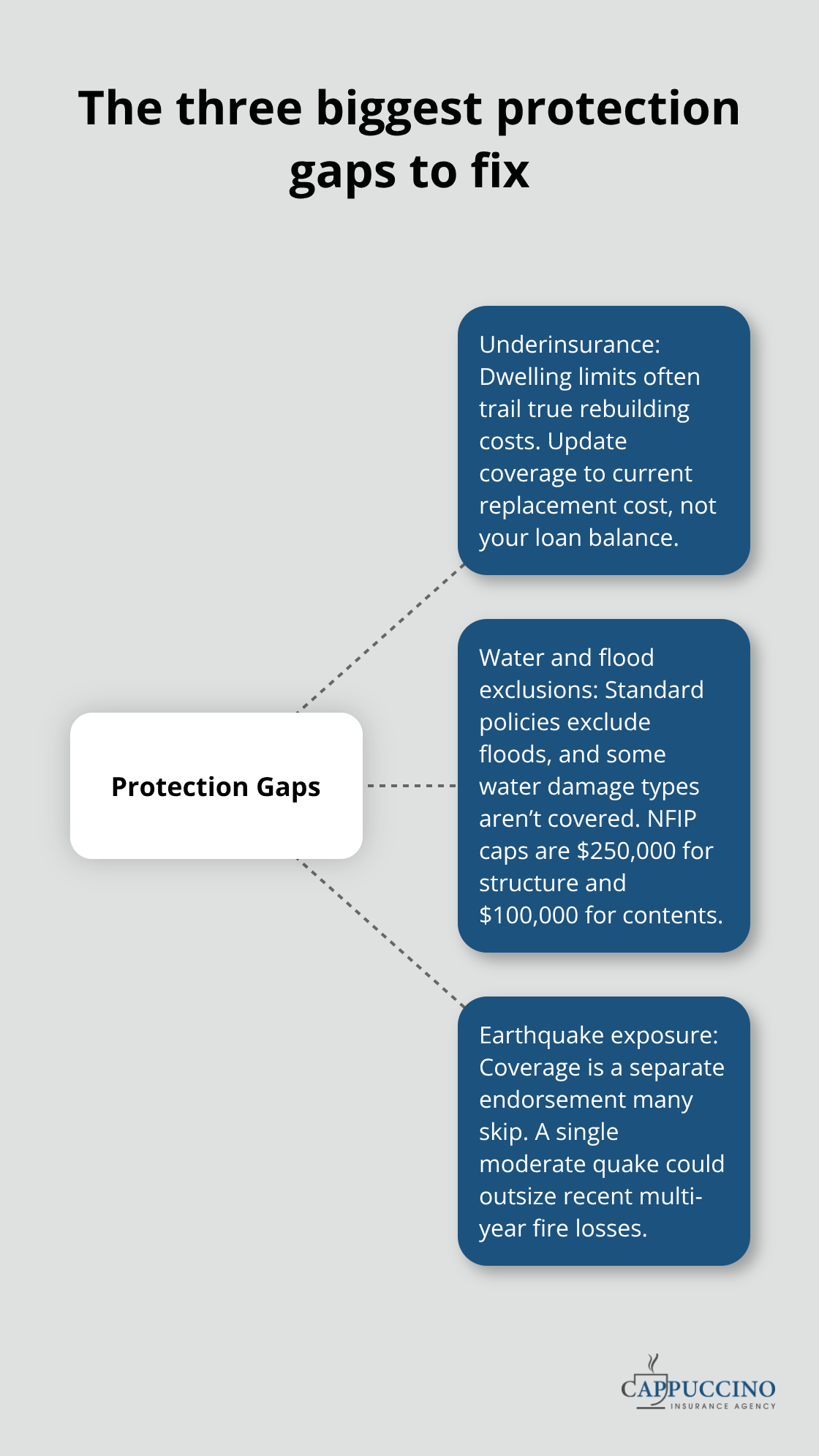

The Protection Gap Matters More Than You Think

Your lender’s requirement protects their claim against your property-you need additional coverage that protects your ability to rebuild your life. This distinction shapes everything about how you should structure your policy and what conversations you need to have with your insurance professional. Understanding where lender requirements end and your actual protection begins reveals why so many California homeowners face financial devastation after a covered loss.

Where Your Coverage Actually Fails

Underinsurance Drains Your Finances After a Loss

Underinsurance is the silent killer in California homeowner policies. You think you’re protected until a loss happens and your dwelling limit covers only 70% of what rebuilding actually costs. The California Department of Insurance has released annual counts of new, renewed, and non-renewed homeowners and dwelling-fire policies in each ZIP code in California. This happens because homeowners set coverage limits based on outdated home values or lender minimums rather than current construction costs. A home purchased for $600,000 in 2015 might need $850,000 to rebuild today due to labor shortages, material inflation, and California’s stricter building codes.

