California Wildfire Risk Insurance: Protecting Homes in Fire-Prone Areas

California wildfire risk insurance has become harder to find and more expensive for homeowners in fire-prone areas. Standard insurance policies increasingly exclude properties in high-risk zones, leaving many families underprotected.

We at Cappuccino Insurance Agency help homeowners navigate these challenges by explaining your coverage options and showing you how to reduce your premiums through practical steps.

Why Home Insurance Disappears in High-Risk Fire Areas

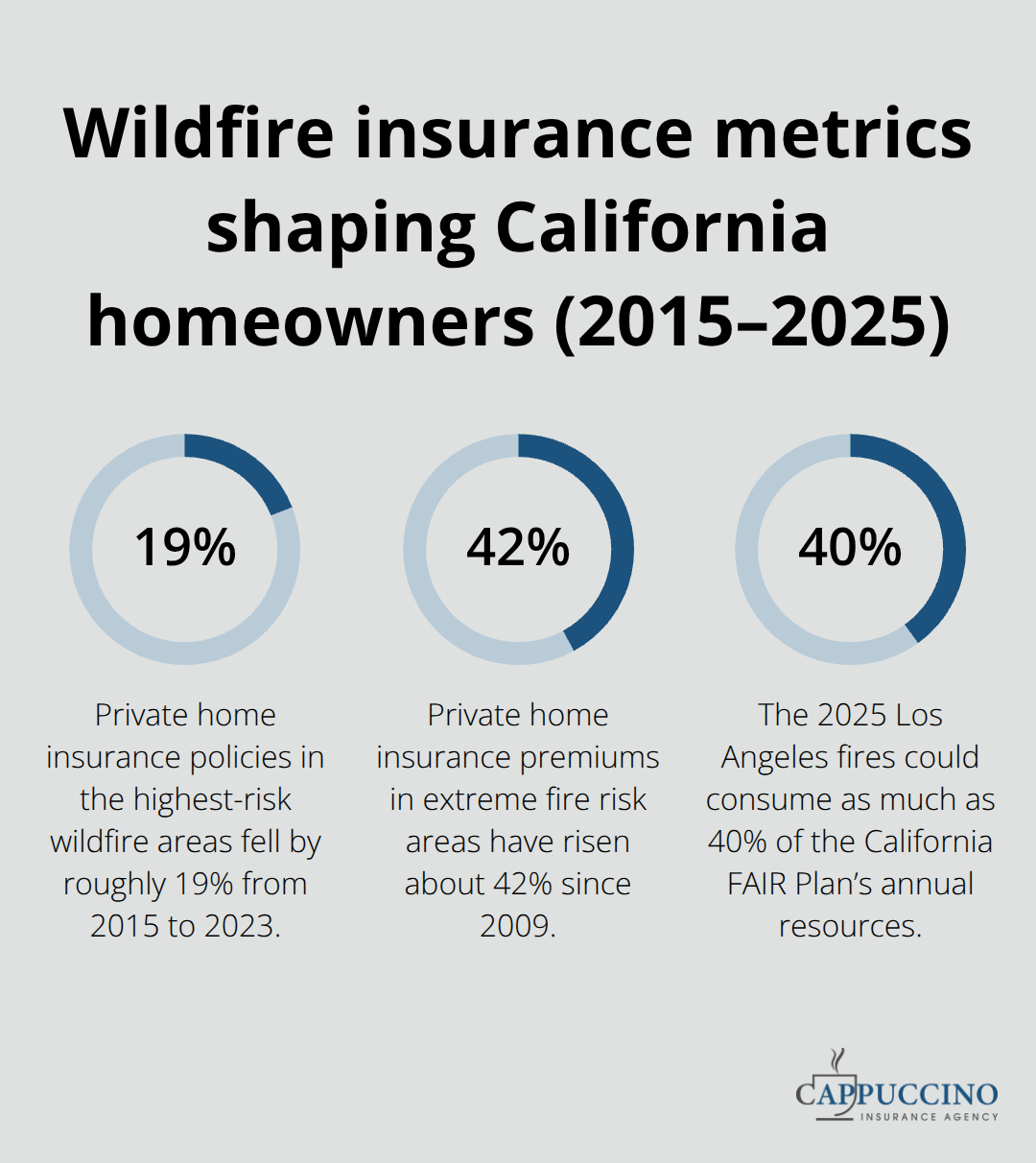

California’s insurance market is contracting in wildfire zones at an alarming rate. From 2015 to 2023, private home insurance policies in the highest-risk wildfire areas fell by roughly 19%, with declines accelerating sharply after 2019, according to California Department of Insurance data.

Since 2018 alone, over 30,000 home insurance policies have faced non-renewal in California’s extreme fire risk regions. In the most extreme wildfire risk areas, private coverage has dropped for about 1 in 5 homes since 2019. More than 150,000 households in California’s highest-risk ZIP codes remained uninsured as of 2023, meaning they face total financial loss if a large fire strikes their property. This isn’t a minor gap-it’s a crisis that affects your ability to secure a mortgage, protect your equity, and recover after a disaster.

The Economics Driving Insurers Away

Insurers are leaving high-risk zones because the math no longer works for them. Private home insurance premiums in extreme fire risk areas have risen about 42% since 2009, yet insurers still face massive wildfire losses that exceed what they collect in premiums. The 2025 Los Angeles fires alone could consume as much as 40% of the California FAIR Plan’s annual resources, triggering emergency assessments on private insurers that remain in the state. When catastrophic losses hit, insurance companies respond with rate increases, tighter underwriting standards, or market exits. Properties in ZIP codes classified above the 90th percentile for Wildfire Hazard Potential face the harshest treatment. Standard homeowners policies typically exclude or severely limit fire coverage in these zones, forcing homeowners into the California FAIR Plan-a backstop insurer that provides only basic dwelling coverage without personal property protection, liability limits, or additional living expenses coverage. This leaves you dramatically underinsured compared to what a standard policy would provide.

