Property Owner Insurance California: Protecting Investment Properties

California property investors face unique insurance challenges that standard homeowners policies simply don’t address. Property owner insurance in California is built specifically for rental properties and investment real estate, covering risks that typical policies ignore.

At Cappuccino Insurance Agency, we’ve helped countless property owners navigate these coverage gaps. The right policy protects your investment from liability claims, lost rental income, and California’s specific hazards like wildfires and earthquakes.

What Property Owner Insurance Actually Covers

Property owner insurance covers the physical structure of your rental property, liability claims from tenants or visitors, and lost rental income when a unit becomes uninhabitable. The dwelling coverage protects the building itself against fire, wind, hail, vandalism, and theft. This differs fundamentally from a standard homeowners policy, which assumes you live in the property. When you rent out a home, condo, or apartment, insurers recognize that tenant-related risks and income protection become priorities that traditional policies ignore.

California’s Wildfire and Earthquake Exposure

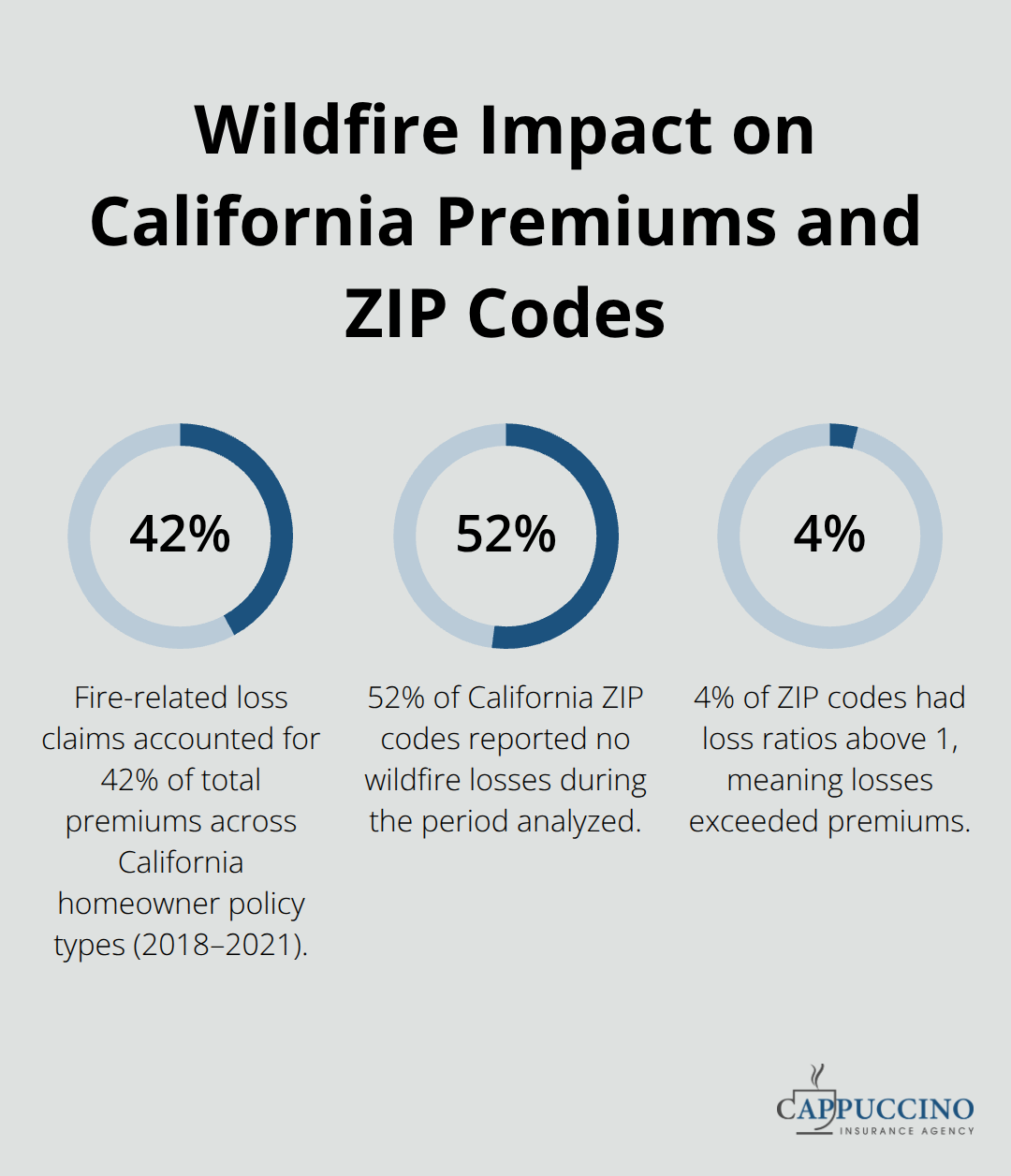

California property owners face wildfire exposure that directly impacts insurance availability and cost. The Terner Center at UC Berkeley found that fire-related loss claims accounted for approximately 42 percent of total premiums across all California homeowner policy types between 2018 and 2021.

