Apartment Building Owner Insurance: Protect Your Investment

Apartment building owners face unique financial risks that go far beyond typical homeowner concerns. At Cappuccino Insurance Agency, we’ve helped countless property owners understand what coverage actually protects their investment.

The right apartment building owner insurance covers everything from structural damage to liability claims. This guide walks you through the coverage types you need, the risks you face, and how to select a policy that fits your property.

What Coverage Actually Protects Your Apartment Building

Building Structure and Property Protection

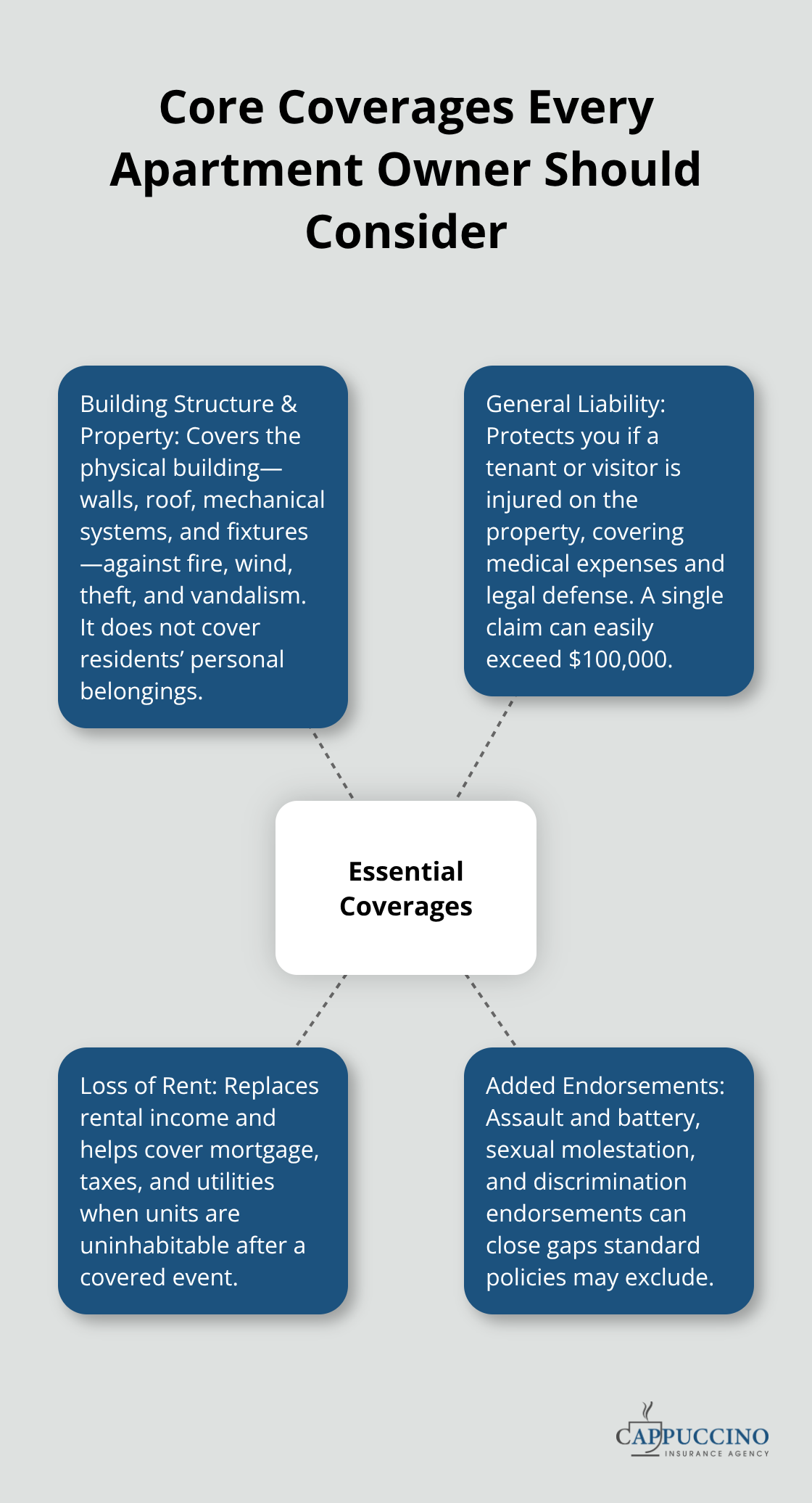

Property damage, liability claims, and lost rental income represent three distinct financial threats to apartment building owners, and each requires separate coverage. Building structure and property protection covers the physical building itself-walls, roof, mechanical systems, and fixtures-against fire, wind, theft, and vandalism.

This coverage protects your asset value, but it does not protect residents’ personal belongings, which remain their responsibility.

Your property value assessment should account for replacement cost, not just market value, since rebuilding typically costs more than selling.

General Liability Coverage for Injuries

General liability coverage protects you when a tenant or visitor suffers injury on the property-a slip on icy stairs, a fall in a common area, or an accident in a hallway-and covers medical expenses and legal defense costs. This coverage is non-negotiable because a single injury claim can easily exceed $100,000, and without it, you face personal liability.

