Auto Insurance Discounts California: Maximize Your Savings

California drivers overpay for auto insurance every single year. Most people stick with their current policy without realizing they’re leaving hundreds of dollars on the table through unclaimed discounts.

At Cappuccino Insurance Agency, we’ve helped countless drivers find auto insurance discounts in California that actually fit their situation. This guide shows you exactly which discounts exist and how to qualify for them.

Which Discounts Actually Save You Money in California

Safe Driver Discounts: The High Bar for Qualification

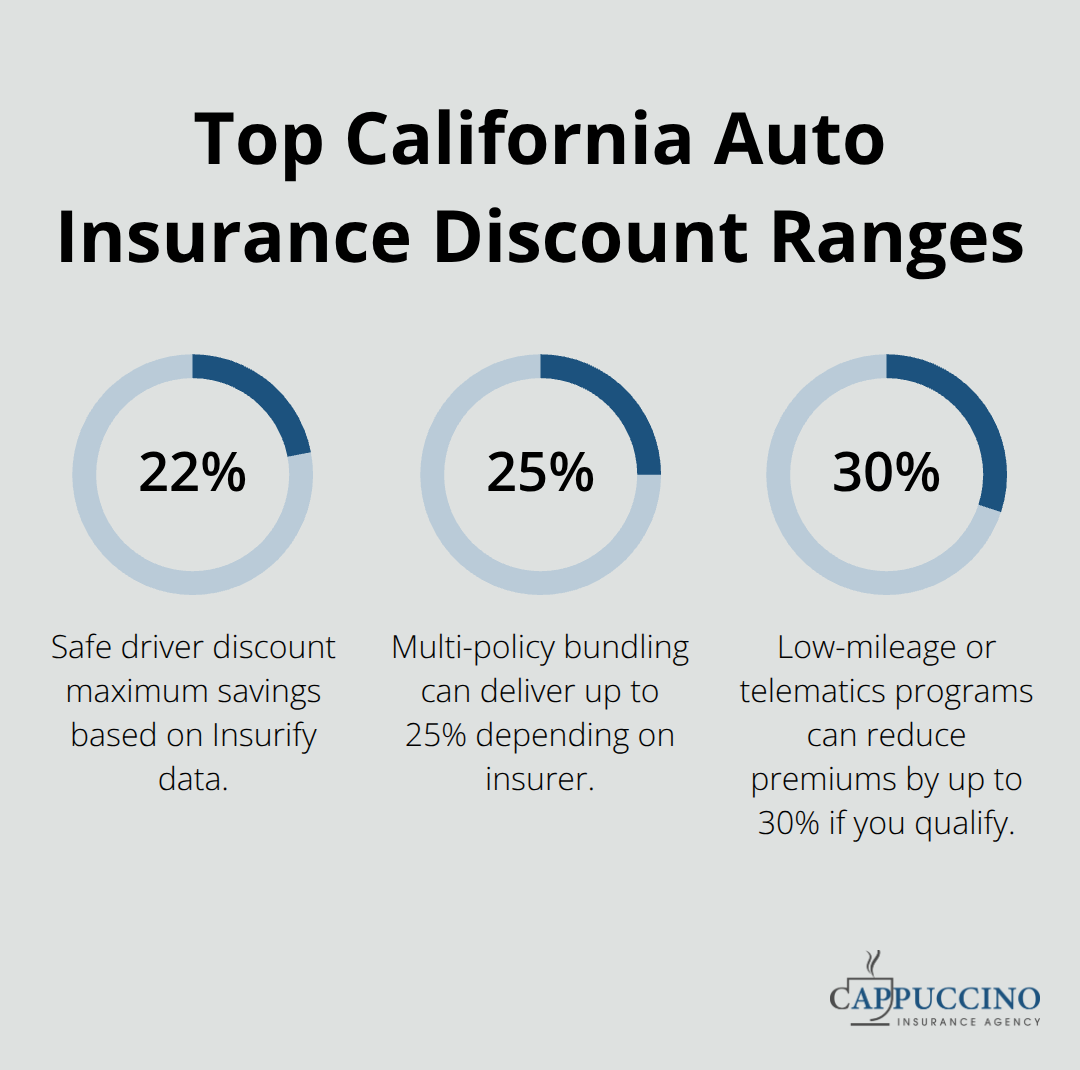

Safe driver discounts cut your premium by up to 22% according to Insurify’s data, but this discount only works if you actually qualify under California’s definition. California considers you a good driver if you have no more than one at-fault property damage accident or one moving violation point in the past three years, plus zero at-fault accidents involving bodily injury or death. One speeding ticket or minor fender-bender disqualifies you immediately. This is why safe driver discounts feel out of reach for many California drivers-the bar is genuinely high.

The state’s minimum coverage jumped to 30,000/60,000/15,000 on January 1, 2025, which means your liability costs increased whether you qualified for discounts or not. If you do have a clean record, this discount stacks with others, so claim it.