Wildfire losses concentrate heavily in specific ZIP codes-52 percent of California ZIP codes reported no wildfire losses at all, yet 4 percent experienced ratios above 1, meaning losses exceeded premiums. Your location determines whether you pay standard market rates or face significant premium increases.

Earthquake coverage does not come standard in any landlord policy in California and requires a separate earthquake policy through the California Earthquake Authority. Flood coverage also sits outside standard policies and must be purchased separately through the National Flood Insurance Program. If your property sits in a high-risk fire zone or flood area, these gaps become expensive realities that renters insurance-which covers tenants, not property owners-completely misses.

The Income Protection Gap

Standard homeowners policies exclude the income protection that landlords need when a covered event makes a unit uninhabitable. You absorb lost rent while still paying mortgage, taxes, utilities, and maintenance costs. Property owner insurance includes loss of rental income coverage that homeowners policies simply do not offer because insurers assume you occupy the property yourself.

Why Homeowners Policies Leave Rental Properties Exposed

Your existing homeowners policy was written for owner-occupied properties and contains exclusions that leave rental properties exposed. Landlord liability coverage differs significantly from homeowner liability because tenant injuries on rental property carry different legal exposure than injuries at your primary residence. A tenant’s guest who slips on your rental property’s stairs creates liability that your homeowners policy may not adequately address.

Property owner insurance covers the dwelling structure, attached structures like garages and sheds, and essential systems-plumbing, electrical, HVAC-that renters cannot repair themselves. When a water heater fails or an electrical panel malfunctions, your policy covers the cost to restore habitability, whereas homeowners policies treat rental properties as non-insurable under their terms. Understanding these specific protections sets the foundation for evaluating which coverage types matter most for your investment strategy.

Key Coverage Types for Investment Properties

Dwelling Coverage: Getting the Numbers Right

Dwelling coverage forms the financial backbone of any property owner insurance policy, and setting this number correctly matters far more than most investors realize. Your dwelling limit must reflect the actual cost to rebuild your rental structure to current California building codes, not its market value. The Terner Center at UC Berkeley found that homes built after 2009 show significantly lower per-$100,000 insured costs than older properties, suggesting that building safety updates reduce replacement expenses. If your 1970s rental property needs a complete roof replacement or electrical system upgrade to meet current code, your policy must cover those modernization costs or you absorb the difference yourself. Obtain a detailed rebuild estimate from a licensed contractor specific to your property type and location before you set dwelling limits. NREIG, a California-focused investment property insurer, requires minimum dwelling coverage of at least $75 per square foot with no coinsurance penalty-a practical baseline that prevents underinsurance traps.

Attached structures like garages, sheds, and detached units require explicit coverage limits since they represent separate loss exposures. Essential systems coverage for plumbing, electrical, and HVAC protects you when these fail and tenants cannot legally occupy the unit until repairs are complete.

Liability Coverage: Protecting Against Catastrophic Claims

Liability coverage shields you from the financial devastation of tenant or visitor injury claims, and California’s tenant-friendly legal environment makes robust protection non-negotiable. Standard property owner policies include $1 million per occurrence and $2 million aggregate premises liability, but this baseline understates actual exposure for most California rental properties. A single slip-and-fall claim resulting in a permanent injury judgment can easily exceed $1 million in damages, leaving you personally liable for amounts above policy limits. Consider umbrella liability coverage that extends protection beyond your standard policy limits, particularly if you own multiple rental units or properties in high-traffic areas.

Document every safety upgrade you make-exterior lighting installation, secure lock replacements, allowed smart security cameras in common areas-because these investments reduce both actual risk and your insurance premiums. California’s habitability standards require landlords to maintain rental properties in safe condition, and insurers increasingly deny claims when deferred maintenance contributed to injuries. Liability coverage also covers defense costs and legal settlements, so even a baseless claim can cost thousands in attorney fees if your policy doesn’t pick up those expenses. Your policy should specify whether liability covers both bodily injury and property damage claims, as some carriers limit one or the other.