The FAIR Plan Growth Reveals Market Failure

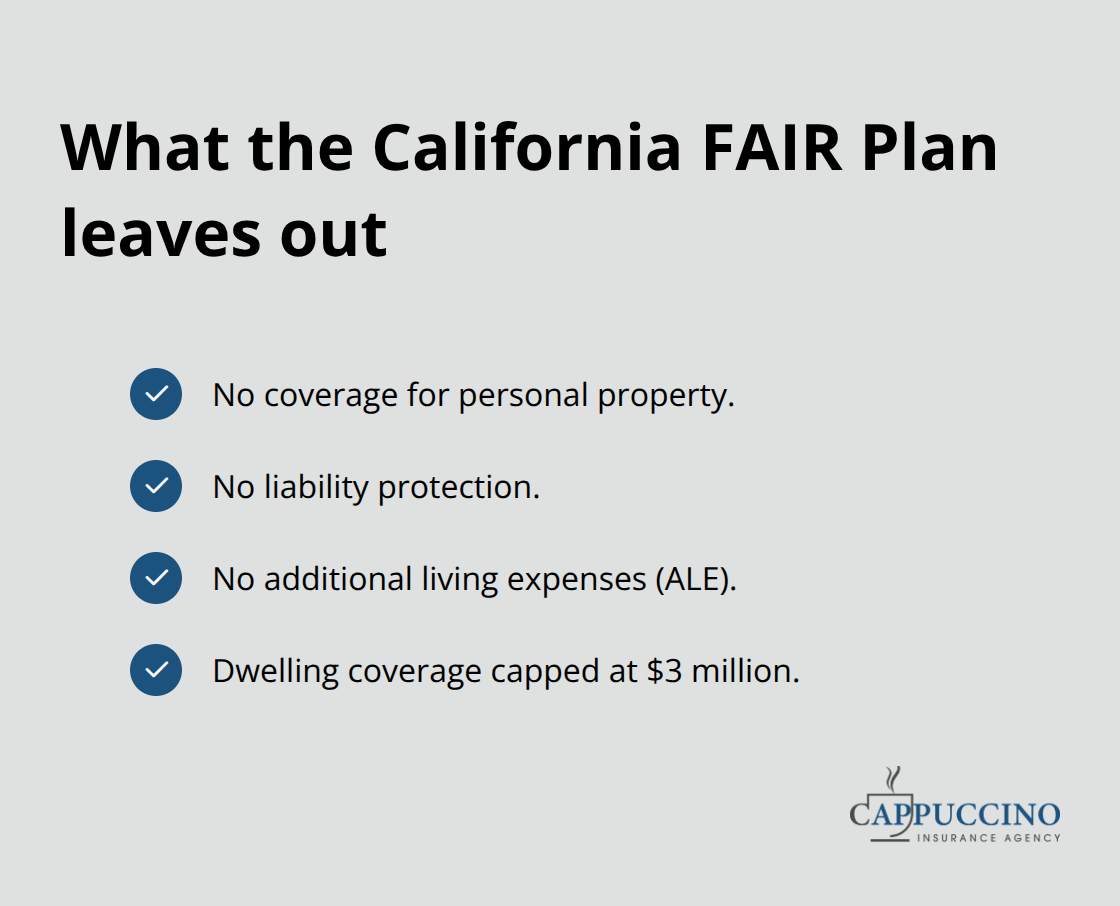

California’s FAIR Plan insured about 210,000 homes in 2020. That number had ballooned to over 463,000 homes by 2024, with total exposure exceeding $450 billion. This explosive growth signals that private insurers have abandoned hundreds of thousands of California homeowners. FAIR Plan policies typically cap dwelling coverage at $3 million and exclude personal property, meaning your belongings inside the home receive no protection. If you own a home valued at $1.5 million with $500,000 in personal property, a FAIR Plan policy covers only the structure, leaving your contents completely exposed. Many homeowners don’t realize this limitation until after a loss occurs. Mortgage lenders require proof of insurance, so uninsured homeowners often face pressure to accept whatever coverage they can find, even if it’s inadequate.

The Two-Tier System and Your Coverage Options

This market collapse creates a two-tier system where wealthy homeowners can shop among insurers or self-insure, while middle-class families get pushed into bare-bones FAIR coverage or drop into the uninsured pool entirely. You need to understand what FAIR Plan policies actually cover and what gaps remain. Difference-in-Conditions policies and wraparound coverage exist to fill those gaps, but finding the right combination requires expertise in high-risk properties. An independent agency that partners with multiple carriers can help you navigate these options and identify solutions that standard insurers won’t offer.

What Actually Covers You When Standard Insurance Won’t

The FAIR Plan Foundation and Its Real Limits

The California FAIR Plan exists because private insurers have abandoned high-risk properties, but it provides only a foundation you’ll almost certainly need to build on. The FAIR Plan covers the dwelling structure itself up to $3 million for owner-occupied homes up to four units. However, personal property inside your home receives zero coverage-your furniture, electronics, clothing, and valuables remain completely unprotected. Liability coverage, which protects you if someone gets injured on your property, is also excluded. Additional living expenses that cover hotel costs after displacement don’t exist under FAIR Plan policies.

A licensed broker can help you apply at no extra cost, and the application process includes a search for traditional coverage first. You should expect to need supplemental protection to close these dangerous gaps.

Wraparound Coverage Transforms Your Protection

A Difference-in-Conditions policy fills the exact gaps that FAIR Plan policies leave open by providing personal property, liability, and additional living expenses when standard homeowners coverage isn’t available in the traditional market. This wraparound approach costs more than FAIR Plan alone, but it transforms you from dangerously underinsured to reasonably protected. The combination of FAIR Plan dwelling coverage plus a Difference-in-Conditions wrap gives you the comprehensive protection that standard policies would have provided. Without this supplemental layer, a total loss leaves your personal belongings and liability exposure completely unprotected, which exposes you to financial ruin that insurance was supposed to prevent.