Owners often overlook assault and battery, sexual molestation, and discrimination claims as potential exposures. Adding endorsements for these risks strengthens your protection against costly third-party lawsuits that standard policies may not cover.

Loss of Rent Protection

Loss of rent protection fills a critical gap that many owners overlook: if a covered event like a fire or pipe burst makes units uninhabitable, you lose rental income during repairs. This coverage pays your mortgage, property taxes, utilities, and other fixed expenses while the building is being restored, preventing cash-flow collapse.

Rising Costs and Deductible Pressures

Rising insurance costs and deductible pressures force owners to make difficult choices about coverage levels and deductible amounts. Understanding your specific property risks-location, age, building systems, and claims history-helps you select appropriate limits without overpaying for unnecessary protection or leaving gaps that expose you to catastrophic loss.

Common Risks Apartment Building Owners Face

Water Damage Strikes Without Warning

Water damage represents the costliest risk apartment building owners face, and it strikes without warning. Broken pipes, leaking water heaters, faulty washing machines, and toilet overflows cause continuous property damage claims that owners often fail to anticipate. Flood-prevention devices detect leaks and automatically shut off the water supply to protect appliances with water-supply lines, including water heaters, washing machines, toilets, and dishwashers. Insurers offer premium credits for installing these devices, making them a cost-effective investment that pays for itself through lower premiums.