If you haven’t adjusted your dwelling coverage in three years or more, you’re almost certainly underinsured. Request a replacement cost estimate from your insurer and compare it against your current dwelling limit. If the gap exceeds 10%, increase your coverage immediately. Construction costs don’t stabilize in California, and waiting for your next renewal could cost you hundreds of thousands of dollars out of pocket.

Water Damage and Flood Exclusions Leave You Exposed

Water damage and flood exclusions create a second major gap that catches homeowners off guard. Standard policies exclude flood damage entirely, which means storm surge, heavy rainfall, and overflow from rivers or streams receive zero coverage unless you purchase separate flood insurance through the National Flood Insurance Program. NFIP coverage maxes out at $250,000 for the structure and $100,000 for contents on single-family homes, leaving many California properties underprotected.

The California Department of Insurance emphasizes that standard policies also exclude certain types of water damage like seepage and gradual leaks, so a pipe that slowly damages your foundation over months won’t trigger coverage. These exclusions apply regardless of how comprehensive your policy appears on paper.

Earthquake Coverage Remains Your Biggest Blind Spot

Earthquake coverage presents a third critical gap. California requires insurers to offer earthquake insurance as a separate endorsement, but most homeowners skip it because they focus only on standard premium costs. Between 2018 and 2021, fire-related claims dominated California’s loss landscape, but a single moderate earthquake could exceed the total fire losses from that entire period. Earthquake coverage through the California Earthquake Authority typically costs 10 to 15% of your standard premium but protects your entire dwelling and personal property against seismic damage.

The decision to skip these coverages isn’t about saving money today-it’s about gambling with your financial security. Your next step involves reviewing flood and earthquake options with your agent before renewal, because waiting until after a disaster means paying out of pocket for losses that separate policies would have covered. These three gaps (underinsurance, water exclusions, and earthquake exposure) shape how you should structure your complete protection strategy moving forward.