Specialty Carriers and Strategic Placement

The real challenge lies in finding insurers willing to write Difference-in-Conditions policies and other specialty coverage for wildfire-risk properties. Most standard carriers won’t touch these properties at any price, which is why working with an independent agency matters far more than shopping online. An independent agency that partners with multiple carriers can access specialty insurers focused specifically on hard-to-place properties that other brokers simply cannot reach. These specialized carriers understand wildfire risk differently than mass-market insurers and price accordingly, often offering better rates if you’ve completed defensible space work or roof upgrades. The California Safe Homes Act creates grants to cover fire-safe roofs and 5-foot ember-resistant zones around properties. Once you’ve completed these improvements, you have documentation to show specialty carriers, which directly improves your rates and coverage options.

Avoiding Underwriting Mistakes

Don’t apply to multiple carriers independently-this damages your underwriting profile and reduces your approval odds. Instead, let a broker with relationships in the specialty market submit you strategically to carriers most likely to approve your property. Strategic placement prevents unnecessary inquiries on your record and increases approval odds substantially. A broker who understands which carriers focus on wildfire-risk properties (and which ones avoid them entirely) saves you months of rejection letters and protects your ability to secure coverage at competitive rates. Your next step involves identifying which home hardening upgrades will have the biggest impact on your specific property and your insurance options.

How Home Hardening Cuts Your Premiums and Expands Coverage Options

Fire-Resistant Upgrades Open New Insurance Doors

The gap between what FAIR Plan policies cover and what you actually need to protect your home narrows dramatically once you invest in fire-resistant upgrades. Specialty insurers pricing wildfire-risk properties reward concrete risk reduction with lower rates and broader coverage terms. The California Safe Homes Act provides grants that cover part or all costs of fire-safe roofs and Zone Zero mitigation within five feet of your home, which means your upgrade expenses may be partially or fully subsidized by the state. This creates a direct financial incentive: complete these improvements, document them thoroughly, and watch your insurance options expand immediately.

Defensible Space Work Delivers Real Savings

Defensible space work-removing dead vegetation, clearing gutters, and trimming tree branches ten feet from your roof-costs far less than the premium increases you’ll face without it. A professional defensible space assessment typically runs $200 to $400 and identifies exactly which improvements matter most for your specific property and its surrounding landscape. Once completed, this documentation becomes your negotiating tool with specialty carriers that understand how these measures reduce wildfire loss severity.

Documentation Transforms Your Negotiating Power

The documentation process matters as much as the work itself. Take dated photographs before and after each upgrade, keep receipts for all materials and labor, and file these records with your insurance broker well before policy renewal. Specialty carriers want proof that you’ve completed Zone Zero mitigation and roof upgrades because these measures directly reduce wildfire loss severity-they’re not interested in vague claims about defensible space. Annual policy reviews catch coverage gaps before they become problems and ensure your documentation stays current as your property changes.

Bundling Discounts Work Only With the Right Carrier

Bundling home and auto insurance with a single carrier typically generates 15% to 25% discounts on both policies, which matters more when you’re already facing elevated rates in high-risk zones. However, bundling only saves money if the carrier actually writes in your ZIP code and offers competitive rates on both lines-many carriers that exit high-risk areas leave you unable to bundle at all. An independent agency evaluates which carriers offer bundling discounts for your specific risk profile and location, then places your coverage strategically rather than forcing you into whatever single carrier happens to write in your area.

Final Thoughts

California wildfire risk insurance has shifted from a convenience to a necessity for homeowners in fire-prone areas. The market collapse we’ve outlined isn’t theoretical-it’s happening now, with over 150,000 households already uninsured and FAIR Plan enrollment doubling in just four years. Your coverage options exist, but finding them requires understanding both what FAIR Plan policies actually provide and what gaps you need to fill with wraparound coverage.