Cooking Fires Demand Active Prevention

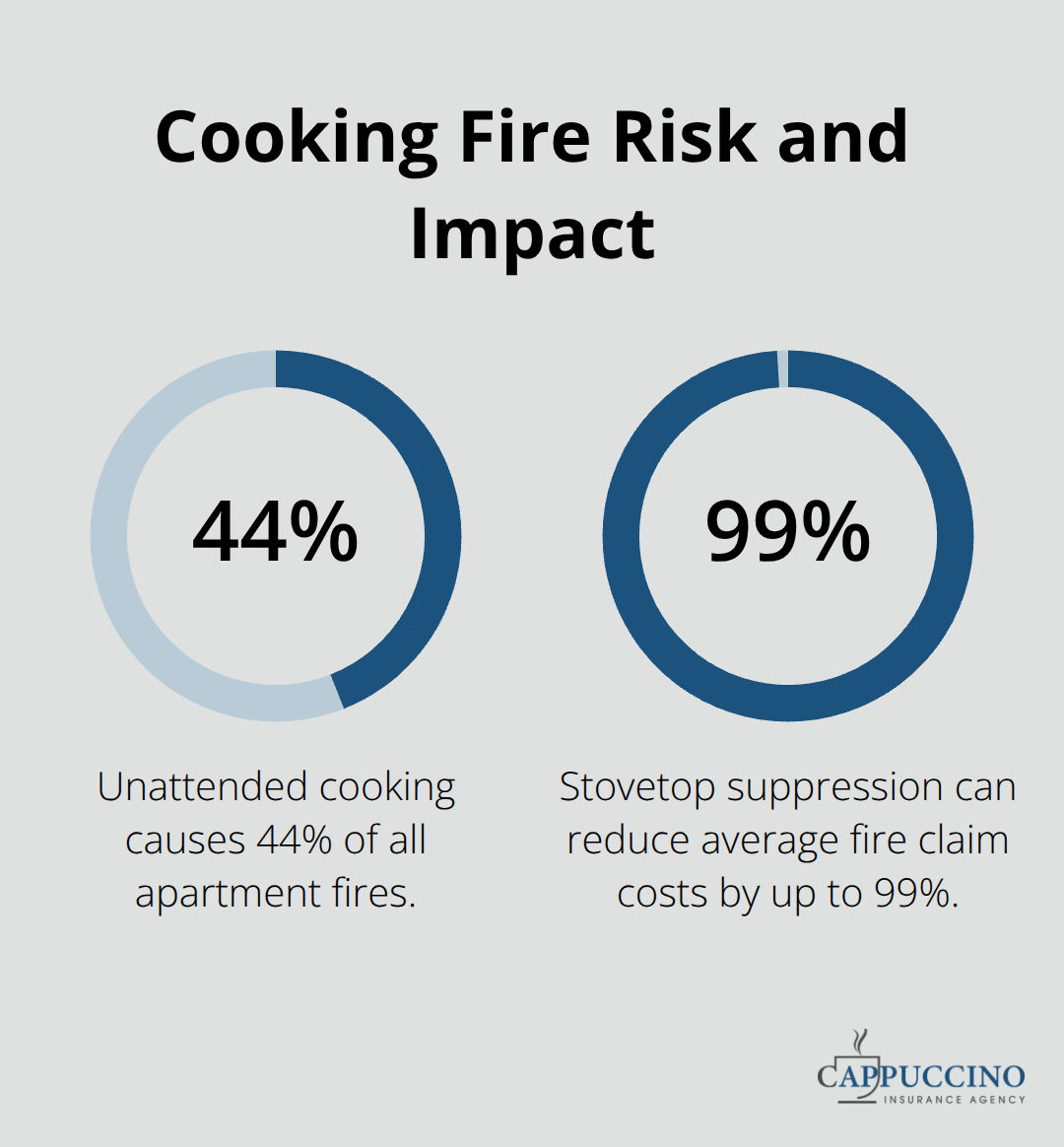

Unattended cooking causes 44% of all apartment fires according to the National Fire Protection Association, accounting for 156,300 cooking fires annually with $1 billion in direct property damage. Stovetop fire suppression devices mounted above or under the vent hood can reduce average fire claim costs by up to 99%, and some insurers provide premium credits for installing them.

Several states have enacted ordinances mandating these devices in multifamily dwellings because they work. Installing these devices represents one of the most effective risk-mitigation steps an owner can take.