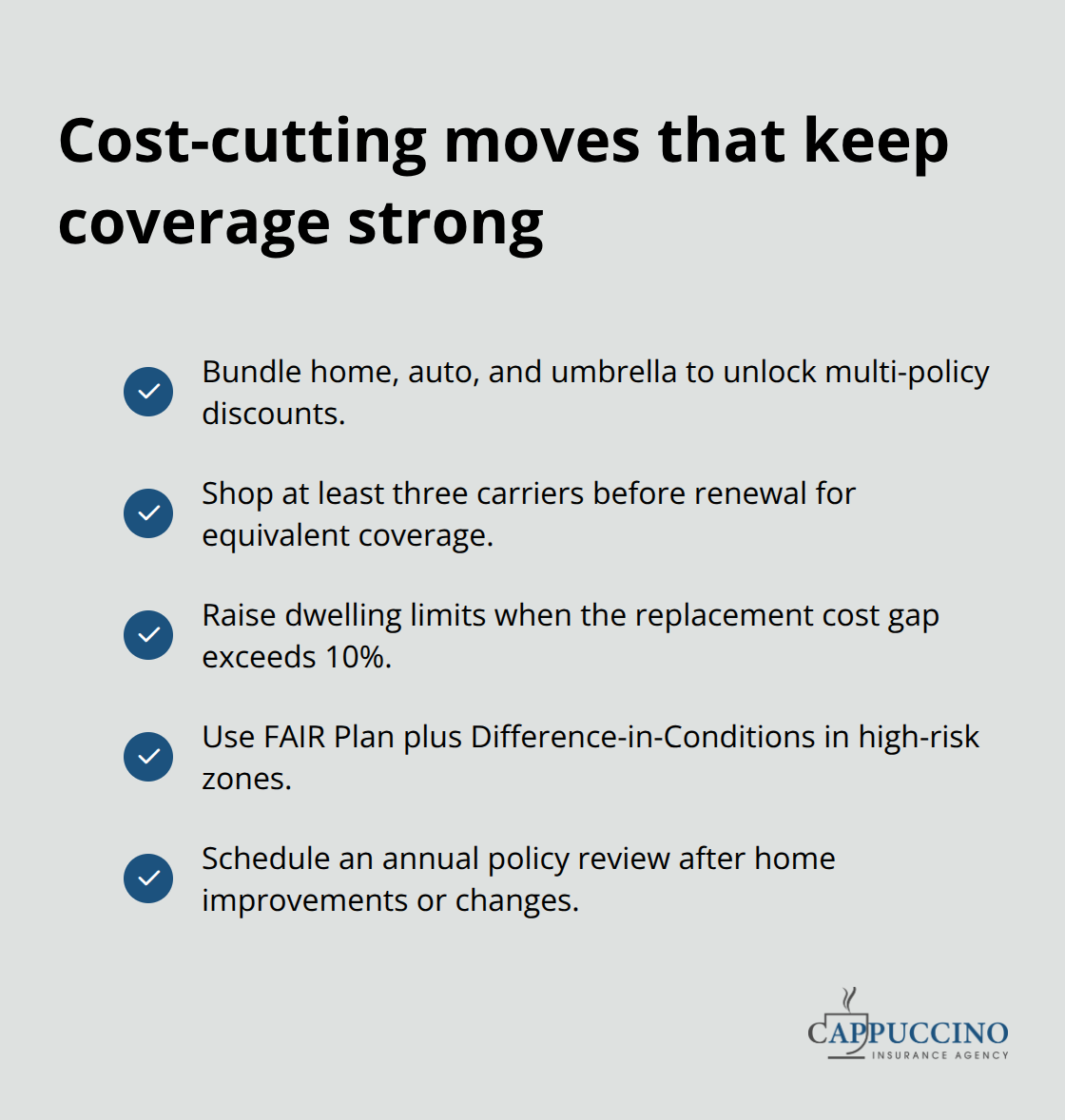

How to Cut Insurance Costs Without Cutting Protection

Bundle Your Policies to Unlock Real Savings

Bundle your policies with the same insurer to unlock significant savings on premiums, but most California homeowners never ask about it. Before you renew, request quotes for bundled coverage from at least three insurers and compare the total cost, not just the home insurance line item. Some carriers offer deeper discounts for bundling than others, and the savings compound when you add life insurance or umbrella coverage to the mix. One critical mistake homeowners make is accepting their current insurer’s renewal quote without shopping around.

Shop Around Before Your Renewal Date

California’s market has shifted dramatically since 2021, with new carriers entering certain ZIP codes while others have pulled back. Your renewal quote might be 15 to 30 percent higher than what a competing carrier charges for identical coverage, especially if your insurer has tightened underwriting in your area due to wildfire exposure or claims history. An independent agent can access multiple carriers and find combinations that work for your specific situation rather than forcing you into one company’s mediocre rates.

Increase Dwelling Coverage to Match Current Costs

Your dwelling coverage should increase annually to reflect California’s rising construction costs, which have outpaced inflation significantly. If you set your coverage limit three years ago based on a contractor estimate, that estimate is now obsolete. Request an updated replacement cost analysis from your insurer before each renewal and adjust your dwelling limit upward if the gap exceeds 10 percent of your current coverage. Construction costs don’t stabilize in California, and waiting for your next renewal could cost you hundreds of thousands of dollars out of pocket.

Address High-Risk Properties With Specialty Coverage

High-risk properties in wildfire zones or flood-prone areas need specialty endorsements that standard policies simply don’t include. The California FAIR Plan serves as a backstop for homeowners who can’t obtain private coverage, but FAIR Plan premiums run 40 to 60 percent higher than standard policies, making it a last resort rather than a permanent solution. If you’re in a high-risk area, ask your agent about Difference-in-Conditions policies that wrap around FAIR Plan coverage to provide additional protection at lower cost than FAIR Plan alone.

Schedule Annual Policy Reviews to Stay Current

Annual policy reviews keep your coverage aligned with your actual needs and home value. Schedule a review every 12 months with your agent to discuss any home improvements, additions, or changes in your personal property that might affect your limits. A kitchen renovation that increased your home’s value by $75,000 should trigger a corresponding increase in your dwelling and personal property limits, yet most homeowners never mention these improvements to their insurer.

Final Thoughts

Adequate homeowner coverage in California requires three concrete actions: stop relying on your lender’s minimum requirement, address the three major gaps that standard policies leave exposed, and review your coverage annually against current construction costs. Your lender protects their investment in your property, not your ability to rebuild your life after a total loss. Underinsurance, water damage exclusions, and missing earthquake coverage represent the real threats to your financial security, and ignoring them costs far more than the premiums you’d pay for complete protection.

Start by requesting a replacement cost estimate from your current insurer and comparing it against your dwelling limit. If the gap exceeds 10 percent, increase your coverage before your next renewal. Next, verify that you have separate flood insurance through the National Flood Insurance Program and earthquake coverage through the California Earthquake Authority or a private carrier (these aren’t optional add-ons in California, they’re essential components of real protection).

Shopping around matters more now than ever because California’s insurance market has shifted dramatically, with new carriers entering certain areas while others have pulled back from high-risk zones. Your current renewal quote might be significantly higher than what competing insurers charge for identical coverage. Contact Cappuccino Insurance Agency to schedule your homeowner coverage California evaluation and ensure your policy actually protects what matters most.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.