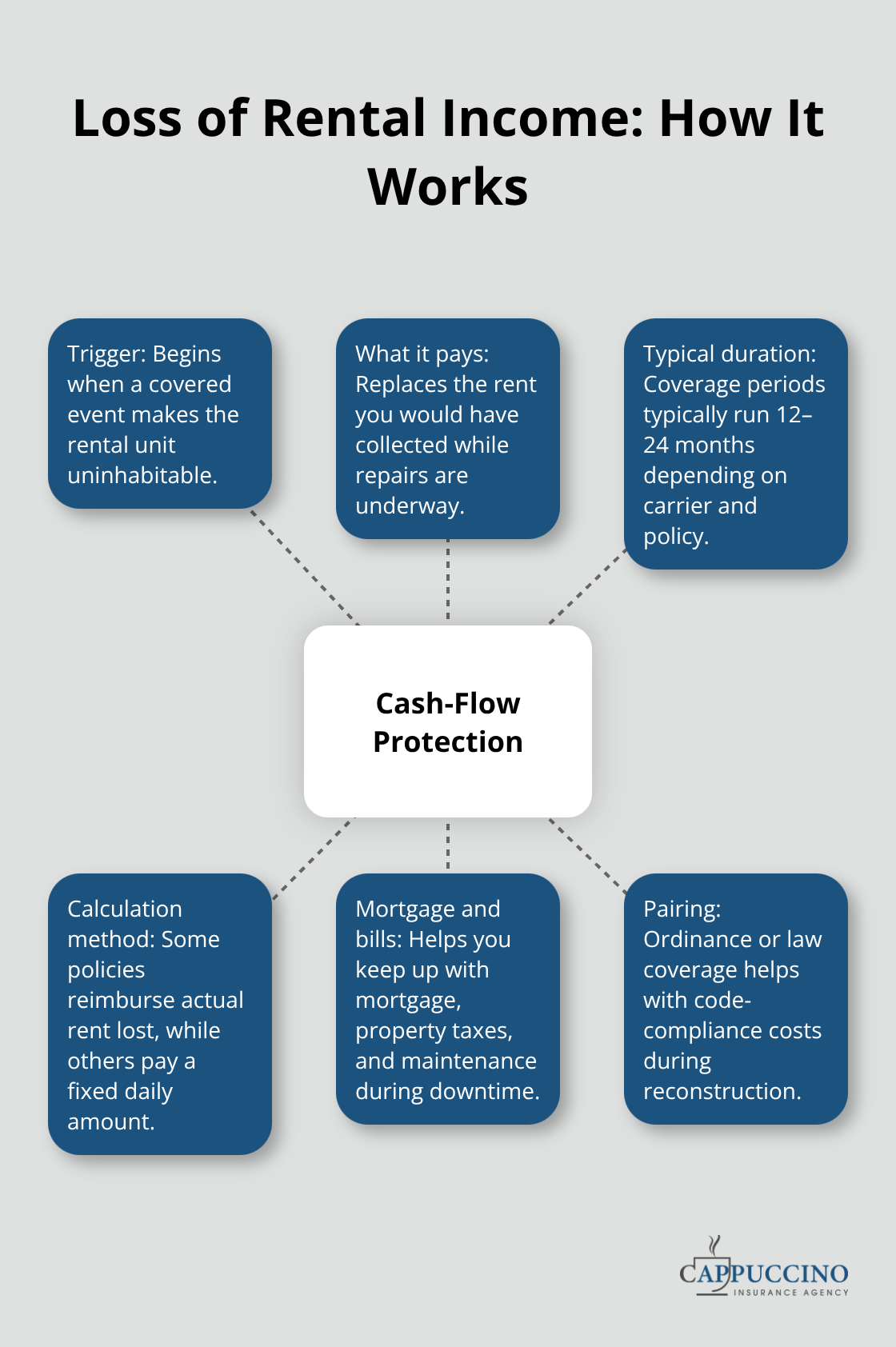

Loss of Rental Income: Protecting Your Cash Flow

Loss of rental income coverage separates serious property owner insurance from stripped-down policies that leave cash flow exposed. When a covered event like a fire or water damage makes your rental unit uninhabitable, this coverage replaces the rent you would have collected while repairs happen, protecting your mortgage payment, property taxes, and maintenance obligations.

The coverage period typically extends 12 to 24 months depending on your policy and carrier, giving you breathing room during extended reconstruction.