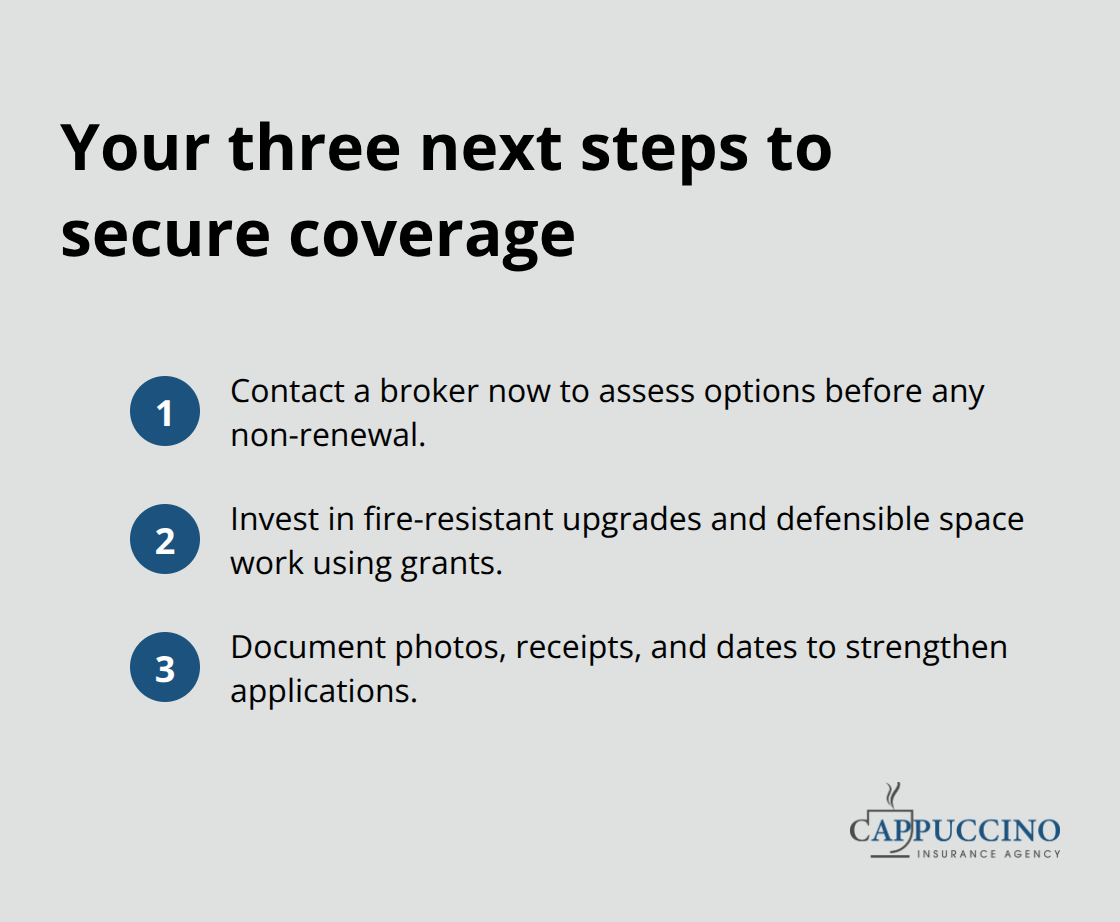

The path forward involves three concrete steps: stop waiting for your current insurer to renew your policy and contact a broker now to assess your coverage options before non-renewal notices arrive. Invest in fire-resistant upgrades and defensible space work while state grants cover much of the cost through the California Safe Homes Act, since these improvements directly expand your insurance options and lower your premiums with specialty carriers that understand wildfire risk. Document everything-photographs, receipts, and completion dates become your negotiating power when applying for coverage with carriers that price based on actual risk reduction.

Local expertise matters more in high-risk areas than anywhere else in California, and an independent agency that partners with multiple carriers can access specialty insurers and strategic placement options that online shopping simply cannot reach. We at Cappuccino Insurance Agency work with multiple carriers to deliver solutions for hard-to-place wildfire-risk properties, including FAIR Plan coverage and Difference-in-Conditions wraps that transform your protection from dangerously inadequate to reasonably comprehensive. Contact us today to secure the coverage your home actually needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.