Multi-Policy Bundling: The Most Actionable Discount

Multi-policy bundling delivers real savings that range from 7% to 25% depending on your insurer. Bundling auto with homeowners, renters, or condo policies typically produces larger overall savings than buying policies separately.

The California average for full-coverage auto insurance sits around $190 per month according to Insurify data, while liability-only averages $92 per month. Bundling could reduce your combined home-and-auto cost by hundreds of dollars annually, which makes this the single most actionable discount available.

Low-Mileage and Telematics Discounts: Privacy Versus Savings

Low-mileage and usage-based telematics discounts range from 10% to 30%, but these require different approaches. Low-mileage discounts apply if you drive significantly fewer miles than average, though eligibility thresholds vary by insurer. Telematics programs install monitoring devices or apps that track your actual driving behavior-acceleration, braking, time of day, speed.

Now that you understand which discounts actually move the needle, the next step involves qualifying for them-and that requires a different strategy for each discount type.

How to Qualify for These Discounts

Safe Driver Discounts: The Three-Year Reset

Safe driver discounts require perfection for three years straight. One speeding ticket or fender-bender erases your eligibility entirely. If you’ve already lost this discount due to a minor violation, the fastest path back is waiting. Your driving record resets after three years, so if you received a ticket in March 2023, you regain eligibility in March 2026.

This all-or-nothing qualification frustrates many California drivers. The realistic approach involves acknowledging whether you actually qualify right now rather than hoping your insurer overlooks a violation. If you don’t qualify, focus your energy on multi-policy bundling instead, which requires zero driving perfection.

Multi-Policy Bundling: The Easiest Path to Savings

Multi-policy bundling works differently because it depends entirely on what you already own, not your driving behavior. If you own a home, rent an apartment, or carry life insurance, you’re already qualified. The mechanics are straightforward: call your current homeowners or renters insurer and ask what auto bundle discount they offer, then compare that against quotes from other carriers who bundle.

California drivers who bundle typically save between 7% and 25% on their combined premium, according to data from the Insurance Information Institute. The action step here is concrete-spend one hour getting three bundle quotes and compare the total annual cost for home plus auto together, not separately. Many drivers compare auto quotes alone and miss the bigger savings hiding in bundled packages.

Annual Policy Reviews: Catching Missed Discounts

Your situation changes constantly throughout the year. You might have paid off your mortgage, qualified for a good student discount through a child, or switched to remote work and now drive fewer miles. Insurers rarely proactively adjust your premium downward when these changes happen-you must initiate the conversation.