California’s median annual home insurance cost sits around $1,728 for landlord policies according to Policygenius data, yet many property owners skip loss of rent coverage to save $200 to $400 annually-a false economy that evaporates immediately after a single claim. Verify exactly how your carrier calculates lost rent, whether they account for seasonal vacancy patterns, and how they handle renovations that extend beyond immediate repairs. Some policies reimburse actual rent lost, while others use a fixed daily amount, creating dramatically different outcomes for high-value rentals. Ordinance or law coverage deserves equal attention because California building codes change constantly, and your policy must cover the cost to bring damaged structures into compliance with current standards rather than simply restoring them to pre-damage condition.

Understanding these three pillars positions you to evaluate additional coverage options that address California-specific exposures and your individual property risks.

Factors Affecting Property Owner Insurance Costs in California

California’s insurance market punishes property owners in high-risk areas while rewarding those who invest in maintenance and risk reduction. Your premium reflects your exact property’s exposure to wildfire, your building’s age and systems, and your track record as an investor-not a statewide average. The Terner Center at UC Berkeley analyzed California Department of Insurance data from 2018 to 2021 and found that fire-related loss claims consumed approximately 42 percent of total premiums across all homeowner policy types, yet this burden concentrated heavily in specific ZIP codes. Fifty-two percent of California’s ZIP codes reported zero wildfire losses, but 4 percent experienced loss ratios above 1, meaning claims exceeded all premiums collected. This extreme geographic variation explains why your neighbor five miles away pays $400 less annually than you do.