Natural Disasters and Regional Exposure

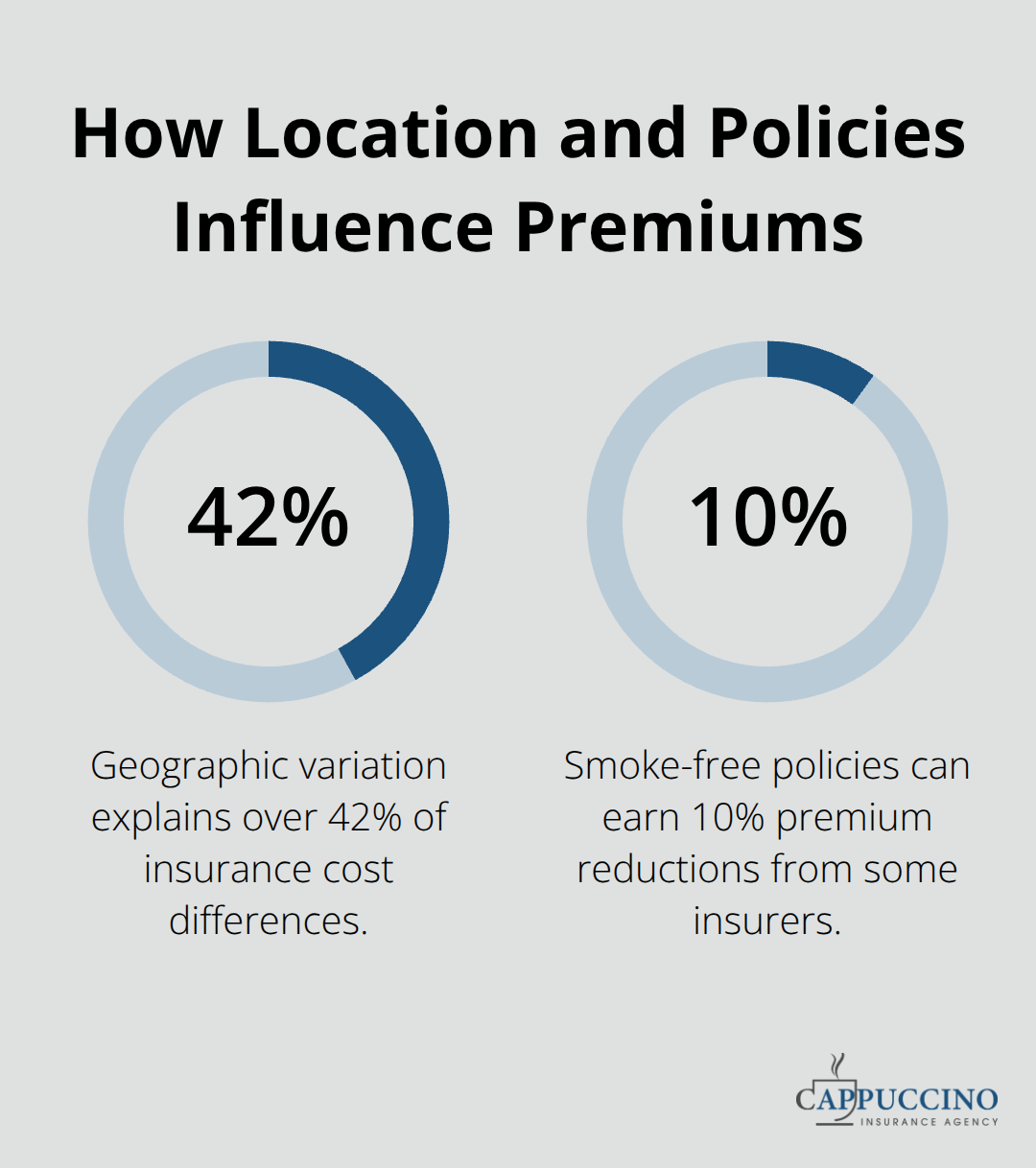

Fire, wind, hail, earthquakes, and floods destroy buildings and eliminate rental income simultaneously, which is why loss of rent protection exists as a separate coverage component. Geographic variation matters enormously: ZIP-code factors explain over 42% of cost-growth variation according to Federal Reserve analysis, meaning coastal properties and disaster-prone regions face substantially steeper premiums and stricter underwriting. Owners in high-risk areas should prioritize smoke-free policies, which some insurers credit with 10% premium reductions, alongside robust maintenance programs and physical resilience improvements like roof upgrades and fire sprinklers.

Rising Deductibles Create Financial Exposure

The Federal Reserve Bank of Minneapolis found that multifamily property insurance premiums rose 45% from 2023 to 2024, with average deductibles surging 412% year-over-year. This dramatic shift means owners face higher out-of-pocket costs when losses occur, making risk mitigation strategies essential rather than optional. Understanding your property’s specific exposure profile-location, age, building systems, and claims history-determines whether standard policies suffice or whether you need specialized endorsements for environmental risks, equipment breakdown, or business interruption.