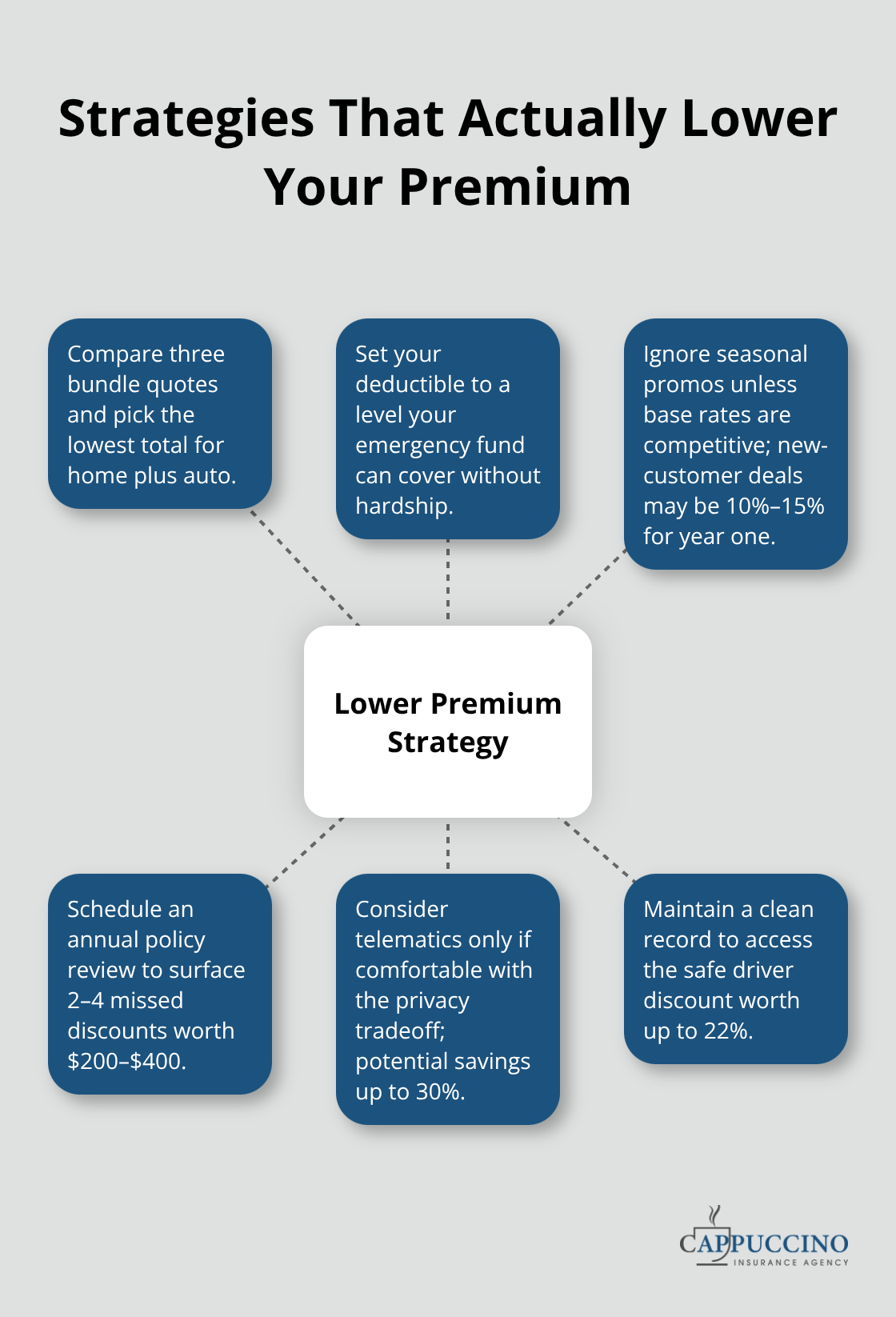

Set a calendar reminder for your policy renewal date each year and request a fresh quote before your renewal goes through. This 30-minute task typically surfaces 2-4 new discounts you weren’t using before. California drivers who review annually save an average of $200-$400 per year simply because they caught discounts their previous quote missed.

Moving Forward with Strategic Comparisons

Once you’ve identified which discounts apply to your specific situation, the next step involves comparing how different carriers price those discounts. Not all insurers value the same discounts equally, which means your best rate depends on finding the carrier whose pricing aligns with your profile.

Strategic Policy Choices That Actually Lower Your Premium

Compare Bundle Quotes Across Multiple Carriers

Bundling home and auto insurance remains the fastest way to reduce your overall insurance costs, but the execution matters far more than the intention. When you call your current homeowners insurer to add auto coverage, you’ll typically see a bundle discount between 7% and 25% depending on the carrier and your location. However, this approach often leaves money on the table because you anchor to your existing insurer’s pricing.

The better strategy involves obtaining three separate bundle quotes before committing to any carrier. Compare the total annual cost for both policies combined, not just the auto premium alone. A carrier offering a smaller auto discount but a larger homeowners discount might deliver a lower total cost than the insurer with the headline-grabbing auto bundle percentage. California drivers who skip this comparison step typically overpay by $300 to $600 annually on their combined home and auto premium.

Set Your Deductible to Match Your Financial Reality

Your deductible is the amount you pay out of pocket before insurance covers the rest of a claim. Raising your deductible from $500 to $1,000 typically cuts your collision and comprehensive premiums by 15% to 30%, according to data from the Insurance Information Institute. The math works only if you can actually afford that higher deductible without financial strain.

If a $1,000 deductible forces you to carry credit card debt or skip other expenses, the premium savings vanish because you’ve created a different financial problem. Calculate your emergency fund balance, then set your deductible to a level you could genuinely pay without disrupting your budget. Many California drivers set deductibles far too high chasing savings, then face genuine hardship when a claim arrives.

Ignore Most Seasonal and Limited-Time Offers

Seasonal and limited-time offers from insurers rarely deliver substantial savings despite the marketing language. Some carriers run promotions offering $50 or $100 discounts for signing up during specific months, but these one-time credits disappear after the first year while your base premium remains unchanged. The only exception involves new-customer discounts from carriers you’ve never used before, which can occasionally reach 10% to 15% off your first policy year.

These discounts matter only if the carrier’s base rates are competitive in your area to begin with. Chasing seasonal promotions while ignoring your overall rate structure is like celebrating a $100 coupon while paying $2,000 more annually than a competitor charges.

Final Thoughts

California drivers waste hundreds of dollars annually by ignoring auto insurance discounts California that directly apply to their situation. Safe driver discounts cut premiums by up to 22%, multi-policy bundling delivers 7% to 25% in savings, and low-mileage programs offer 10% to 30% reductions if you qualify. The gap between what you currently pay and what you could pay with proper discount stacking often reaches $300 to $600 per year.

Identify which discounts match your actual circumstances rather than chasing discounts you don’t qualify for. If you have a clean driving record, claim the safe driver discount immediately. If you own a home or rent an apartment, obtain three separate bundle quotes comparing your current insurer against State Farm and USAA before renewal. Set your deductible to a level you can genuinely afford without financial strain, then ignore seasonal promotions that disappear after year one.

Schedule an annual policy review before your renewal date arrives-your situation changes constantly, and insurers won’t proactively lower your premium when you qualify for new discounts. One 30-minute conversation typically surfaces 2 to 4 missed discounts worth $200 to $400 annually. Contact Cappuccino Insurance Agency to get started with a local agent who understands California’s insurance landscape and can match you with the right coverage at the right price.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.