Location and Wildfire Risk Zones

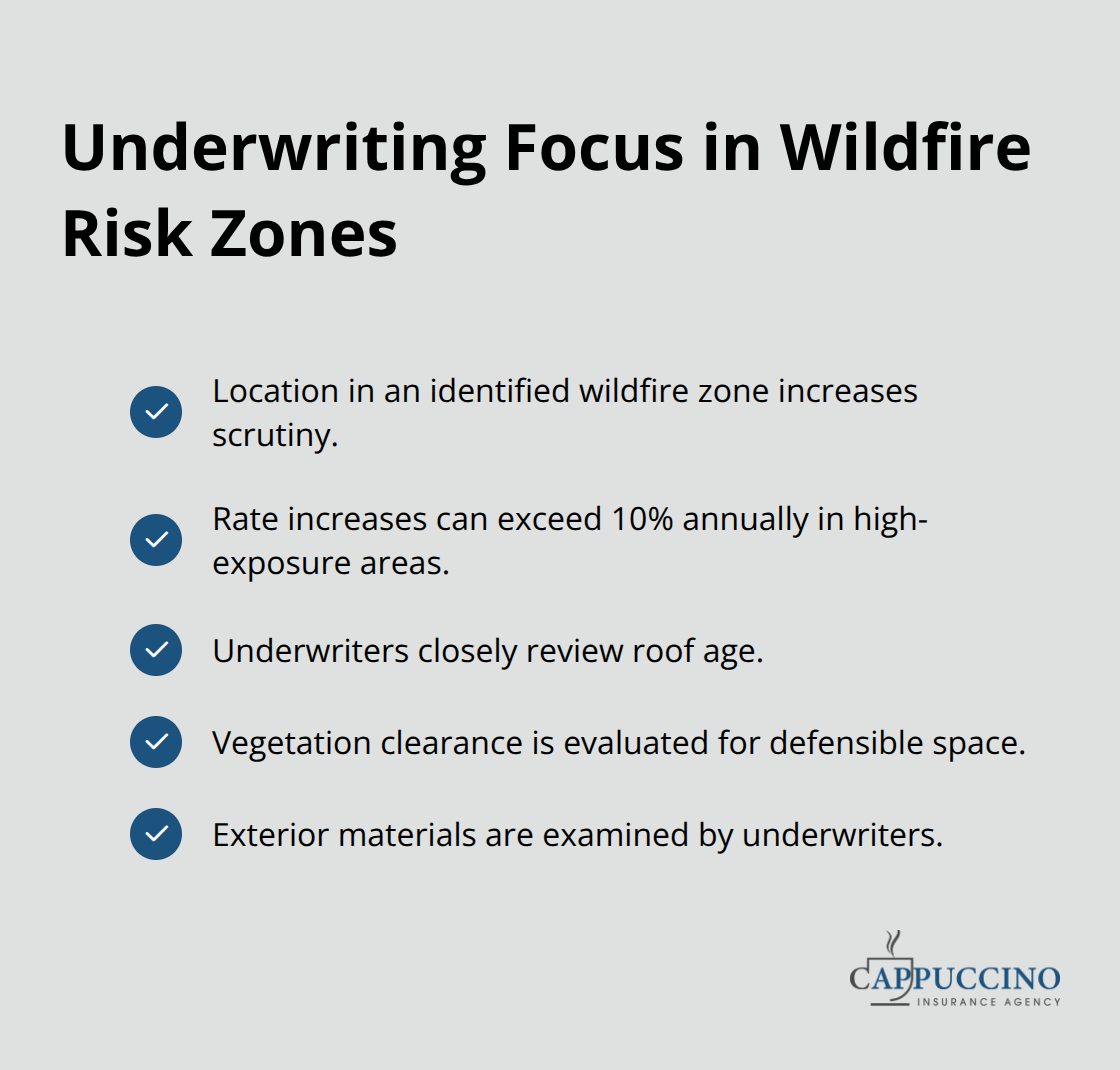

Insurers now price climate risk aggressively, and properties in high-fire-exposure zones face rate increases exceeding 10 percent annually. If your rental property sits in an identified wildfire zone, underwriters scrutinize roof age, vegetation clearance, and exterior materials with intensity that standard homeowners policies never required.

Your location determines whether you pay standard market rates or face significant premium increases that compound over time.

Building Age and System Condition

Properties built after 2009 benefit from modern building codes that reduce replacement costs, translating to lower per-square-foot insurance expenses compared to 1970s and 1980s stock. Older properties with original electrical panels, aging plumbing, or outdated HVAC systems trigger higher premiums because insurers recognize that these systems fail more frequently and create both property damage and liability exposure. A property with deferred maintenance-cracked roof shingles, overgrown vegetation, deteriorated exterior walls-faces non-renewal threats alongside premium increases, because underwriters now tie insurability directly to property condition rather than treating it as a secondary factor.

Claims History and Regional Factors

Your claims history shapes future premiums more than most investors realize, and a single water damage claim can increase your costs for five to seven years. California’s Inland Empire and High Desert markets face additional scrutiny because extreme heat accelerates system failures, aging property stock concentrates in these regions, and repair costs run 15 to 20 percent higher than coastal areas. Each claim you file creates a record that carriers reference for years, making prevention and maintenance investments far more cost-effective than accepting claims as inevitable.

Coverage Limits and Underinsurance Risk

Coverage limits directly impact premiums, but underinsurance creates far greater financial exposure than premium savings justify. NREIG requires minimum dwelling coverage of $75 per square foot with no coinsurance penalty, establishing a practical floor that prevents you from absorbing rebuild costs above your policy limit. Setting your liability limit at the standard $1 million per occurrence leaves you exposed in California’s tenant-friendly legal environment where a single permanent injury judgment regularly exceeds that amount. Higher limits cost more upfront but protect your personal assets from catastrophic claims.

An independent agent familiar with your specific property can compare multiple carriers and identify which companies offer competitive rates for your exact risk profile-something generic online quotes cannot accomplish because they fail to account for local construction types, neighborhood crime rates, and carrier-specific underwriting preferences. Annual policy reviews before busy rental seasons allow you to adjust coverage as rent increases, property improvements reduce risk, or market conditions shift, transforming insurance from a static expense into a dynamic risk management tool.

Final Thoughts

Property owner insurance in California protects your investment from financial exposure that standard homeowners policies completely ignore. The right coverage combines dwelling protection, liability defense, and loss of rental income into a comprehensive strategy that keeps your cash flow stable when disasters strike. Your specific property’s location, age, and condition determine which coverages matter most and what you’ll actually pay, making generic policies inadequate for serious investors.

Finding the right policy requires working with an agent who understands California’s unique rental market and can compare multiple carriers on your behalf. Online quotes miss critical details like your property’s exact rebuild cost, local wildfire exposure, and carrier-specific underwriting standards that dramatically affect both availability and price. An independent agency identifies which companies offer competitive rates for your risk profile and structures coverage that matches your investment strategy rather than forcing you into a one-size-fits-all package.

Contact Cappuccino Insurance Agency to evaluate your current exposure and identify gaps in your existing protection. We help property owners across California secure property owner insurance that reflects their actual risk and income protection needs through carrier comparisons and free coverage assessments. Document your property’s rebuild cost, review your liability limits against California’s legal environment, and confirm that loss of rental income coverage extends long enough to protect your mortgage payments during extended repairs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.