Selecting the Right Coverage for Your Property

Calculate Your True Replacement Cost

Start with an honest assessment of what your building would cost to rebuild from the ground up, not what it would sell for today. Replacement cost typically runs 20–40% higher than market value because construction expenses, labor, and materials dominate rebuilding budgets in ways they don’t affect resale prices. The Federal Reserve’s analysis of multifamily properties shows that per-unit insurance costs averaged $68 monthly in 2023 dollars by 2024, yet most owners still underestimate their replacement exposure and carry insufficient limits.

Request a professional property valuation specifically for insurance purposes, and model worst-case scenarios using catastrophe modeling tools that account for your ZIP code’s specific natural disaster exposure. Geographic variation explains over 42% of insurance cost differences according to Federal Reserve research, so a property in coastal Florida or Louisiana faces dramatically different risk profiles than an identical building in the Midwest.

Make Strategic Deductible Decisions

Your deductible choice matters more now than ever. The Minneapolis Federal Reserve found that average deductibles surged 412% year-over-year from 2023 to 2024, forcing owners to decide whether accepting higher deductibles to lower premiums makes financial sense given your cash reserves and property’s vulnerability to specific risks like water damage or fire. Honestly assess whether you can afford a $25,000 deductible versus a $5,000 one if a covered loss occurs.

Shop Multiple Carriers for Real Savings

Shopping multiple carriers reveals the dramatic pricing variation that exists in this market. Nearly all apartment owners now solicit competing bids because premium differences often exceed 30–40% for identical coverage, according to Federal Reserve survey data from multifamily owners. Request quotes that hold coverage limits constant across carriers so you compare apples to apples, and specifically ask each insurer about premium credits for risk-reduction investments like stovetop fire suppression devices, which some carriers credit at 10% or more, or smoke-free policies that reduce fire exposure.

Invest in Risk Mitigation Before Raising Rents

Three in five multifamily owners increased rents to offset higher insurance costs, but before you consider that path, exhaust your risk-mitigation options. Installing flood-prevention devices on water-supply lines, upgrading roofs, and implementing fire-prevention equipment often qualify for discounts that can offset 15–25% of premium increases. Request quotes with different deductible levels to see the true cost of accepting higher out-of-pocket exposure, and factor in endorsements for assault and battery, discrimination claims, and business interruption coverage that standard policies frequently exclude.

Verify Lender Compliance and Coverage Gaps

Verify that your lender’s minimum insurance requirements align with the quotes you receive, since some carriers impose stricter terms or exclusions than others, and non-compliance with mortgage requirements can trigger default clauses. Each insurer evaluates risk differently, so the coverage one carrier offers may differ substantially from another’s terms for the same property.

Final Thoughts

Protecting your apartment building requires honest assessment of your replacement costs, strategic decisions about deductibles, and comparison shopping across multiple carriers. The insurance market for multifamily properties has shifted dramatically, with premiums and deductibles rising faster than general inflation, which means your apartment building owner insurance decisions directly impact your bottom line and financial stability. Rising costs are real, but they’re not inevitable-owners who invest in risk mitigation like stovetop fire suppression devices, flood-prevention systems, and smoke-free policies often qualify for premium credits that offset 15–25% of increases.

Your next step is straightforward: request professional property valuations for insurance purposes, model your specific geographic and property-level risks, and solicit competing quotes from multiple carriers while holding coverage limits constant. Nearly all apartment owners now shop multiple insurers because premium differences frequently exceed 30–40% for identical coverage. Ask each carrier about credits for risk-reduction investments and endorsements for assault and battery, discrimination claims, and business interruption coverage that standard policies exclude.

Verify your lender’s minimum insurance requirements before finalizing any policy, since non-compliance can trigger default clauses and leave you exposed. The complexity of apartment building owner insurance-replacement cost calculations, deductible trade-offs, geographic risk variation, and carrier-specific terms-makes professional guidance invaluable. Contact Cappuccino Insurance Agency for a free coverage assessment and annual policy review to confirm you’re securing the best protection at the right price.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inaccuracies.